The hard disk drive industry may not get the same hype as AI chips, but it remains a major beneficiary of the artificial intelligence (AI) boom as data storage demand surges. That is where HDD makers still dominate, and Seagate Technology Holdings plc (STX) remains one of the biggest names powering large-scale storage worldwide.

The company has spent decades building a dominant position in large-scale data storage, making Seagate highly sensitive to manufacturing lead times and capacity decisions. So naturally, Wall Street reacted sharply this week, sending STX stock down 7.5% on Monday after CEO Dave Mosley raised concerns about increasingly long production cycles.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Speaking at the J.P. Morgan Global Technology, Media, and Communications Conference, he warned that some critical wafer operations now carry lead times of more than nine months due to increasing manufacturing complexity. He explained that the industry can no longer ramp production as quickly as it could 15 or 20 years ago.

That matters because, during a demand boom, long lead times can create major bottlenecks, affecting everything from supply availability to pricing power and future revenue growth. If Seagate cannot ramp production quickly enough, it risks leaving sales on the table just as AI-driven storage demand accelerates. Meanwhile, investors were uneasy about the CEO’s cautious stance on aggressive capacity expansion plans. Adding too much capacity too late can crush margins once demand cools.

The CEO tried to calm those fears by saying Seagate is taking a disciplined approach, adding manufacturing tools tied to future technology transitions rather than blindly flooding the market with extra capacity. He also noted that demand remains strong enough to absorb current output, while the company’s next-generation HAMR drives continue gaining traction with major cloud providers after shipping millions of units and securing major qualifications.

About Seagate Technology Stock

Headquartered in Singapore, Seagate Technology is one of the leading names in global data storage, developing HDDs, solid-state drives (SSDs), and storage solutions used in data centers, enterprise systems, and personal computing.

Backed by its research and manufacturing expertise and its global supply network, Seagate plays an important role in managing the world’s growing data needs. As cloud computing and AI continue expanding, the company is focusing heavily on high-capacity storage innovation. Today, Seagate carries a market capitalization of $166.1 billion.

That growing demand has also fueled a powerful rally in Seagate Technology stock. As AI infrastructure spending accelerates, hyperscalers and cloud companies are racing to secure high-capacity, cost-efficient storage solutions – an area where Seagate’s advanced Mozaic HAMR drives are gaining strong traction. The result has been a sharp shift in investor sentiment, turning Seagate from a steady storage name into one of the market’s hotter AI infrastructure plays.

