Cerebras Systems (CBRS) has already claimed the spotlight in a year many expect to rank among the busiest Initial Public Offering (IPO) markets in recent memory. The artificial intelligence (AI) data center semiconductor company sparked intense investor interest from day one, largely because many believe it could eventually capture the kind of rich profit margins that have turned Nvidia Corporation (NVDA) into the industry's gold standard.

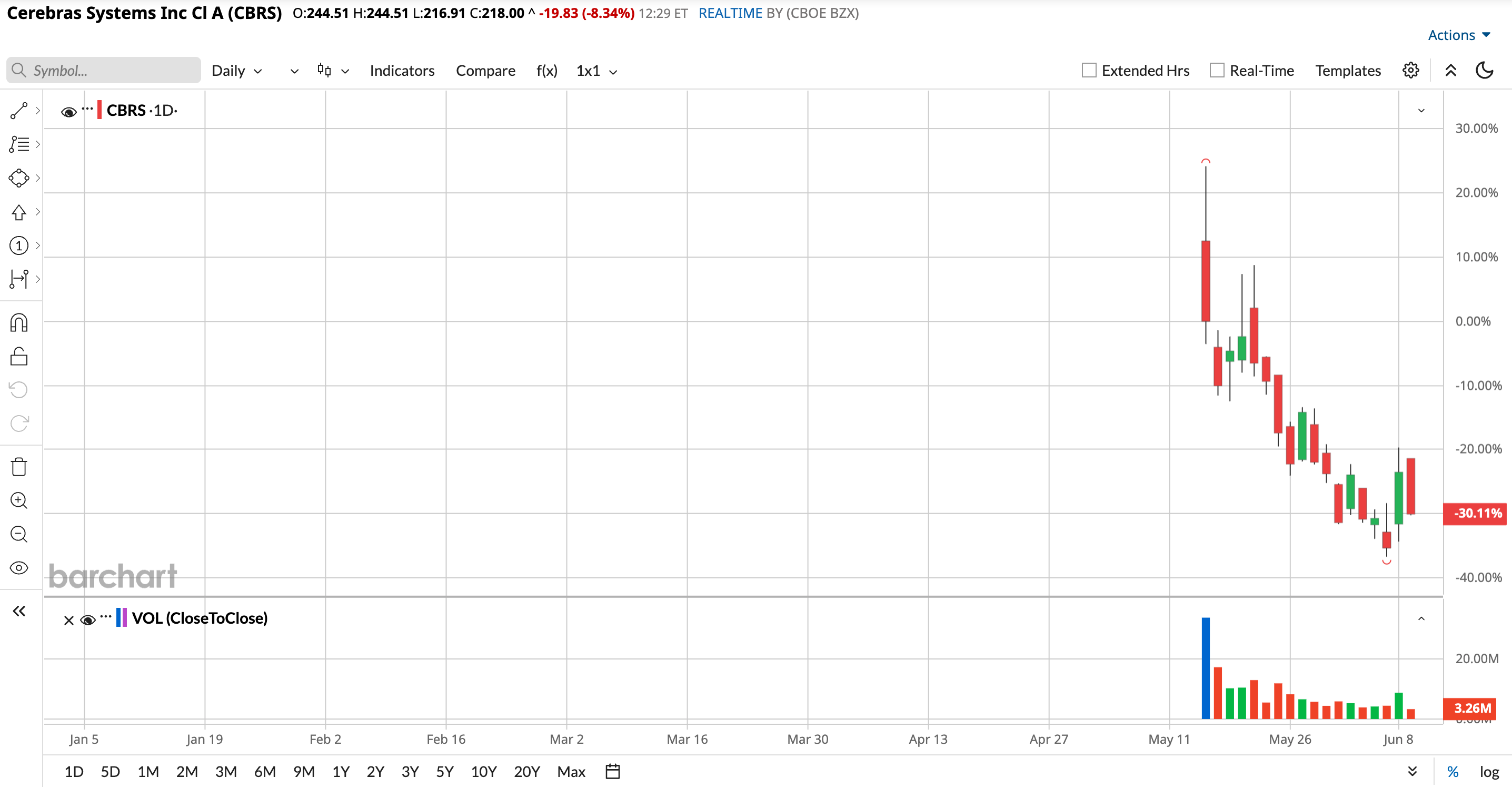

The company priced its IPO at $185 per share and trading opened at $350. The stock then raced to an intraday high of $386 before ending its debut session at $311. The weeks that followed brought a pullback, though several sharp rallies kept traders on their toes.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

However, Cerebras’ shares surged 18.3% on Monday, June 8, as analysts lined up behind the stock with unusually strong conviction. Research firms repeatedly described Cerebras as one of the most credible challengers to Nvidia’s dominance, citing its wafer scale architecture along with a multibillion-dollar backlog as major engines for future growth.

A common thread which ran through nearly every new research report is that analysts see Cerebras holding a meaningful edge in fast inference, the technology responsible for running live AI models after training.

