The news of a deal between the U.S. and Iran to reopen the Strait of Hormuz sent markets higher yesterday. The S&P 500 and Nasdaq Composite gained 1.65% and 3.07%, respectively.

While the mood was positive on Wall Street, there were bearish price surprises alongside the bullish ones.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Leading the way higher was Regentis Biomaterials (RGNT), up 526.7%, with a standard deviation of 4.12. On the downside, the stock with the highest standard deviation was Elicio Therapeutics (ELTX), at 4.45, down 72.53%.

I’ve given up on harping about how expensive stocks are. If investors want to pay 40.5 times earnings -- I’m using the Shiller PE ratio, which is the current price divided by the 10-year moving average of inflation-adjusted annual earnings per share -- the last time it was this high was at the end of 1999 and the dot.com bubble. Before that? Never.

The bulls will argue that times are different and public companies are more profitable than they were back then. For everyone’s sake, I hope that remains the case.

Yesterday, one of the 200 bearish price surprises that caught my eye was EPR Properties (EPR), with a standard deviation of 1.99% and a 2.49% price drop.

If you’re an income-focused investor, EPR stock is an excellent long-term hold. Here are three reasons why.

Movie Theaters Are Just One Revenue Generator

Originally known as Entertainment Property Trust, the REIT was incorporated in August 1997 and went public in November 1997, selling 13.8 million shares at $20 each.

The REIT’s first acquisition was the purchase of 12 megaplex theatres from AMC Entertainment (AMC) for $249 million. It also had an option to buy five more from AMC for $139 million.

The original executives of EPR were involved in AMC’s management. AMC had looked for a REIT to help it finance growth. When it couldn’t find one, it started one. In addition to AMC theaters, it planned to own those run by competitors. Today, the REIT owns 148 properties operated by 17 movie exhibitors. They account for 36% of its annual adjusted EBITDAre (earnings before interest, taxes, depreciation and amortization for real estate).

It continues to move away from a reliance on movie theaters. It changed its name to EPR Properties in November 2012 to reflect its diversification moves.

“While Entertainment continues to be our largest segment, over the years we have strategically expanded the types of specialty segments in which we invest. Our new name leverages our brand heritage and provides the necessary latitude to encompass a broader set of specialty categories,” CEO David Brain said in a press release at the time. He was one of the original managers of EPR and retired in March 2015.

While the REIT began pushing into education in 2007, these properties account for just 6% of its annual EBITDAre. The rest -- 280 properties run by 54 operators, including AMC, Cinemark (CNK), and TopGolf -- is experiential.

Remarkably Consistent Revenue and FFO Generation

In the past 10 years, it has increased its revenue in eight of those years, from $418.4 million in 2015 to $714 million in 2025—the two down years: 2020 (COVID) and a slight decline in 2024. As for FFO (Funds From Operations), they increased by 63% over the past decade from $235.2 million in 2015 to $383.8 million, with three down years in 2019, 2020, and 2024.

Meanwhile, its total debt-to-EBITDA ratio has barely budged, up two basis points to 5.7x from 5.5x. Further, it ended Q1 2026 with total debt of $2.9 billion, 99% of which was unsecured, and a weighted average interest rate of 4.4%. Over the next six years, it will have no more than $550 million maturing in any given year, with a $1 billion unsecured revolving credit facility that’s undrawn.

So, it has the financial flexibility to pursue an acquisition when the price is right and cash flow is sufficient.

In early May, at the same time it announced Q1 2026 results, it raised its 2026 adjusted FFO per share guidance from $5.38 at the midpoint to $5.45. It shares trade at just 10.7 times that estimate.

EPR Continues to Invest Wisely

On April 6, the REIT closed six of the seven amusement parks it acquired from Six Flags Entertainment (FUN) for $315 million. The six are all regional parks in the U.S. The seventh, Six Flags La Ronde in Montreal, Canada, should close by the end of June.

In 2026, it expects to invest between $500 million and $600 million in new properties. Given its $7.1 billion investment across 335 locations, that’s less than a 10% increase, but it’s enough to keep growing its cash flow to pay its generous dividend.