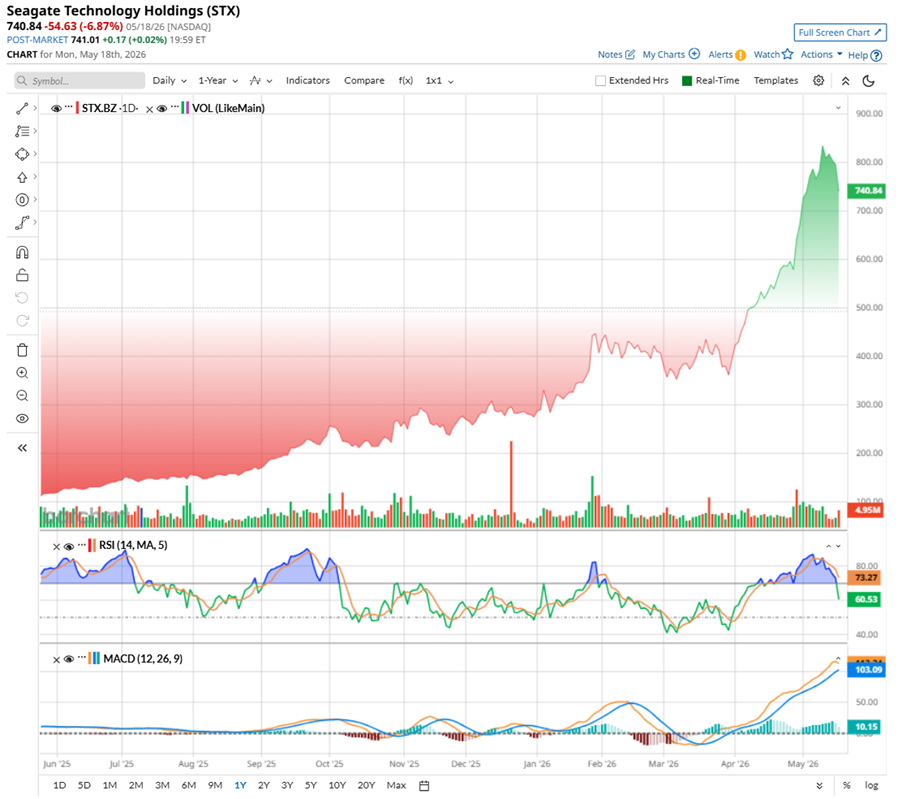

After one of the market’s impressive rallies, STX stock finally appears to be catching its breath. Shares recently pulled back 12.8% from their all-time high of $841.31 reached on May 11, as investors reacted strongly to CEO Dave Mosley signaling a more cautious approach toward capacity expansion and discussing increasingly long manufacturing lead times. The comments arrived after a near-parabolic run fueled by AI enthusiasm, booming demand for high-capacity storage, and growing worries around global chip shortages.

Even with the recent dip, the stock’s overall performance remains extraordinary. STX has surged 572.55% over the past 52 weeks and climbed another 183% in just the last six months. The momentum has remained remarkably strong throughout 2026 as well, with shares already up 166.3% year-to-date (YTD).

The gains accelerated in the recent months following Seagate’s blowout fiscal Q3 earnings report, which highlighted record margins and powerful AI-driven demand from hyperscalers and data centers. Over the past month alone, the stock has jumped 33.9% as Wall Street analysts rolled out bullish price-target upgrades.

Technically, the chart suggests momentum may still favor the bulls despite the cooldown. The 14-day RSI has eased back to 59.04 after previously flashing overbought conditions, signaling the rally may simply be pausing. Meanwhile, the MACD oscillator flashes bullish signals, with the MACD line holding above the signal line since mid-March alongside positive histogram readings, suggesting that buyers still appear to control the broader trend even after the recent pullback.

www.barchart.com

www.barchart.com After such a massive rally, valuation has naturally become a bigger conversation around Seagate Technology. STX is priced at 56.42 times forward adjusted earnings, which sits above the industry average, though still slightly below its own historical median. The premium becomes even more noticeable with its forward price-to-sales ratio of 13.79 times, far above both sector norms and historical levels. Wall Street is placing quite a rich premium on Seagate’s role in the AI-driven storage boom, leaving less room for execution mistakes if growth slows.

Further, Seagate Technology has built a solid reputation for consistently returning cash to shareholders. The company has been paying dividends for more than a decade and has even raised them over the years, showing confidence in its cash-flow strength. STX declared a quarterly dividend of $0.74 per share recently, payable on July 7, 2026. That puts the annualized payout at $2.96 per share, giving the stock a forward yield of around 0.37%. That’s not huge, but still a steady bonus for long-term investors.

A Closer Look at Seagate's Q3 Numbers

Seagate delivered its impressive third-quarter results for fiscal 2026 on April 29, with revenue amounting to $3.11 billion, up 44.1% year-over-year (YOY) and comfortably exceeding Wall Street’s projections. Non-GAAP EPS rose 115.8% annually to $4.10, again ahead of expectations.

AI data rapid growth is fueling massive demand for high-capacity storage, and Seagate Technology is capitalizing through efficient high-density drives, helping boost both growth and profit margins. The company’s non-GAAP operating margin came in at a record 37.5%, up sharply from 23.5% a year ago.

Plus, cash flow also came in strong, with $1.1 billion generated from operations and $953 million in free cash flow. The company used part of that cash to pay down $641 million in debt while still returning $191 million to shareholders through dividends and buybacks.

Meanwhile, nearline drives used by hyperscalers accounted for roughly 90% of shipments, with much of that capacity already booked through 2027.

Looking ahead, the management anticipates Q4 revenue around $3.45 billion, plus or minus $100 million. This represents 41% YOY growth at the midpoint. Non-GAAP EPS is guided to $5, plus or minus $0.20.

Wall Street analysts are optimistic about Seagate’s growth potential, expecting a revenue of $3.48 billion in Q4, with EPS expected to be somewhere around $4.83. For the current fiscal year, profit is expected to rise 94.2% annually to $14.10 per share, and then grow by another 81% annually to $25.52 in fiscal 2027.

What Do Analysts Expect for Seagate Stock?

After Seagate Technology delivered strong Q3 results, several Wall Street firms raised their price targets. But optimism surged further after Evercore lifted its STX target to $1,000 following meetings with Seagate’s management.

