With a vast customer base spanning consumers, businesses, and government organizations, Verizon Communications Inc. (VZ) is a leading telecommunications provider focused on wireless services, broadband connectivity, and network security solutions. Headquartered in New York City, the company serves customers across the globe, including nearly all Fortune 500 companies, and generated $138.2 billion in revenue in 2025.

As emerging technologies reshape the digital landscape, Verizon is increasingly integrating artificial intelligence (AI) across its operations to enhance network performance, improve efficiency, and strengthen customer engagement. Combined with its expanding 5G infrastructure, these investments position the company to support the growing demand for data-intensive services and next-generation applications.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With a market capitalization of roughly $200.47 billion, Verizon ranks among the market’s mega-cap companies, a designation reserved for firms valued at $200 billion or more. Despite its dominant position in the telecommunications industry, Verizon's stock has struggled to keep pace with the broader industry rally.

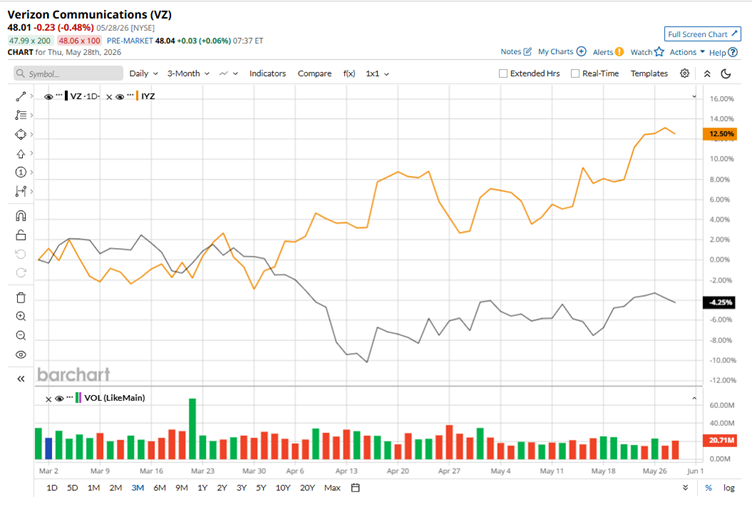

Shares are down 7.1% from their 52-week high of $51.68 reached on March 24 and have declined 4.3% over the past three months. By comparison, the iShares U.S. Telecommunications ETF (IYZ) has surged 12.5% over the same period, underscoring the gap between Verizon's performance and that of its industry peers.

www.barchart.com

www.barchart.com The longer-term performance tells a similar story. While Verizon shares have gained a respectable 11.3% over the past 52 weeks, the stock has significantly trailed the broader telecom industry. Over the same period, the iShares U.S. Telecommunications ETF has soared 58%, highlighting Verizon's inability to fully capitalize on the industry's strong momentum.

Verizon has remained comfortably above its 200-day moving average since late January, a sign of underlying long-term strength. However, the stock is currently trading just around its 50-day moving average, indicating that near-term momentum has been more subdued.

www.barchart.com

www.barchart.com Shares of Verizon climbed about 1.6% on April 27 after the telecom giant delivered a first-quarter earnings beat and raised its fiscal 2026 guidance, driven by stronger-than-expected postpaid subscriber growth and solid profit expansion. Total operating revenue rose 2.9% year over year to $34.4 billion, although it fell slightly short of the $35.03 billion consensus estimate.

The revenue miss was largely attributed to the company’s disciplined reduction in aggressive promotional activity, as well as a one-time 80-basis-point impact on wireless service revenue from customer credits issued following a major network outage in January. Despite the modest top-line shortfall, investors focused on the report’s brighter spots. Verizon posted adjusted earnings of $1.28 per share, up 7.6% from a year earlier and marking its strongest quarterly earnings growth since 2021.

The result also comfortably exceeded Wall Street’s expectation of $1.22 per share. However, the standout achievement was the company’s subscriber performance. Verizon reported a surprise net gain of 55,000 postpaid phone subscribers, its first positive first-quarter addition in that category since 2013, suggesting a meaningful improvement in customer momentum and competitive positioning.

Compared to its key telecom rival, Verizon's performance looks notably stronger. Over the past 52 weeks, Verizon has delivered a double-digit gain, while shares of AT&T Inc. (T) have declined 9.5% during the same time frame.

Despite its recent stretch of underperformance relative to the broader telecom industry, Wall Street remains constructive on Verizon's outlook. The stock carries a consensus “Moderate Buy” rating from 29 analysts, reflecting continued confidence in the company's fundamentals. Moreover, the average price target of $51.92 suggests about 6.1% upside from current levels, indicating analysts still see room for further gains ahead.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Marvell Technology Reports Strong FCF and Outlook - Could MRVL Move Higher? Palantir vs. Snowflake: Only 1 AI Software Stock Looks Strong for the Next Decade S&P Futures Gain on Hopes for U.S.-Iran Deal; Dell Pops on Blowout Earnings Ford Stock Is Moving Like Tesla Now. Its Results Can’t Justify the Premium.