It last increased its monthly dividend by 5.1% to $0.31 a share, up from $0.2950 with the April 2026 payment – the annual rate of $3.72 yields a healthy 6.3%. In 2025, it paid out $290.7 million in dividends to shareholders. That’s just 73% of its $398.2 million in adjusted funds from operations.

That’s just part of the compelling story that is EPR.

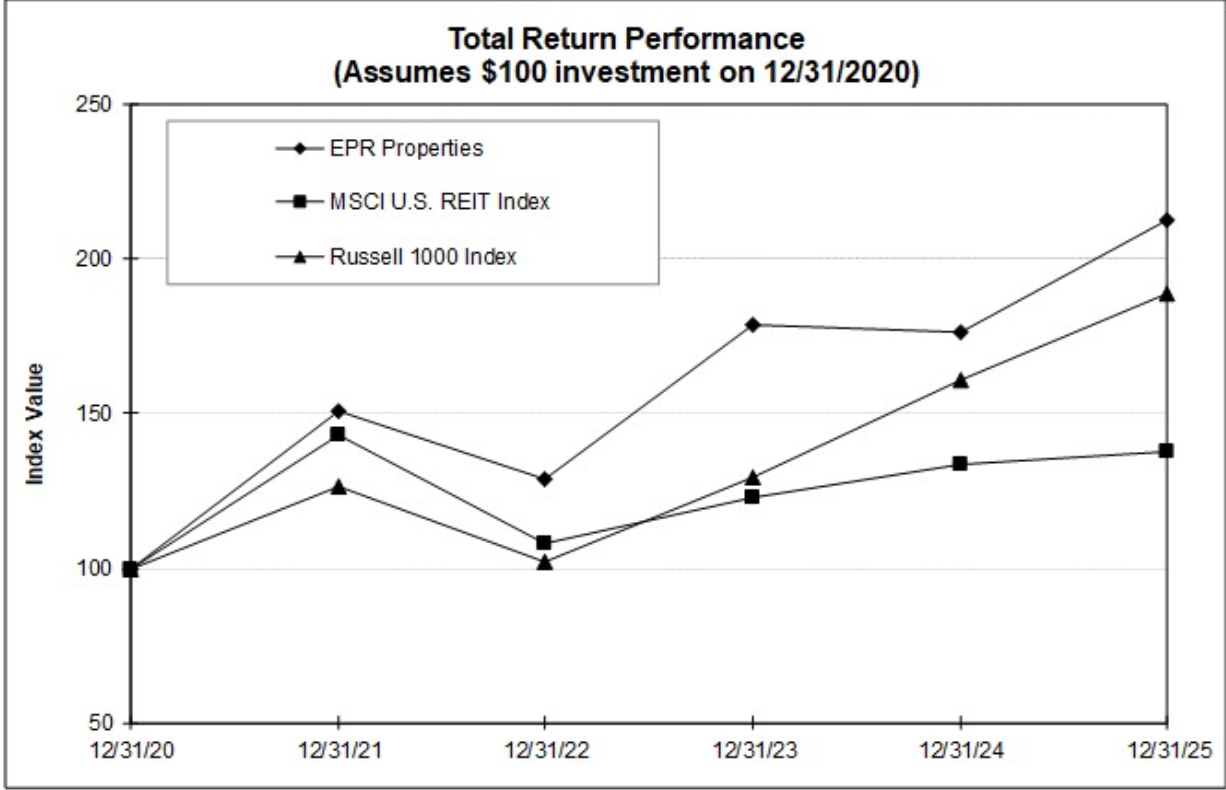

Source: S&P Global Market Intelligence, EPR’s 2025 10-K

Between the end of 2020 and 2025, EPR delivered a cumulative total return of 112.46%, considerably higher than the 37.53% total return for the MSCI U.S. REIT Index and the 89.1% total return for the Russell 1000 Index.

There are going to be times when you’ll be happy about EPR’s generous monthly dividend and times when you’ll be happy about its capital appreciation.

I see the next 2-3 years being the best of both worlds for EPR shareholders.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Unusual Put Options Activity in Lam Research Stock Highlights Its Value This Monthly Dividend Powerhouse Is Trading at a Bargain-Bin Valuation Dear Honeywell Stock Fans, Mark Your Calendars for June 29 The Risk of ‘Unproven Outcomes’ Has This Analyst Betting SpaceX Stock Will Fall 30% from Here