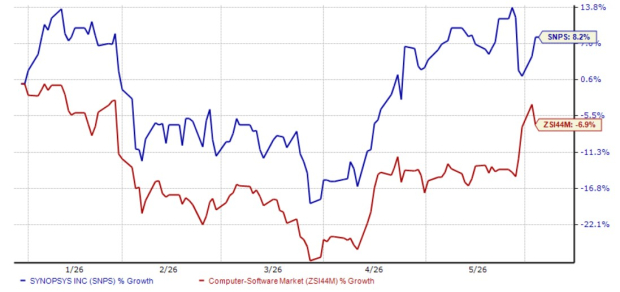

Synopsys, Inc. SNPS shares have appreciated 8.2% year to date, outperforming the Zacks Computer - Software industry’s decline of 6.9%.

SNPS YTD Performance Chart

Image Source: Zacks Investment Research

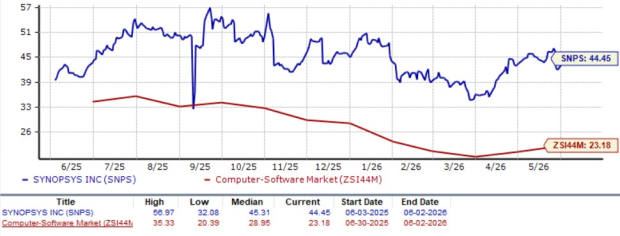

The outperformance in the stock price led to a premium valuation, with SNPS stock trading at a P/E multiple of 44.45x, much above the industry P/E multiple of 24.02x. The premium valuation is further established by the Zacks Value Score of F.

SNPS Forward 12-Month Valuation Chart

Image Source: Zacks Investment Research

Given these dynamics, investors are wondering if it’s the right time to buy, sell or hold the stock? Let’s dive into the fundamentals and financials of the stock and discuss what investors should do with SNPS right now.

SNPS’ Design IP Business is Under Pressure

Synopsys gains from multi-trillion-dollar AI infrastructure buildout, driving strong system-level and semiconductor R&D spending and robust AI compute design activity. Synopsys is embedding AI across its product portfolio to automate engineering workflows and improve customer productivity.

While generative AI could disrupt software companies. Synopsys gains from decades of deep engineering expertise, proprietary codebases and solvers, silicon-proven design technologies and foundry co-optimization capabilities. The company has been able to provide its customers with up to 50% faster knowledge assistance, 70% faster workflow assistance and 5x faster formal testbench generation.

Despite strength in some parts of its portfolio, SNPS’ Design IP segment faced pressure in the second quarter of fiscal 2026. Revenues declined to $454.2 million from $482 million in the year-ago quarter, while adjusted operating margin fell to 24% from 31%. The weakness was not limited to a single quarter, as the segment’s adjusted operating margin for the first six months of fiscal 2026 was 21%, down from 30% in the same period last year.

Synopsys continues to carry a sizable debt load following its recent acquisitions and strategic investments. As of April 30, 2026, the company had $10.014 billion in long-term debt, compared with $2.484 billion in cash, cash equivalents and short-term investments. The debt burden is contributing to higher financing costs, affecting the bottom line.

The Zacks Consensus Estimate for SNPS’ fiscal 2026 earnings is pegged at $14.49, indicating 12% year-over-year growth. Estimates have been revised upward in the past seven days.

Image Source: Zacks Investment Research

SNPS Faces Stiff Competition in EDA Space

The company faces tough competition from EDA vendors, such as Cadence Design Systems Inc. CDNS, Keysight Technologies KEYS and Siemens SIEGY. These companies offer products focused more on distinct phases of the IC design process and provide a range of services to companies throughout the world to help optimize their product development process, among other things.

Keysight Technologies competes in the electronic design and testing space, particularly providing software solutions for electromagnetic analysis, circuit simulation and hardware verification. Cadence benefits from higher design complexity and rising customer spend on AI-driven automation.

Amid rapid AI proliferation, the Cadence.ai portfolio has been gaining strength, and the new product launches like AgentStack, along with ChipStack, ViraStack and InnoStack AI Super Agents, are expected to aid in sustaining the momentum. Siemens EDA, Siemens' electronic design automation division and Cadence Design Systems both provide EDA tools, including software, hardware and services essential for designing chips and semiconductor devices.

Conclusion

Synopsys remains well-positioned to benefit from the accelerating AI-driven semiconductor and infrastructure spending cycle, supported by its strong EDA leadership. However, investors should not ignore the challenges. The weakness in the Design IP business, margin compression, a significantly higher debt burden and intense competition from Cadence, Keysight and Siemens EDA could weigh on near-term performance. Moreover, the stock’s premium valuation leaves limited room for execution missteps. Considering these factors, we suggest that investors should stay away from this Zacks Rank #4 (Sell) stock at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Synopsys, Inc. (SNPS): Free Stock Analysis Report

Cadence Design Systems, Inc. (CDNS): Free Stock Analysis Report

Siemens AG (SIEGY): Free Stock Analysis Report

Keysight Technologies Inc. (KEYS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).