Shares of Sun Life Financial Inc. SLF are trading at a premium compared with the industry. Its trailing 12-month price-to-book value of 2.56X, is above the industry average of 2.06X, but below the finance sector's 4.33X, and the Zacks S&P 500 composite’s 8.09X.

With a market capitalization of $36.62 billion, the average volume of shares traded in the last three months was 0.7 million.

Image Source: Zacks Investment Research

Shares of other insurers like Reinsurance Group of America, Incorporated RGA , Manulife Financial Corp MFC and Primerica, Inc. PRI are trading at 1.05X, 1.91X and 3.53X respectively.

SLF Is an Outperformer

Shares of Sun Life have risen 15.7% in the past year compared with the industry, the Finance sector and the Zacks S&P 500 index’s growth of 14.2%,12.8% and 31.6%, respectively.

Image Source: Zacks Investment Research

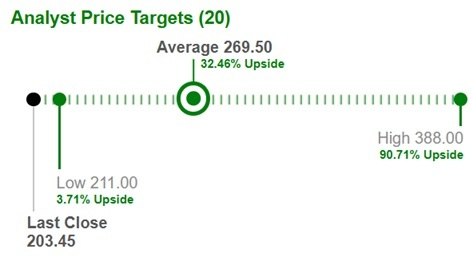

Average Target Price for SLF Suggests Upside

Based on short-term price targets offered by 20 analysts, the Zacks average price target is $269.50 per share. The average suggests a potential 32.46% upside from the last closing price.

Image Source: Zacks Investment Research

Projections for SLF

The Zacks Consensus Estimate for Sun Life’s 2026 earnings per share is pinned at $5.24, implying a year-over-year increase of 7.6%. The Zacks Consensus Estimate for Sun Life’s 2027 earnings per share indicates a year-over-year increase of 8.9%.

The insurer has a solid track record of beating earnings estimates in each of the trailing three quarters, with an average surprise of 2.63%. Earnings have grown 4.5% in the past five years.

Key Points to Note for SLF

Sun Life is focusing on the emerging economies of Asia, which are expected to provide higher returns and growth than the North American markets. It has a solid presence in China, the Philippines, India, Hong Kong and Indonesia and has also forayed into Malaysia and Vietnam. The contribution from the Asia business to SLF’s earnings has increased to 21% over the last few years.

SLF envisions itself as one of the top five players and remains focused on growing its voluntary benefits business. SLF is shifting its growth focus toward products that require lower capital and offer more predictable earnings, such as mutual funds and group benefits. The company intends to invest an additional $20 billion over the next five years across its general account and third-party investments.

Sun Life continued to effectively manage capital with more than 10 strategic transactions, including the acquisition of Pinnacle Care, the IPO of India Asset Management Joint Venture and buying DentaQuest to boost health and group benefits in the United States. The company estimates thst it will generate more than $7 billion in total annual U.S. benefits revenues as one of the largest providers of specialty benefits in the United States. This transformational deal will drive improved market positioning and growth.

SLF has been working to strengthen Asset Management, which provides a higher ROE, requires lower capital, witnesses lesser volatility and has the potential for an earnings upside. Thus, Sun Life Investment Management’s investments in private fixed-income mortgages and real estate, as well as in pension plans and other institutional investors, should bear fruit.

The company’s capital position remains strong, with Sun Life Assurance’s Life Insurance Capital Adequacy Test (“LICAT”) ratio at 134%. The balance sheet and capital positions remain robust, with SLF’s LICAT ratio of 143%. Sun Life had $1.3 billion in cash and other liquid assets as of March 31, 2026. This reflects disciplined capital management and a sustained emphasis on capital-light businesses.

Risks for SLF

Sun Life's expense increase over the past few years averaged 11%. Expenses increased due to high employee expenses, premises and equipment, service fees, amortization of intangible assets and other expenses.

SLF has employed hedging costs to offset unstable earnings due to the volatility in equity markets and interest rates. These costs have exerted pressure on the company’s earnings.

Conclusion

Sun Life’s focus on strengthening its Asian presence, expanding global asset management business, favourable business mix and solid capital position bode well for growth. However, increased expenses and volatility in equity markets and interest rates are the main concerns.

Consistent wealth distribution makes it an attractive pick for yield-seeking investors. Its dividend payout ratio is targeted within the 40-50% range.

Coupled with the solid financial position, favorable growth projections and strategic acquisitions. It is, therefore, wise to retain this Zacks Rank #3 (Hold) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Manulife Financial Corp (MFC): Free Stock Analysis Report

Reinsurance Group of America, Incorporated (RGA): Free Stock Analysis Report

Primerica, Inc. (PRI): Free Stock Analysis Report

Sun Life Financial Inc. (SLF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).