About Cerebras Stock

Most chipmakers connect thousands of smaller graphics processing units (GPUs) to handle AI workloads. Cerebras Systems chose a very different path. Founded in 2015 and based in Sunnyvale, California, the company builds wafer scale chips roughly the size of a dish. According to Cerebras, these processors handle AI inference workloads much faster than Nvidia’s graphics processing units.

Inference serves as the stage where AI generates answers, predictions, or outputs after completing training. Businesses increasingly rely on inference across a growing number of applications, which gives faster and more efficient systems a potentially powerful competitive advantage.

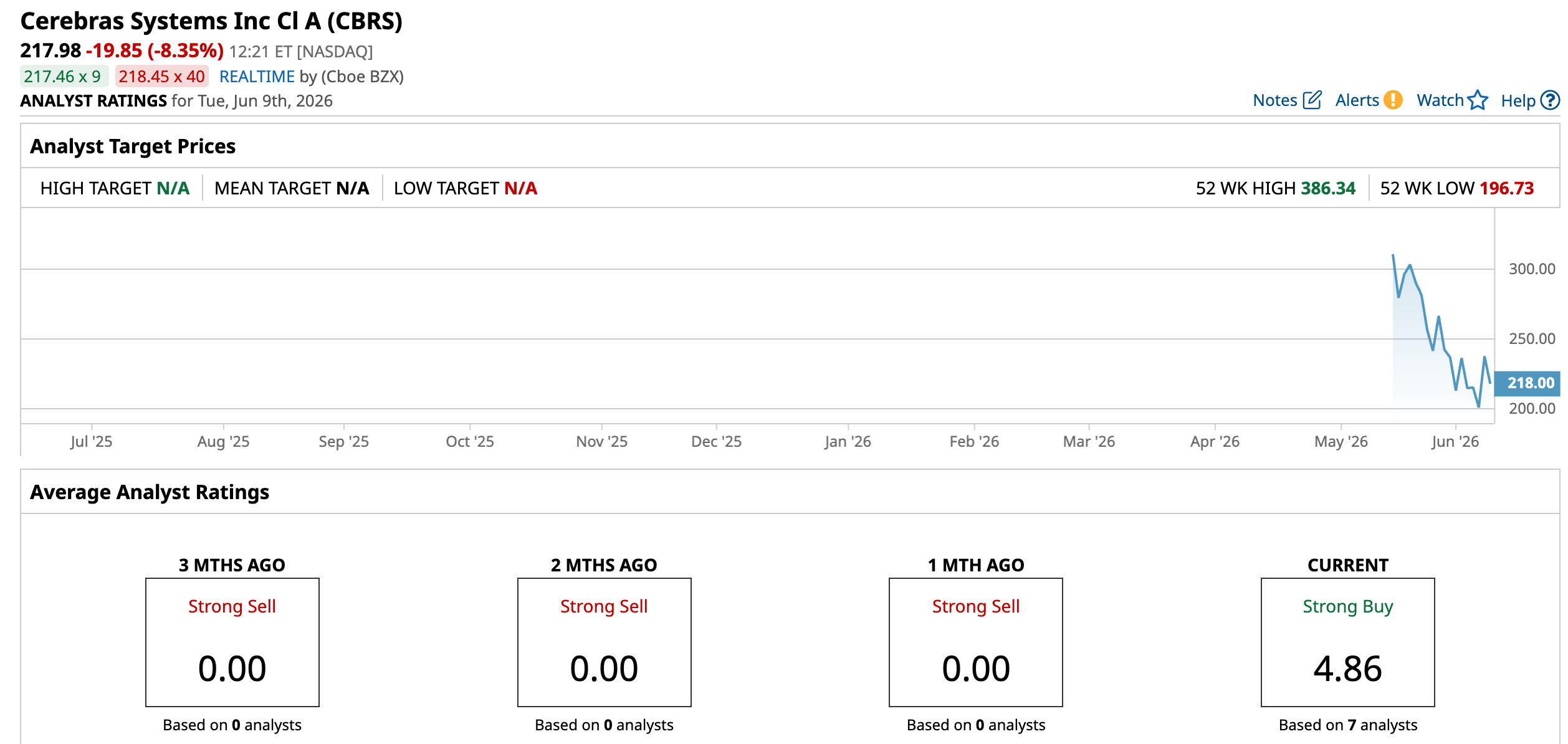

Cerebras also argues that its technology delivers better economics once hardware expenses along with operating costs enter the equation. The chipmaker now carries a market cap of $51.2 billion, but its stock has slumped 8.25% over the past five trading days.

www.barchart.com

www.barchart.com Needham Sees a Massive Opportunity Ahead

Among the firm's biggest supporters sits Needham analyst N. Quinn Bolton. He launched coverage with a “Buy” rating along with a $300 price target which suggests a gain of 38.3% from current price levels. Bolton highlighted that Cerebras stands alone as the only company currently producing Wafer Scale Engines, a category of AI processors built from one massive piece of silicon.

Those chips pack significantly greater on chip memory along with bandwidth than competing designs. That advantage makes them particularly effective for fast inference workloads such as real time coding assistants and instant research agents.

