The Montreal Canadiens play the Carolina Hurricanes in Game 5 of the NHL’s Eastern Conference final tonight in Raleigh. Down 3-1, I don’t hold out much hope for the sole remaining Canadian team in this year’s playoffs.

Hopefully, they win tonight in Carolina and Sunday in Montreal, forcing a Game 7, Montreal’s third consecutive seven-game series. We’ll see.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

On more pressing matters, Thursday’s options volume was about equal to its 90-day average of 61.65 million. Calls outnumbered puts by 1.6 times, with the top 100 stocks out of 4,462 accounting for 77% of the volume.

Boston Scientific (BSX) was one of yesterday’s stocks with above-average options and share volume. The former was 607,406, 11.5 times its 30-day average, while its share volume of 44.94 million was more than double its average volume.

Unsurprisingly, the medical devices stock had significant unusual options activity that included two of the top three Vol/OI (volume-to-open-interest) ratios and four over 10.0.

It’s been a while since I’ve seen such a high Vol/OI ratio. I might not be the sharpest tool in the drawer, but it can’t be a coincidence that the Dec. 18 $67.50 call and Dec. 18 $40 put’s Vol/OI ratios were so high.

The combination screams M&A. Here’s why.

Have an excellent weekend.

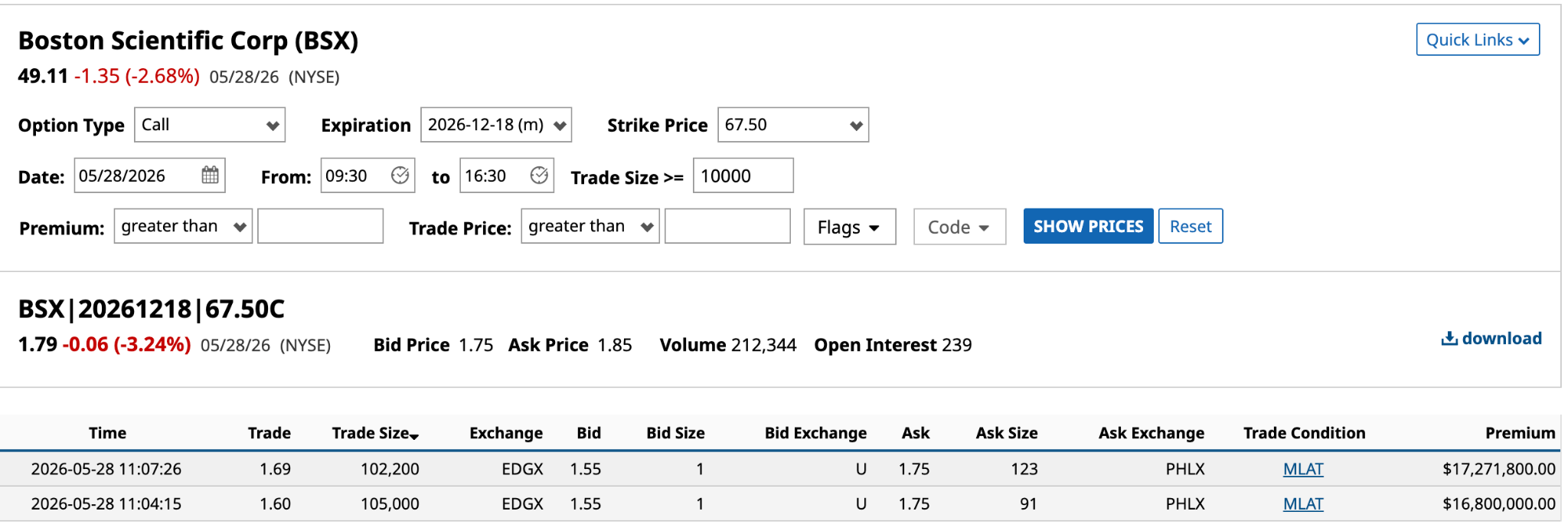

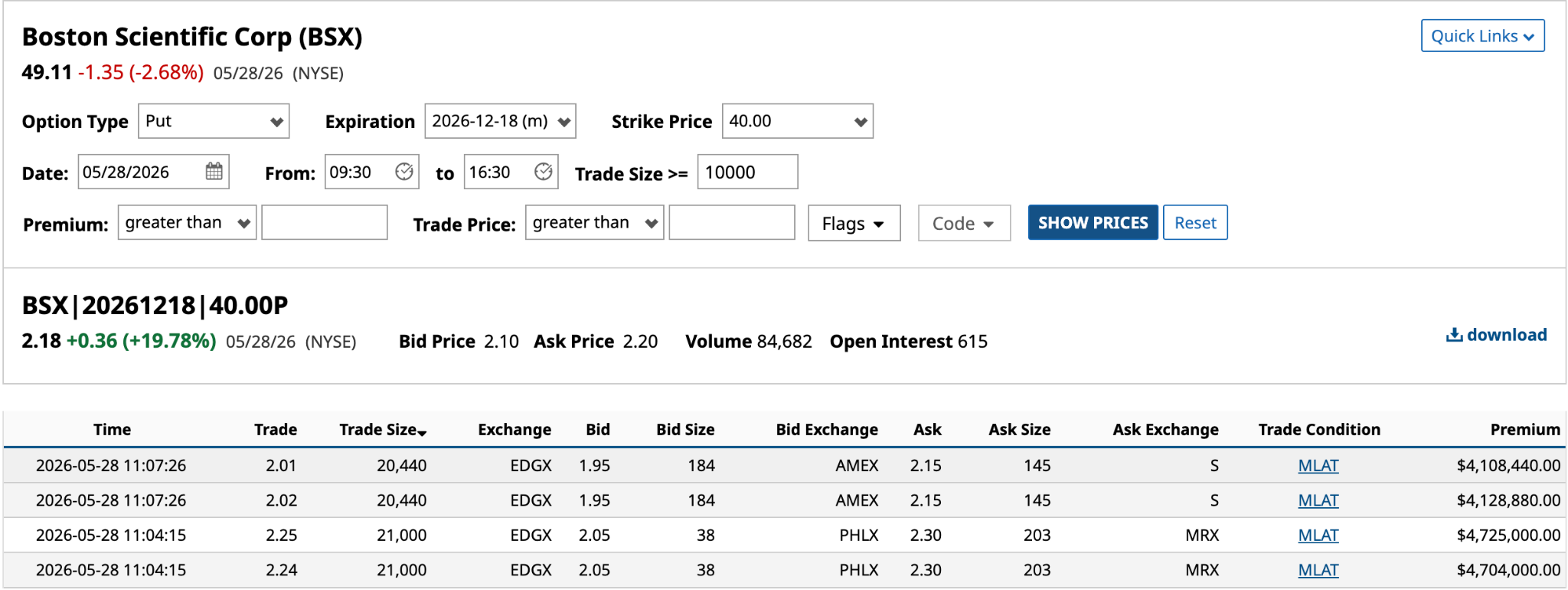

The BSX Options in Question

To put yesterday’s volume in context, 607,406 contracts traded was the highest daily amount in the past 12 months, 4.8 times higher than the second-highest volume of 126,575 on Jan. 20.

The call and put expiring on Dec. 18 in 205 days accounted for nearly 50% of the overall volume. Determining the possible options strategies at play involves a closer look at the trades for both options.

Here are the two notable call trades. One happened at 11:04 a.m. ET yesterday, while the other was three minutes later at 11:07. These two trades accounted for 97.6% of the contract volume for the Dec. 18 $67.50 call.

Here are the four notable put trades. Two happened at 11:04 a.m. ET yesterday, while the other two were three minutes later at 11:07. These four trades accounted for 97.9% of the contract volume for the Dec. 18 $40 put.

