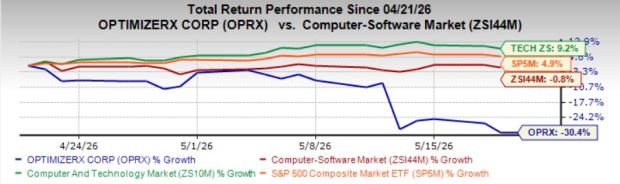

OptimizeRx Corporation OPRX stock has lost 30.4% in the past month compared with the Zacks Computer Software industry’s decline of 0.8%. The stock has also underperformed the Zacks Computer & Technology sector and the S&P 500 composite growth of 9.2% and 4.9%, respectively.

The stock has underperformed its peers, such as Omnicell OMCL, Doximity DOCS, and Veeva Systems VEEV. OMCL has gained 19.2% while DOCS and VEEV lost 20.2% and 2.7%, respectively, in the same time frame.

Image Source: Zacks Investment Research

Investors may wonder whether OPRX has further downside risk or if its underlying fundamentals can help stabilize the stock. Let’s examine the company’s strengths, operational challenges and growth outlook to determine the best course of action.

Key Factors to Consider

OptimizeRx’s near-term performance remains under pressure due to ongoing macroeconomic challenges and disruption related to most favored nation (MFN) pricing dynamics, which have resulted in more cautious customer spending, shorter contract durations and delayed campaign timing. On the last earnings call, management highlighted that visibility into the full year remains limited, prompting the company to lower its 2026 revenue guidance to $95-$100 million from prior expectations. Revenue in the first quarter declined 10% year over year to $19.8 million, reflecting softness in the contracted revenue base and weaker spending patterns among certain pharmaceutical customers.

The company also continues to face customer-specific execution challenges that negatively impact growth and guidance visibility. Management highlighted that one major client remains disrupted due to a combination of MFN-related pressures, internal customer changes and execution shortcomings on OptimizeRx’s side. Contracted revenue declined 15-20% year over year because clients are increasingly opting for shorter-duration agreements instead of the typical six-to-12-month commitments, limiting backlog visibility and increasing renewal risk throughout the year.

Cash flow and balance sheet metrics also reflected some pressure during the first quarter. Cash and cash equivalents declined to $20.2 million at the end of the first quarter from $23.4 million at the end of 2025, while operating cash flow turned negative, primarily due to bonus payouts and sales commission payments. Although debt levels improved following repayments, the company still carried $23.6 million in debt exiting the quarter. In addition, average revenue per top 20 pharmaceutical manufacturers declined year over year, while net revenue retention softened slightly to 110% from 114%, indicating moderating expansion within existing accounts.

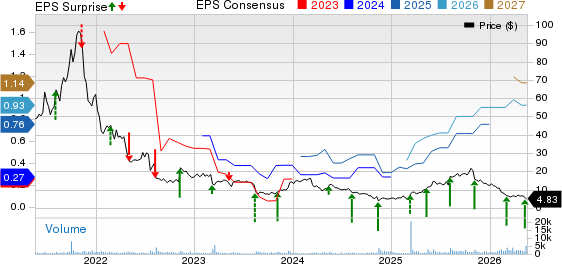

OptimizeRx Corp. Price, Consensus and EPS Surprise

OptimizeRx Corp. price-consensus-eps-surprise-chart | OptimizeRx Corp. Quote

Despite these headwinds, OptimizeRx delivered improved profitability metrics in the first quarter, supported by cost optimization efforts and a favorable product mix. Adjusted EBITDA more than doubled year over year to $3.3 million, while non-GAAP net income increased to $2.7 million from $1.5 million in the prior-year period. The company also maintained its adjusted EBITDA guidance of $21-$25 million despite lowering revenue expectations, reflecting confidence in operating leverage, efficiency initiatives and margin improvement strategies. Management expects annualized savings of approximately $3 million from recently launched operating efficiency programs.

The company is also benefiting from strong momentum in its AI-enabled DAAP platform and subscription-based offerings. DAAP revenue grew 60% in the first quarter, while DAAP subscription revenue increased 45%, highlighting growing customer adoption and improving revenue durability. Management also noted increasing traction among mid-tier and long-tail life sciences customers, alongside expanding opportunities in medtech, where pilot programs are evolving into multimillion-dollar engagements.

OptimizeRx is further strengthening its long-term outlook through strategic platform expansion and improved financial flexibility. The company recently enabled demand-side platforms controlling more than 80% of digital promotional spending to connect directly into its proprietary EHR network, opening a potentially significant new revenue channel. Management believes this initiative could materially increase inventory utilization and drive substantial long-term growth beginning in late 2026 and accelerating into 2027. Additionally, the refinancing of its debt with Fifth Third Bank reduced borrowing costs by approximately 625 basis points, which is expected to generate around $1.5 million in annual interest expense savings and improve overall financial flexibility.

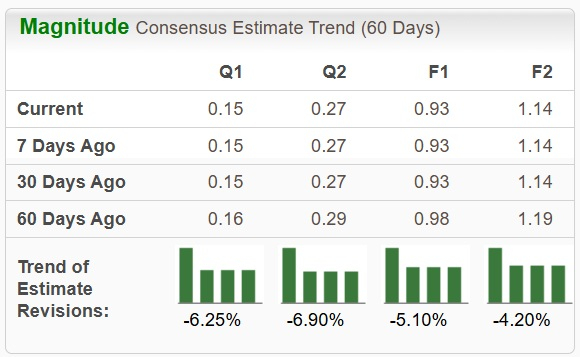

OPRX’s Estimate Revision Trend Unfavorable

OPRX’s estimates are currently on a downward trajectory. The Zacks Consensus Estimate for OPRX’s earnings for fiscal 2027 has been revised downward over the past 60 days.

Image Source: Zacks Investment Research

A Look at OPRX’s Valuation

OPRX is trading at a forward 12-month price/sales ratio of 0.88, lower than the sector’s multiple of 6.71.

Image Source: Zacks Investment Research

OMCL, DOCS and VEEV are trading at a forward 12-month price/sales ratio of 1.58, 5.16 and 7.19, respectively.

Should You Hold or Sell Now?

Given OPRX’s weakening revenue visibility, ongoing customer-related disruptions and downward estimate revisions, investors should stay on the sidelines until the company demonstrates a more stable growth trajectory and improved business momentum.

OPRX currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicell, Inc. (OMCL): Free Stock Analysis Report

OptimizeRx Corp. (OPRX): Free Stock Analysis Report

Veeva Systems Inc. (VEEV): Free Stock Analysis Report

Doximity, Inc. (DOCS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).