Evercore analyst Amit Daryanani believes Seagate’s growth story could last for years, not just quarters, and that’s due to the company’s focus on increasing storage capacity through areal density improvements and technologies like HAMR, which allow Seagate to store far more data on each drive without dramatically increasing costs. Evercore also pointed to Seagate’s long-term customer agreements, some stretching through 2027, which provide unusually strong visibility into future demand.

The analyst noted that HDD markets operate far more discipline than NAND memory, helping Seagate maintain pricing power. He expects the HAMR rollout to support growth through 2030, while AI workloads, video generation, autonomous driving, cameras, and sensors continue accelerating global data creation and increasing the need for long-term data retention.

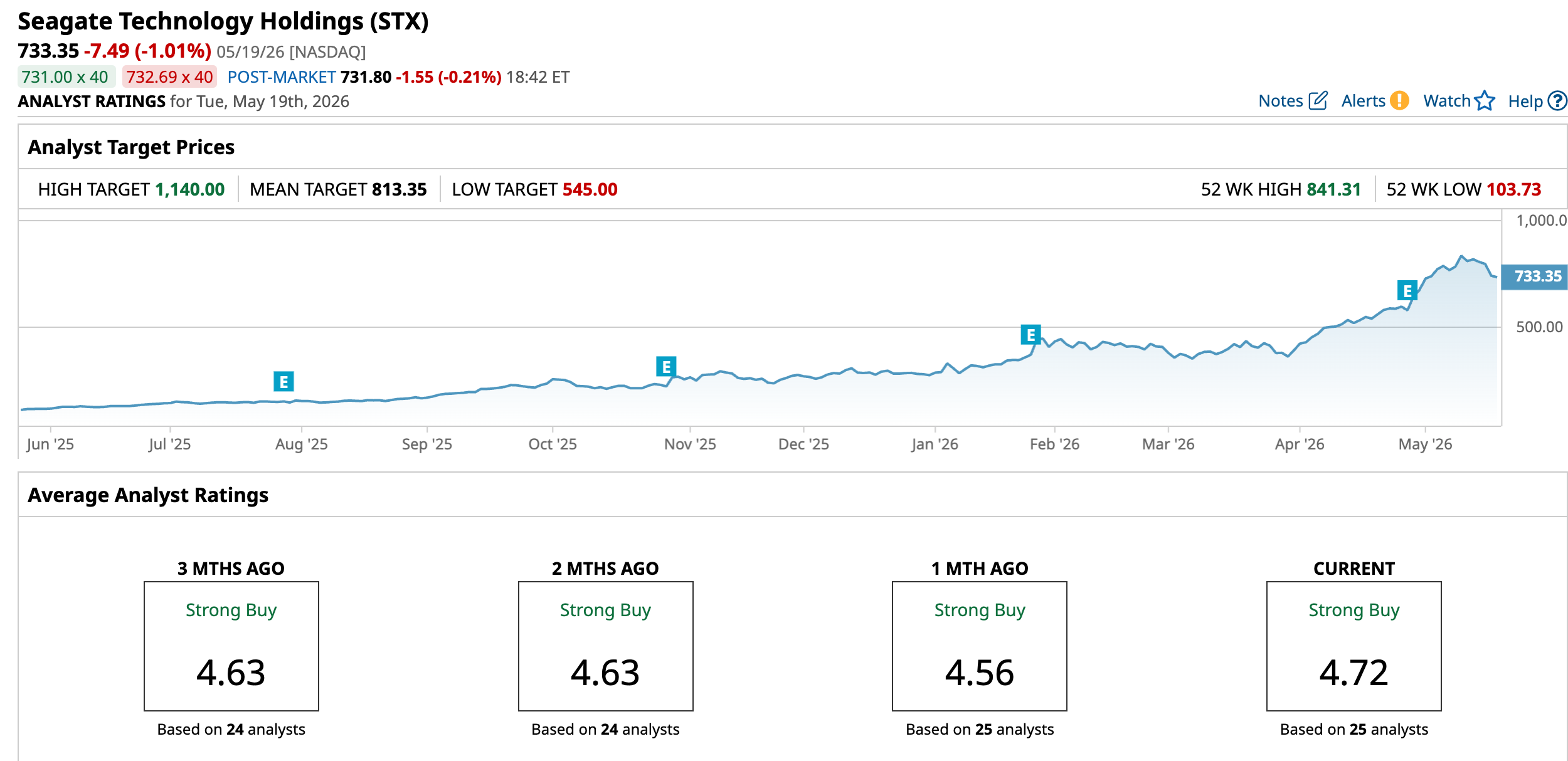

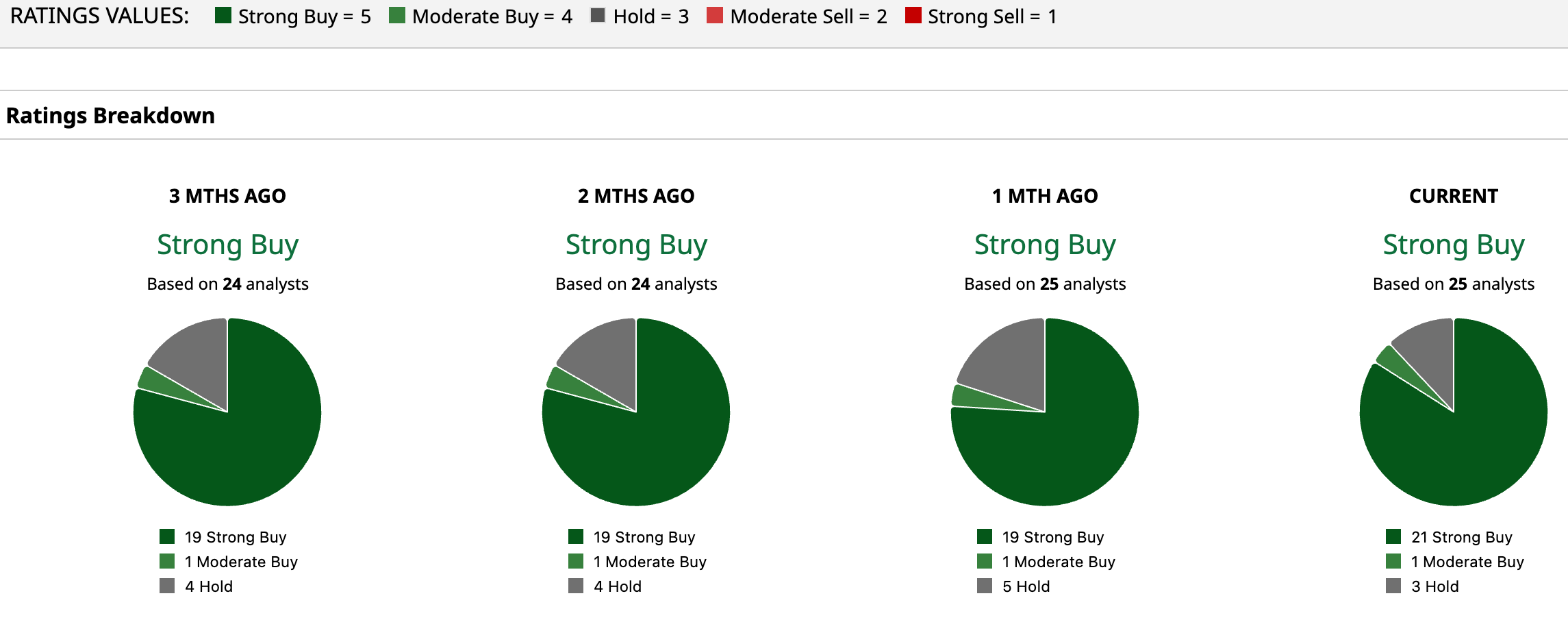

STX stock has an overall “Strong Buy” rating. Of the 25 analysts rating the stock, 21 rate it a “Strong Buy,” one has a “Moderate Buy,” and three analysts are playing it safe with a “Hold” rating.

STX’s mean price target of $813.35 suggests an upside potential of 11% from here. But some analysts, like Evercore’s Amit Daryanani, think the rally may still have room to run, with the Street-high target of $1,140 suggesting the stock could surge as much as 55.5%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Seagate Stock Plunges on Executive Warnings. Why Lead Times Matter so Much for STX Here. Cathie Wood Joins the Cerebras Bandwagon With More Than 100,000 Shares. Wait for It to Deliver Before You Buy In, Too. Dominion, NextEra Merge to Create a $67 Billion Electric Behemoth. History Tells Us This Is a Cautionary Tale. AMD’s AI CPU Opportunity Is Getting Bigger and So Is the AI-Driven ‘Boom’ for AMD Stock