Nuclear energy has suddenly become the hottest ticket in town as artificial intelligence (AI) data centers, industrial giants, and defense operators hunt for reliable power around the clock. Small modular reactor companies are now seeing a massive opening as hyperscalers chase electricity deals at breakneck speed.

Right in the middle of the frenzy, Oklo (OKLO) has muscled its way into the spotlight, with Bank of America Corporation (BAC) now calling the company an “early leader” in the fast-heating nuclear race. The growing optimism spilled into the market on Friday, May 22 after Bank of America restarted coverage on OKLO stock with a “Buy” rating and an $80 price target, pushing the stock up 1.2% during the session.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

BoFA analysts led by Ross Fowler believe Oklo holds a unique advantage because instead of merely building reactors and walking away, the company plans to own, operate, and manage its nuclear systems while securing long-term customer contracts that allow it to capture the full economics of every project.

BofA also believes early commercial traction further strengthens the bull case for Oklo. The bank pointed to the company’s nearly 1.2 GWe binding power agreement with Meta Platforms (META) alongside a development pipeline exceeding 14 GWe through non-binding customer letters.

According to the bank, that already places Oklo among the largest players in the small modular reactor space while signaling that demand for advanced nuclear reactors continues gaining steam.

With its demonstration reactor remaining on track and hyperscaler agreements steadily piling up, Oklo seems to stand in a sweet spot to capitalize on the rapidly expanding nuclear energy market.

About Oklo Stock

Headquartered in Santa Clara, Oklo develops advanced nuclear fission power plants designed to deliver scalable clean energy solutions. Its Aurora Powerhouse reactors produce between 15 megawatts and 75 megawatts of electricity.

The $11.462 billion market cap company also develops nuclear fuel recycling and fabrication technology that converts used nuclear fuel into reusable reactor fuel, which allows the company to tighten its grip across multiple parts of the nuclear energy value chain.

The stock itself has kept investors on their toes. Oklo’s shares skyrocketed 43.95% in the past 52 weeks as enthusiasm surrounding nuclear energy and AI-powered electricity demand gained steam. Even so, the stock still sits down 1.96% year-to-date (YTD). However, shares managed to edge 1.85% higher in the last three months.

www.barchart.com

www.barchart.com Hoever, valuation remains sky high. OKLO stock currently trades at 10.74k times sales, which towers above industry averages and signals that investors already expect substantial future growth from the company.

A Closer Look at Oklo’s Q1 Earnings

The advanced nuclear startup released its Q1 FY2026 results on May 12 which led its shares sliding 5.8% following the report. The reaction came after Oklo posted wider losses, elevated spending, and another reminder that meaningful revenue generation still remains years away.

The company continues operating firmly in development mode while pouring cash into reactor engineering, fuel systems, infrastructure, licensing work, and long-term deployment plans tied to its Aurora nuclear platform.

For the quarter, Oklo reported a net loss of $33.07 million, or negative $0.19 per share. During the same period last year, the company posted a loss of $9.8 million, or negative $0.07 per share. Operating expenses climbed sharply to $51.2 million from $17.9 million one year earlier as Oklo expanded hiring across technical and administrative teams while stock-based compensation expenses also moved substantially higher.

Research and development spending alone surged to $27 million during the quarter as the company accelerated investment in reactor design, fuel development, and commercialization technologies. Even so, Oklo managed to hand investors an important silver lining beneath the headline losses.

The company exited the quarter with roughly $2.5 billion in cash and marketable securities, largely fueled by a successful at the market equity offering program that generated approximately $1.2 billion in net proceeds. Management says that capital will support expansion efforts across the company’s power, fuel, and isotope businesses as commercialization efforts continue ramping higher.

Looking ahead, analysts expect Q2 FY2026 loss per share to widen 5.6% year-over-year (YOY) to $0.19. For full FY2026, Wall Street expects loss per share to deepen another 11.1% to $0.80. Analysts also forecast FY2027 loss per share to expand another 20% YOY to $0.96 as Oklo continues investing aggressively in future growth.

What Do Analysts Expect for Oklo Stock?