The M&A Angle

On Wednesday, BSX shares lost more than 12% due to a couple of reasons.

First, several analysts published bearish takes on the stock, while Wolfe Research analyst downgraded BSX from Outperform to Peer Perform, and Wells Fargo downgraded it to Hold from Strong Buy.

Secondly, and part of the reason some analysts were negative, was CEO Mike Mahoney's comments on Wednesday, suggesting that its Watchman device, used to close the left atrial appendage, was experiencing declining usage for stand-alone procedures.

BSX stock is now down nearly 49% year-to-date, trading at or near a three-year low. With investors skeptical about the company’s ability to meet its 2026 organic growth guidance of 7.3% at the midpoint, the downward pressure on its stock could persist for some time.

So, with its stock 55% off its September 2025 all-time high of $109.50, the institution making this big bet could know, or be speculating, that an offer from Johnson & Johnson (JNJ) or another large medical device company is interested in buying Boston Scientific at a time when its stock is cheap.

Conjecture, of course, but it’s not uncommon for a CEO to talk down a segment of its business when negotiating a sale to keep investors off the scent and potential buyers interested.

We’ll see soon enough.

Hedging Their Bet

Another possibility is that this big institution doesn’t know anything specific about a buyout but believes it could be a catalyst for upside by December, and already has a large position in BSX. The 207,200 calls are 2.5 times the 82,880 puts, indicating a bullish sentiment.

However, one of two things could be happening regarding the puts. Either the institution long on the calls was buying puts for downside protection, should the buyout thesis not materialize, or it was selling puts for premium to reduce the cost of the calls from $34.1 million to $16.4 million. It’s a cheap way to make a leveraged bet.

In either scenario, the institution is betting that a major catalyst is on the horizon.

The Bottom Line BSX Play

The options strategy at play here appears to be a Long Ratio Strangle, where the institution buys 10 calls for every 4 puts. The 207,200 call contracts divided by 10 equals 20,720; the 82,880 call contracts divided by 4 equals 20,720 units. The math works.

In a standard Long Strangle, the investor buys one call and one put. Below is the BSX data as of early Friday morning. As you can see, its share price has dropped slightly from yesterday’s close. The net debit of $4.60 is below 10% of the share price, which is ideal leverage.

To make money on this strategy, the share price in December must be above the $72.10 upside breakeven or below the $35.40 downside breakeven. The expected 22.13% move suggests that only a buyout will deliver the premium necessary to make money. The implication is that the institution expects an offer of more than $72.10 per share.

Let’s assume someone makes a $90-per-share offer, an 84% premium over its current share price. I don’t know BSX well enough to make an educated guess at what a fair price should be. Let’s assume $90 is fair.

The profit on this standard strangle would be $1,790 [$90 share price - $67.50 call strike - $4.60 net debit * 100 shares].

The profit on the institution's bet requires a little more legwork.

1) The 10:4 ratio’s cost per unit would be $3,130 [(10 calls @ $2.15 = $21.50 * 100 = $2,150) + (4 puts at $2.45 = $9.80 * 100 = $980)].

2) As mentioned earlier, there are 20,720 units.

3) The profit per call contract is $2,035 [$90 share price - $67.50 strike price - $2.15 call cost * 100]. The profit for 10 calls is $20,350.

4) The 4 puts expire worthless for a $980 loss.

5) The net profit per unit is $19,370 [$20,350 - $980].

So, the total profit is $401.35 million, a return of 618.4% based on a cost of $64.9 million [$3,130 per unit * 20,720], or 1,111.9% annualized.

No risk. No reward.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Unusual Options Activity Points to Boston Scientific Stock as a Hot M&A Target Marvell Technology Reports Strong FCF and Outlook - Could MRVL Move Higher? Unusual Options Activity in Key ETFs Unveils 3 Trade Ideas Here Amazon Max Pain Points to a Price of $235 by June 18th