In the energy sector, Cenovus Energy Inc. CVE and ConocoPhillips COP are two well-known names. Cenovus Energy is an integrated energy company based in Canada, with operations across upstream and downstream segments. CVE’s upstream operations are mainly concentrated in Canada, including its oil sands projects in northern Alberta and conventional crude oil and natural gas projects across Western Canada. Additionally, its downstream footprint includes refining operations in Canada and the United States.

On the other hand, ConocoPhillips is a pure play upstream energy company, with operations in 14 countries worldwide, including the United States, Norway, Canada, Australia and Qatar. The company holds a deep, durable inventory of low-cost supply in the U.S. Lower 48, which contributes to the majority of its consolidated liquids and natural gas production.

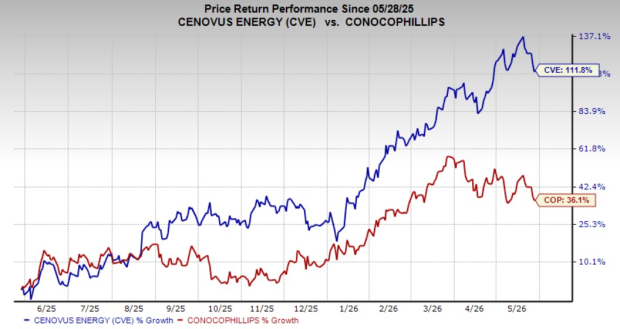

Over the past year, CVE has surged 111.8%, outperforming COP’s 36.1% gain. While price performance demonstrates the attractiveness of any stock, it would be wiser to evaluate the fundamentals and overall business environment of both stocks before coming to an investment decision.

CVE’s Integrated Business Model and MEG Acquisition Drive Growth

Cenovus’ integrated business model offers strategic value, enhances resilience and provides a cushion against Canadian heavy oil pricing volatility. The company benefits from the low-cost and long reserve life of its asset base. Cenovus’ production, mainly from the oil sands assets, consists of heavy and bitumen-blend crude, the price of which is linked to the Western Canadian Select (“WCS”).

WCS usually trades at a discount compared to the West Texas Intermediate (“WTI”) benchmark, as the Canadian heavy oil is more difficult to refine. In its latest presentation, Cenovus mentioned that its downstream integration and access to pipeline capacity allow it to offset the risk of Western Canadian price dislocation. Notably, the company stated that it expects to have more than 750 thousand barrels per day (MBbls/D) of heavy oil egress and conversion capacity by 2028. This will be supported by its Canadian and U.S. refining capacity, TMX access and future contracted U.S. pipeline capacity. This implies that the integration of its upstream and refining operations cushions volatility and supports profitability.

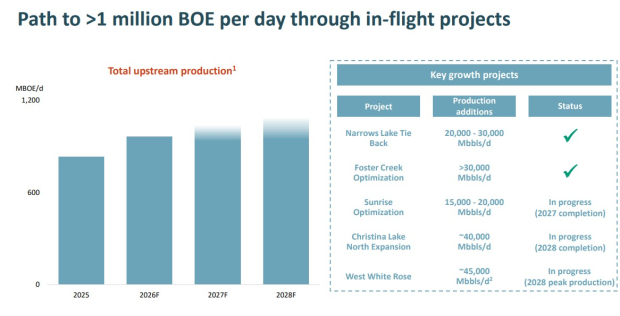

Another major catalyst for CVE’s long-term growth is the successful integration and expansion potential of the Christina Lake North assets (formerly known as MEG Energy’s Christina Lake). The acquisition meaningfully adds to the company’s asset base, extending its production capacity and reserve life. The company also mentioned that the redevelopment-well program at Christina Lake North started ahead of schedule and is expected to support a meaningful production increase throughout the rest of the year. Additionally, CVE has multiple growth projects underway to drive production growth to upward of 1 million barrels of oil-equivalent by 2028.

Image Source: Cenovus Energy

Low-Cost of Production and High Oil Prices Support COP’s Profitability

ConocoPhillips holdsa strong portfolio of assets in the shale basins of the United States, including the Delaware Basin, Midland Basin, Eagle Ford and Bakken shale. The company highlights that it boasts a deep, durable and high-quality inventory in the U.S. Lower 48 that supports production at low breakeven costs. In addition, the company’s production is supported by other assets outside of the Lower 48, including the oil sands in Canada and conventional assets in Asia, Europe and the Middle East, further supporting low-cost operations. This allows the upstream player to generate incremental cash flows, particularly during periods of high commodity prices.

At present, the commodity pricing scenario is significantly more favorable than in the previous year. Per the data from the U.S. Energy Information Administration, the WTI spot price benchmark is expected to average $96.42 per barrel in the second quarter, higher than $64.63 in the prior-year quarter. As a pure-play upstream energy firm, COP stands to benefit significantly from rising oil prices, as higher prices support increased cash flow.

However, commodity prices are generally volatile and are affected by several factors, including global demand growth and geopolitical conditions. Despite the volatility, ConocoPhillips maintains an unhedged strategy, which means it retains full upside in bullish market conditions but also bears the full downside when crude oil and natural gas prices weaken. While ConocoPhillips emphasizes capital discipline and resilience, its financial condition and operating results remain dependent on unpredictable macroeconomic and commodity-market factors.

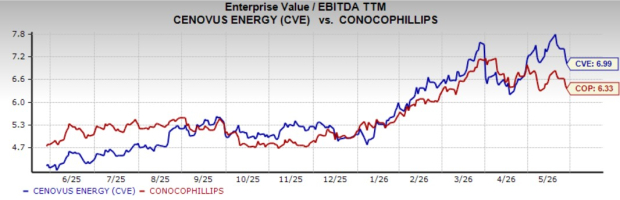

Valuation Snapshot

Considering the valuation snapshot, it has become evident that investors are now willing to pay a premium for Cenovus over ConocoPhillips, due to its future growth outlook and integrated business model. This is reflected in the fact that CVE trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 6.99X, above COP’s 6.33X.

Image Source: Zacks Investment Research

CVE vs. COP: Should You Buy or Hold?

Cenovus’s integrated business model is expected to provide a cushion to its profitability during volatile times. Moreover, the company is investing in multiple growth projects that significantly brighten its production outlook and cash flow growth expectations.

Since ConocoPhillips is a pure-play upstream energy player, its performance is significantly affected by the commodity pricing environment. COP is expected to benefit from the rise in oil prices in the near term. However, its operating results remain dependent on unpredictable macroeconomic and commodity-market factors.

Given the current macroeconomic environment and long-term growth outlook, investors may consider owning the CVE stock, which carries a Zacks Rank #1 (Strong Buy) at present. At the same time, while COP stands to gain from the current commodity environment, as a pure-play exploration and production company, its earnings are more directly related to volatile commodity-market conditions. So, investors who already own the stock can continue to hold COP stock, carrying a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ConocoPhillips (COP): Free Stock Analysis Report

Cenovus Energy Inc (CVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).