Innodata Inc. INOD is demonstrating that artificial intelligence growth can be far more than a revenue story. The company’s first-quarter 2026 results showed how its expanding role in the AI ecosystem is translating into higher profitability, stronger margins and accelerating cash generation.

Revenue surged 54% year over year to a record $90.1 million, driven by growing demand from frontier AI labs, hyperscalers and enterprise customers. However, the more important development was that profits grew even faster than sales. Adjusted EBITDA nearly doubled year over year to $25 million, while adjusted EBITDA margin expanded to 28% of revenue. Adjusted gross margin reached 47%, well above management’s long-term target of 40%.

Management attributes this margin expansion to a shift toward higher-value AI services such as expert-grade training data, model evaluation, trust and safety testing, agent optimization and AI observability platforms. These offerings require specialized expertise and create greater pricing power than traditional data services. Innodata is also increasingly monetizing proprietary datasets and software-like platforms that can be reused across customers, reducing reliance on linear headcount growth and improving scalability.

The company’s strategy is benefiting from customer diversification as well. Revenues from non-core Big Tech customers grew 453% year over year, while a new leading technology customer is expected to generate roughly $51 million of revenues in 2026 and become Innodata’s second-largest customer.

Perhaps most encouraging for investors, Innodata generated $37.3 million in operating cash flow during the quarter and ended March with $117.4 million in cash. Supported by stronger visibility and growing demand, management raised its 2026 revenue growth outlook to approximately 40% or more.

The takeaway is clear: Innodata is not merely benefiting from the AI boom. It is increasingly converting AI demand into sustainable profit growth, expanding margins and stronger cash generation.

How Innodata Compares With Key AI Data Rivals

Among Innodata’s closest competitors are TaskUs TASK and Concentrix CNXC, both of which provide AI-related data, trust and safety and digital operations services to large technology customers. However, Innodata is increasingly differentiating itself by moving deeper into high-value AI workflows.

Concentrix has been expanding its AI capabilities through automation, data services and digital transformation offerings. Concentrix benefits from its large enterprise customer base and global delivery network. However, Concentrix remains heavily focused on customer experience management and business process services, which generally carry lower growth and margin potential than specialized AI development work.

TaskUs is also expanding its AI services portfolio, particularly in trust and safety, content moderation and AI data operations. TaskUs benefits from relationships with leading technology companies and has invested heavily in AI-related services. Yet TaskUs remains more exposed to traditional outsourcing activities, making its growth profile less directly tied to frontier AI model development.

In contrast, Innodata is increasingly focused on expert-grade training data, model evaluation, AI safety testing, agent observability and proprietary AI platforms. These higher-value services helped drive significant margin expansion and operating leverage in the latest quarter. As AI models become more complex, Innodata’s specialization may allow it to capture a larger share of industry profit pools than Concentrix and TaskUs.

INOD’s Price Performance, Valuation & Estimates

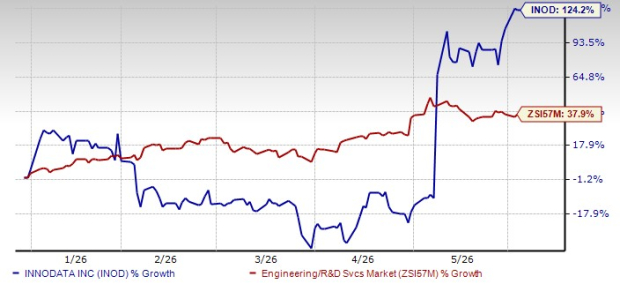

Shares of Innodata have gained 124.2% year to date (YTD), outperforming the industry’s 37.9% growth.

INOD YTD Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, INOD trades at a forward 12-month price-to-earnings ratio of 86.31, higher than the industry’s average.

INOD Valuation - P/E (F12M)

Image Source: Zacks Investment Research

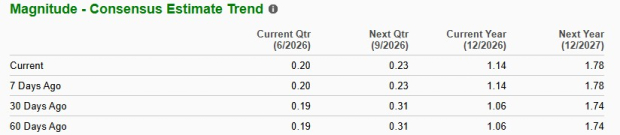

The Zacks Consensus Estimate for INOD’s 2026 sales and earnings implies a year-over-year uptick of 40.6% and 23.9%, respectively. EPS estimates for 2026 have increased to $1.14 in the past 30 days, as shown below.

Image Source: Zacks Investment Research

INOD currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Innodata Inc (INOD): Free Stock Analysis Report

Concentrix Corporation (CNXC): Free Stock Analysis Report

TaskUs, Inc. (TASK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).