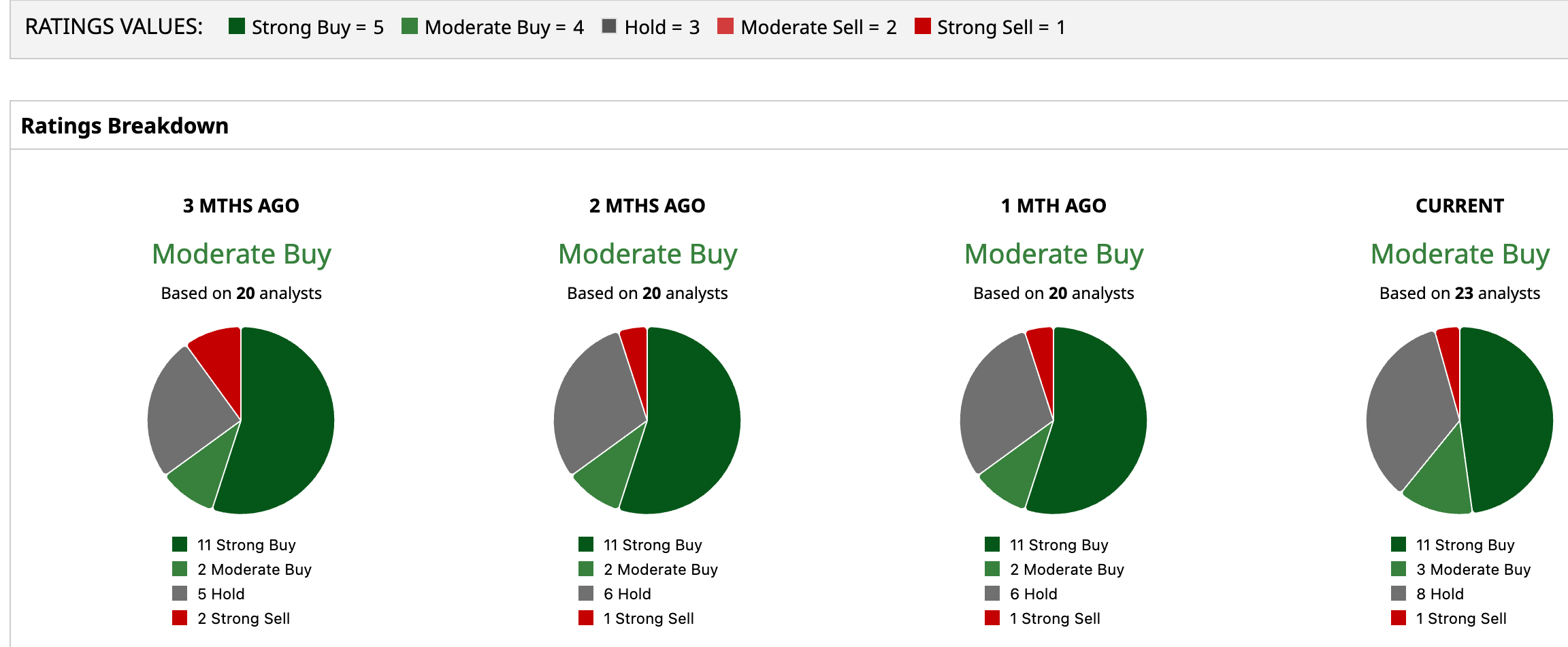

Despite the mounting losses, Wall Street still leans bullish on the stock overall. Analysts currently assign OKLO stock an overall “Moderate Buy” rating. Among 23 analysts covering the stock, 11 analysts rate the stock a “Strong Buy,” three call it a “Moderate Buy,” eight remain on the sidelines with “Hold” ratings, while one analyst carries a “Strong Sell” recommendation.

The broader analyst community also sees further upside. The stock’s average price target of $86.30 represents potential upside of 25.6%. Meanwhile, the Street-High target of $130 suggests a gain of 89.2% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Oklo Stock Gets a New ‘Buy’ Rating from Bank of America: It’s an ‘Early Leader’ 1 Mega-Cap Tech Stock With 35% Upside Just Dropped a Reddit-Like App BlackBerry Just Hit a New 52-Week High. Here's Why Walmart Is Supposed to Be a Safe-Haven Stock. High Gas Prices Are Hitting Its Shares Instead.