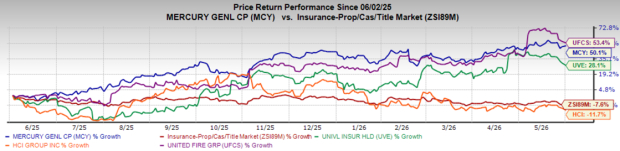

Shares of Universal Insurance Holdings, Inc. UVE have risen 28.1% in the past year, outperforming the industry’s decline of 7.6% and the Finance sector’s growth of 12.2%. However, the stock has lagged the Zacks S&P 500 composite’s gain of 33.9% over the same timeframe.

Strong earnings growth, lower loss ratios, secured reinsurance coverage and disciplined underwriting have boosted investor confidence. UVE is set to gain from Florida’s improving post-reform loss environment, while its disciplined underwriting strategy continues to support strong unit economics and selective growth opportunities.

Image Source: Zacks Investment Research

Some of Universal Insurance's peers include HCI Group, Inc. HCI, United Fire Group, Inc. UFCS and Mercury General Corporation MCY. Shares of HCI have lost 11.7%, while UFCS and MCY have rallied 53.4% and 50.1%, respectively, in the past year.

UVE’s Expensive Valuation

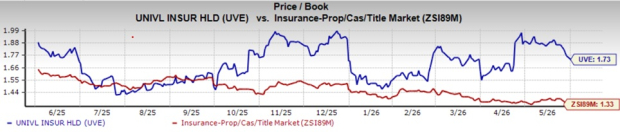

UVE’s shares are trading at a premium compared with the industry. Its forward price-to-book value of 1.73X is higher than the industry average of 1.33X.

Image Source: Zacks Investment Research

UVE’s Earnings & Growth Outlook

The Zacks Consensus Estimate for Universal Insurance’s 2026 revenues is pegged at $1.54 billion, implying a year-over-year decrease of 3.7%.

The consensus estimate for 2027 revenues and EPS indicates an increase of 1.5% and 1.6%, respectively, from the corresponding 2026 estimates.

The company’s earnings have improved 79.6% in the past five years, better than the industry average of 22.3%.

Optimistic Analyst Sentiment on UVE

The consensus estimate for 2026 and 2027 has moved 18.7% and 10% north, respectively, in the past 30 days, reflecting analysts’ optimism.

UVE’s Favorable Return on Capital

Return on equity for the trailing 12 months was 31.5%, which compared favorably with the industry’s 6%. This reflects its efficiency in utilizing shareholders’ funds.

Return on invested capital in the trailing 12 months was 24.3%, better than the industry average of 5.7%, reflecting UVE’s efficiency in utilizing funds to generate income.

Key Points to Note for UVE

UVE's disciplined underwriting framework remains a key competitive advantage. The company continues to open and close markets using internal profitability models, reinforcing underwriting discipline and mix quality. Management emphasized that it is prioritizing rate adequacy over volume growth. Strong agency relationships and ongoing rate analysis should enable the company to balance growth, pricing and margins while maintaining confidence among reinsurance partners.

The company also strengthened its risk management profile through the successful completion of its 2026-2027 reinsurance renewal. Management reported the 2026-2027 reinsurance renewal is fully supported and secured, and that the company also added $352 million of multi-year coverage extending into the 2027-2028 treaty period. Retentions are expected to remain unchanged at $45 million, with the captive structure continuing to cover the $66 million layer above retention for the first event. Management expects to provide pricing details soon, which should frame how much of the better loss environment can flow through to earnings stability across the upcoming hurricane seasons.

UVE’s top-line momentum was driven by broad-based premium expansion across its footprint. Direct premiums written increased 8.5% year over year to $506.5 million, driven by 4.9% growth in Florida and 18.3% growth in other states. The stronger expansion outside Florida reflects continued execution of UVE's diversification strategy, which helps reduce catastrophe concentration risk while broadening growth opportunities.

Florida's legislative reforms continue to support underwriting profitability through lower litigation frequency and severity. As a result, the net loss ratio improved 6.6 percentage points year over year to 63.9%, while the net combined ratio improved to 89.7% from 95.0% in the first quarter of 2026. These trends contributed to a strong underwriting performance. Management referenced continuing benefits from the legislative environment.

UVE continues to pair regular dividends with opportunistic repurchases while prioritizing capitalization of the insurance entities. With the reinsurance program secured for 2026-2027 and extended multi-year protection, management retains flexibility to balance growth, volatility protection and ongoing capital returns.

Conclusion

Healthy policy retention, selective market positioning and steady policy growth should support profitable expansion. Strong capital levels, along with dividends and share repurchases, make UVE a strong contender for being in one’s portfolio. The Zacks average price target is $44 per share, suggesting a potential 18.9% upside from the last closing price.

Coupled with premium expansion, secured reinsurance, optimistic analyst sentiment and higher return on capital, the time appears right for potential investors to bet on this Zacks Rank #1 (Strong Buy) insurer. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United Fire Group, Inc (UFCS): Free Stock Analysis Report

HCI Group, Inc. (HCI): Free Stock Analysis Report

Mercury General Corporation (MCY): Free Stock Analysis Report

UNIVERSAL INSURANCE HOLDINGS INC (UVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).