Volatility can be an option trader's best friend or worst enemy, depending on how it's approached.

High implied volatility rank signals that options prices are elevated compared to their historical norms, creating unique opportunities for those who know how to capitalize on them.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

Whether you're selling premium to take advantage of inflated option prices or seeking sharp price swings for directional trades, understanding which stocks have unusually high IV is crucial.

To get an accurate picture of stocks with a high implied volatility rank, we can use the Stock Screener.

These elevated readings suggest the options market is pricing in significant potential price movements, whether due to upcoming earnings announcements, sector-specific developments, or broader market dynamics.

For traders considering volatility-based strategies, these stocks warrant particular attention as they may offer enhanced premium collection opportunities, though careful position sizing and risk management remain crucial.

Using The Stock Screener To Find High Volatility Stocks

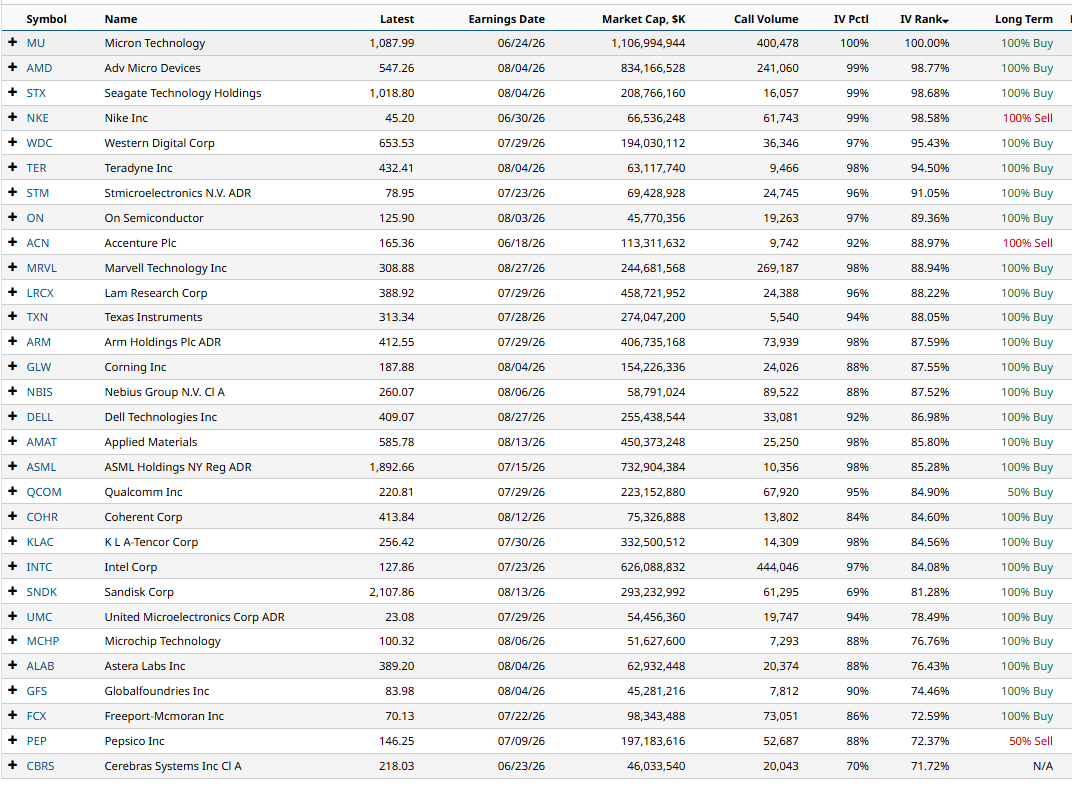

We currently have 30 stocks showing an IV rank above 70.

We can set the following filters using the Stock Screener to find stocks with a high implied volatility rank.

Total Option Volume 10,000 Market Cap greater than 40 billion IV Rank greater than 70%This screener gives us the following stocks ranked from highest IV rank to lowest:

How To Use IV Rank

Generally, when implied volatility rank is high, focusing on short volatility trades such as iron condors, short straddles, and strangles is better.

