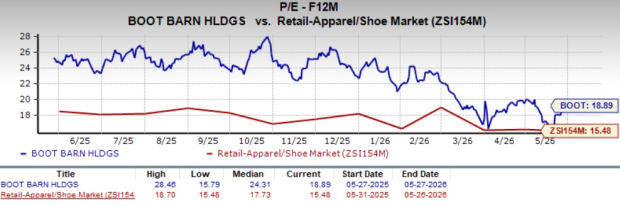

Boot Barn Holdings, Inc. BOOT a prominent player in the retail apparel and shoes sector, is currently trading at a forward 12-month price-to-earnings (P/E) ratio of 18.89X, which is higher than the industry’s average P/E of 15.48X. This higher valuation reflects investor confidence in BOOT’s long-term growth. The stock trades below its one-year median P/E ratio of 24.31X, which suggests that although BOOT is slightly cheaper than its recent historical average, it still remains an expensive stock in a broader market context.

Image Source: Zacks Investment Research

This premium positioning is particularly noticeable compared with peers such as Deckers Outdoors Corporation DECK, American Eagle Outfitters, Inc. AEO and Urban Outfitters, Inc. URBN, which have P/E of 15.23X, 9.70X and 12.21X, repectively.

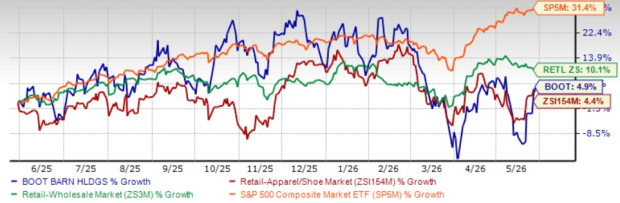

BOOT’s shares have gained 4.9% in the past year, outperforming the Zacks industry’s growth of 4.4%. However, the stock has underperformed the broader sector’s 10.1% growth and the S&P 500 Index’s 31.4% increase in the same period.

BOOT Stock's 1-Year Return

Image Source: Zacks Investment Research

Closing at $165.35 in the last trading session, Boot Barn stock stands 21.4% below its 52-week high of $210.25 reached on Dec. 12, 2025. BOOT is trading above its 50-day simple moving average of $156.9, indicating a favorable technical setup for the stock.

BOOT Trades Above 50-Day SMA

Image Source: Zacks Investment Research

BOOT Benefits From Store Expansion & Brand Penetration

Boot Barn’s recent stock momentum has been driven by strong execution across store expansion, comparable sales growth, digital initiatives and margin improvement, reinforcing investor confidence in the company’s long-term growth trajectory. The company delivered a solid fourth-quarter fiscal 2026 performance, supported by healthy same-store sales and continued success in expanding its store base. Management also accelerated several store openings planned for the next fiscal year, signaling confidence in demand and execution capabilities.

New stores are contributing meaningfully to incremental sales and earnings, while maturing locations are supporting comparable-store sales as they enter the comp base. This highlights the scalability of Boot Barn’s growth model.

Digital strength has also supported investor sentiment. E-commerce sales remained robust, led by bootbarn.com, while dedicated websites for Cheyenne and CLEO & WOLF expanded the company’s direct-to-consumer reach and improved brand storytelling.

Merchandise margin expansion is another key driver, fueled by rising exclusive brand penetration. These brands enhance product differentiation, support pricing power and strengthen profitability.

Additionally, Boot Barn’s AI initiatives are aimed at improving customer engagement, driving traffic, enhancing operational efficiency and supporting personalized marketing. Overall, strong comps, disciplined expansion, digital growth, exclusive brand momentum and technology-driven efficiencies have fueled confidence in BOOT’s growth prospects.

BOOT Guidance Looks Compelling

Boot Barn issued a strong fiscal 2027 outlook, expecting total sales growth in the range of 14%-16% to $2.578-$2.623 billion alongside consolidated same-store sales growth of 2%-4%. The company plans to open 70 new stores in the year, in addition to 10 accelerated openings completed in fiscal 2026. Management also expects a merchandise margin of 51.4% and earnings per share in the range of $8.21-$8.64.

For the first quarter of fiscal 2027, the company projects sales growth of 14%-16% to $574-$584 million, supported by consolidated same-store sales growth of 2%-4% and continued strength in e-commerce. Management also guided for a merchandise margin of 51.5%, while earnings per share are expected to be in the range of $1.62-$1.71.

How Have Estimates Shaped Up?

The Zacks Consensus Estimate for BOOT’s fiscal 2027 earnings per share has improved by a penny to $8.56 in the past 30 days. The consensus mark for fiscal 2028 earnings per share has improved 1.2% to $9.92 in the past 30 days.

Image Source: Zacks Investment Research

Are Gross Margin Pressures Hurting BOOT?

Gross margin pressures remain a key concern. Tough year-over-year comparisons hurt Boot Barn’s fourth-quarter fiscal 2026 gross margin, as the prior-year period benefited from lower shrink and freight costs. Higher buying, occupancy and distribution center expenses, largely related to new store openings, added further pressure. As a result, gross profit declined year over year despite continued sales growth and expansion efforts.

The company also expects first-quarter fiscal 2027 gross margin to remain under pressure due to deleverage in buying, occupancy and distribution center costs, suggesting that elevated operating expenses may continue to weigh on near-term profitability.

How to Play BOOT Stock?

Boot Barn’s premium valuation appears justified by its merchandise margin expansion, exclusive brand strategy and accelerating store expansion, all of which support sustained top-line momentum. While the stock’s premium valuation warrants caution, its resilient business model offers a compelling case for long-term investors.

The prudent move for existing investors may be to hold their positions rather than chase the stock at its current highs. Prospective investors may prefer to wait for a more attractive entry point. At present, BOOT carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Eagle Outfitters, Inc. (AEO): Free Stock Analysis Report

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Urban Outfitters, Inc. (URBN): Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).