Akamai Technologies Inc. (AKAM) is a global computing, cybersecurity, and content delivery network (CDN) provider. The company optimizes web traffic through edge routing algorithms and has successfully transitioned its core business focus far beyond internet delivery.

Founded in 1998, the company is headquartered in Cambridge, Massachusetts.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

AKAM Stock Rallies

Akamai's stock performance reflects its strategic multi-year transformation from a legacy content delivery network into a high-growth cloud security and decentralized infrastructure business. The stock has mounted an explosive rally, posting a 64.5% year-to-date return and skyrocketing by 85% over the past 52 weeks. This momentum accelerated into a fresh 52-week high of $165.45, heavily backed by structural accumulation.

Compared with the illustrious S&P 500 Information Technology ($SRIT), Akamai has delivered a market-shaking alpha in recent months. While the cap-weighted sector benchmark posted steady double-digit gains backed by mega-cap software names, Akamai’s 47% performance surge over the past 30 days alone has completely outpaced the broader index average.

www.barchart.com

www.barchart.com Akamai Posts Strong Results

Akamai delivered a solid financial performance for the first quarter of 2026, highlighted by accelerating enterprise demand for its expanding cloud infrastructure and specialized security offerings. The company reported total quarterly revenue of $1.07 billion, matching analyst expectations and representing a 6% increase year-over-year.

Growth was led primarily by the cloud infrastructure services division, which surged 40% annually to $95 million, and the security segment, which rose 11% to $590 million, offsetting a 7% decline in legacy delivery applications. Cash flow from operations remained resilient at $313 million, supporting $206 million in common stock repurchases during the quarter.

Profitability faced short-term pressure due to heavy infrastructure investments and payroll costs, resulting in a GAAP operating margin contraction to 11% and a 14% drop in GAAP net income to $106 million. Non-GAAP net income reached $239 million, translating to adjusted diluted earnings-per-share of $1.61, beating the consensus estimate.

Looking ahead, management raised its full-year 2026 revenue guidance to a midpoint of $4.5 billion and adjusted earnings-per-share estimates to $6.78, supported by a new seven-year, $1.8 billion cloud infrastructure contract signed with Anthropic, a major frontier AI model provider. This structural backlog positions Akamai to capture sustained, high-margin AI inference workloads at the edge through the end of the decade.

Akamai Down on Convertible Note Offering

Shares of Akamai Technologies dropped 5% following the announcement of a proposed $2.6 billion private offering of 0% convertible senior notes due in 2030 and 2032. Initial institutional purchasers retain an option to buy up to an additional $400 million in notes. Akamai intends to deploy the net proceeds to finance the accelerated capital expenditure requirements of its cloud infrastructure services business, specifically targeting the rapid expansion of its global footprint.

Additionally, a portion of the capital will fund convertible note hedge transactions to mitigate future equity dilution, alongside a planned $350 million private share repurchase program. The notes will exist as senior unsecured obligations and can be settled by Akamai in cash, common stock, or a combination of both upon conversion.

Should You Bet on AKAM?

Akamai’s convertible senior notes offering triggered short-term equity dilution fears, but it strategically funds an aggressive, footprint-expanding buildout of its cloud services.

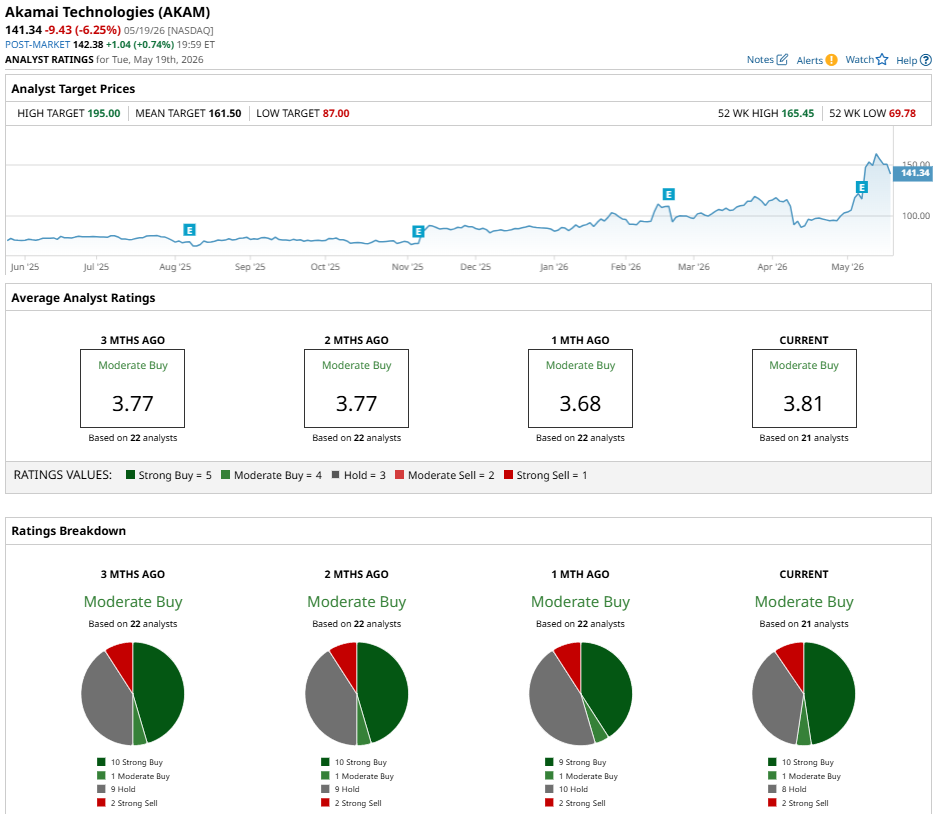

This calculated high-growth pivot underpins a Wall Street consensus "Moderate Buy" rating. Of the 21 tracked analysts, the breakdown includes 10 "Strong Buy" ratings and one "Moderate Buy" rating, balanced against eight "Holds" and two "Strong Sells." Backed by a mean price target of $160.79, Akamai offers a 12.8% projected upside from its recent market price, presenting an attractive risk-reward profile for investors seeking decentralized AI edge infrastructure.

www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wall Street Is Warming Up to ServiceNow Stock. That’s Because It’s Now a Bet on Agentic AI. INM Stock Alert: What to Know as InMed, Mentari Announce Merger The $2.6 Billion Power Play: How Akamai Is Weaponizing Debt to Build the AI Edge Up 153% YTD, Here's Why Micron Stock Is Already My 2026 Winner