It’s also a good idea to watch the upcoming earnings dates as stock can make big moves following earnings announcements.

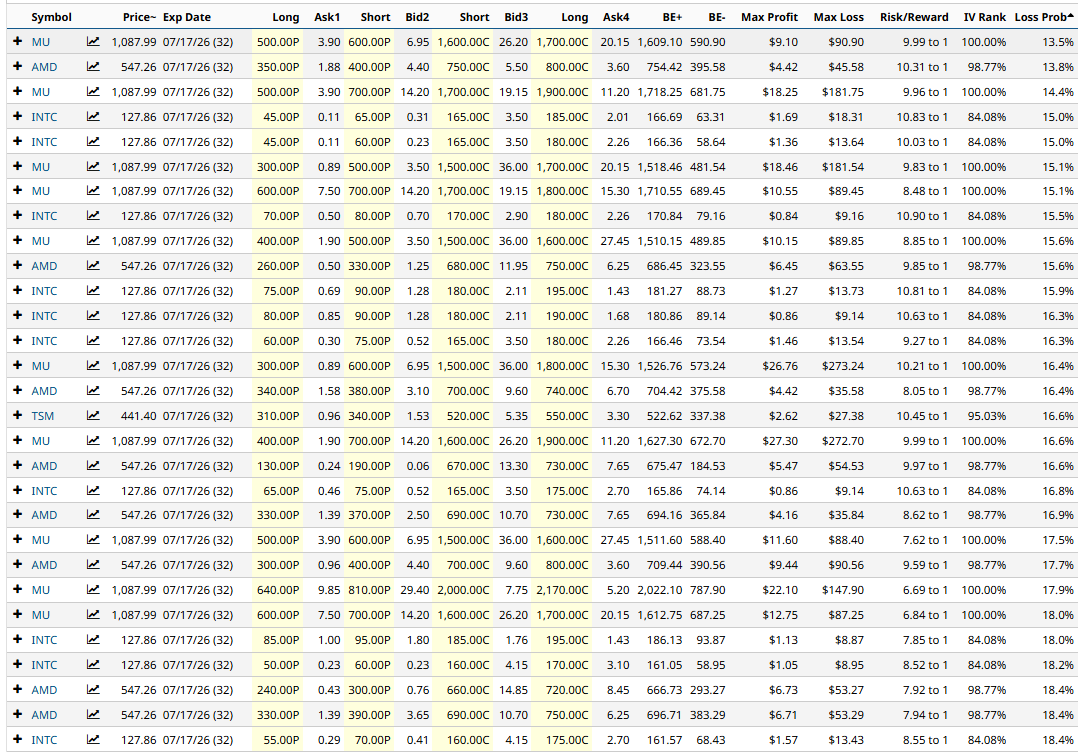

Iron Condor Screener

Let’s run an iron condor screener for the above stocks and analyze the results.

Let’s look at the first line item on Micron Technology (MU).

Using the July 17 expiry, the trade would involve selling the $600 put and buying the $400 put. Then on the calls, selling the $1,600 call and buying the $1,700 call.

The price for the condor is $9.10 which means the trader would receive $910 into their account. The maximum risk is $9,090 for a Risk/Reward ratio of 9.99 to 1 with a Loss Probability of 13.5%.

The profit zone ranges between $590.90 and $1609.10. This can be calculated by taking the short strikes and adding or subtracting the premium received.

Micron Technology is due to report earnings on June 24, so this trade would have earnings risk if held to expiration.

Please remember that options are risky, and investors can lose 100% of their investment. This article is for education purposes only and not a trade recommendation. Remember to always do your own due diligence and consult your financial advisor before making any investment decisions.

On the date of publication, Gavin McMaster did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Volatility Alert: 30 Stocks Showing a High IV Rank Autodesk Stock At Recent Lows Spurs Unusual Put Options Activity - Is ADSK Too Cheap? ConocoPhillips Has Attractive Short-Put Yields over 1% for the Next Month Options Action: Naked Put Trade Ideas for June 15th