Needham's bullish view rests on several long-term catalysts. In January, Cerebras unveiled a compute agreement with OpenAI worth more than $20 billion. The deal calls for OpenAI to deploy approximately 750 megawatts of Cerebras compute capacity through 2028.

OpenAI holds an option to expand that commitment by another 1.25 gigawatts. Needham believes that decision could dramatically reshape the company's revenue outlook if OpenAI chooses to exercise the expansion option.

The firm pointed to Cerebras' collaboration with AWS announced in March. The partnership focuses on disaggregated inference. Needham believes meaningful system deliveries to Amazon.com (AMZN) could place the company's growth story into an even higher gear.

What Do Other Analysts Expect for Cerebras Stock?

Morgan Stanley analyst Joseph Moore described Cerebras as a rare opportunity for investors seeking exposure to an AI processor company with a first mover advantage against Nvidia. Thus, Moore raised his price target from $201 to $250 while maintaining a “Buy” rating on the stock.

Meanwhile, Rosenblatt Securities sees the OpenAI and AWS partnerships as the spark behind a major revenue acceleration. The firm noted that Cerebras expanded annual revenue from just $25 million in 2022 to $510 million in 2025. Projections point to revenue reaching $6.8 billion by 2028. Hence, analyst Kevin Cassidy initiated coverage with a “Buy” rating along with a $300 price target.

UBS analysts led by Timothy Arcuri also joined the chorus. The firm described Cerebras as a fast inference pure play with a growing backlog. UBS highlighted the company's Wafer Scale Engine as the largest compute chip in the world, arguing that it delivers a performance edge over GPUs across select fast inference applications that serve a premium segment of the market. UBS maintains its “Buy” rating along with a $300 price target.

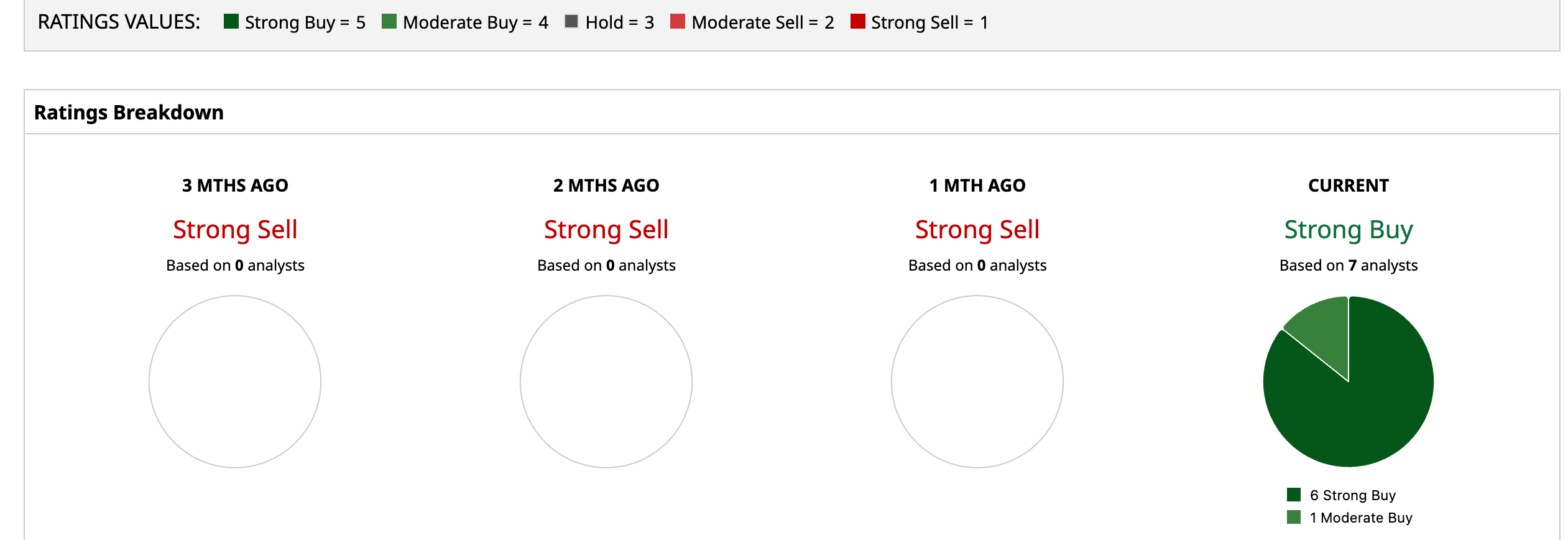

Wall Street has thrown its weight behind the stock, assigning it an overall rating of “Strong Buy.” Among seven analysts covering the stock, six rate it a “Strong Buy,” while one recommends a “Moderate Buy.”

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Oracle Stock Is Careening Toward Earnings with a Heavy $100 Billion Weight on Its Back Wedbush Thinks Cerebras Stock Is Ready for More Upside as CBRS Debuted at Just the Right Time This Analyst Just Upgraded Crocs Stock. Here's Why. Why Needham Analysts Think Cerebras Stock Can Gain Another 25% After Historic IPO