With many households still feeling stretched with higher prices, Costco Wholesale (COST) just lowered the price tags on some of its top Kirkland Signature products. In an attempt to alleviate price strain, the company said four items would see price cuts between $1 and $10. These items are Kirkland Signature Crispy Wings (dropped from $16.99 to $14.99), Kirkland Signature Milk Chocolate Almonds (dropped from $19.99 to $18.99), Kirkland Signature golf balls (dropped from $32.99 to $29.99), and Kirkland Signature king-size sheets (dropped from $89.99 to $79.99).

While these small price cuts on items won’t transform budgets overnight, they can help American consumers who are already feeling inflationary pressures. After all, the Consumer Price Index (CPI) was up by 0.5% in May, sending the annual inflation rate to 4.2% compared to the 3.8% reported in April. According to a CNN poll, 76% of Americans also say that cost of living is a major concern.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With that in mind, let's take a closer look at what's going on with Costco right now.

www.barchart.com

www.barchart.com Even the Smallest Price Cuts Can Help Both Consumers and Costco

Costco's recent price cuts could help drive more traffic to the store as well as drive new memberships and membership renewals, which are actually what powers the company's profits. In its most recent quarter, Costco reported $1.37 billion in membership fee income, up more than 10% year-over-year (YOY), with more than 81 million paying members to date. Consumers see an opportunity to buy bulk groceries, cheap gas, and Kirkland products, all for lower prices. From a business perspective, Costco is a strong membership-based warehouse club that has an incredible moat, improving renewal rates, and a dividend to boot. Costco now pays an annualized dividend of $5.88 per share.

Plus, consider this: According to a Consumer Reports’ price comparison study, Costco’s average prices were about 21.4% below Walmart (WMT), while BJ’s Wholesale Club (BJ) averaged about 21% lower prices. Offering lower prices than Walmart should certainly attract shoppers.

In addition, Costco purposefully operates on very low gross margins. That’s because the company is more concerned about driving in more net profit from higher-margin membership fees. Over the last decade, revenue has soared from $118.72 billion in 2016 to trailing 12-month revenue of $293.5 billion today. Total cardholders have also increased from roughly 81 million in 2016 to 145.9 million. A decade ago, Costco had 715 warehouses worldwide. Now, the company has 931 stores.

Earnings Growth Has Been Strong

In the third quarter of fiscal 2026, Costco saw EPS of $4.93, which beat the consensus estimate of $4.91 per share. Revenue of $70.53 billion, up about 12% year-over-year (YOY), also beat estimates. Total sales climbed 12% YOY to $69.2 billion, while comparable sales grew almost 10% YOY. The average customer ticket was up 7.3% during the quarter, and traffic was up 2.4%.

Unfortunately, Costco did not provide guidance in the report. “We do not give guidance on what we expect future trends to look like,” said CFO Gary Millerchip on the earnings call.

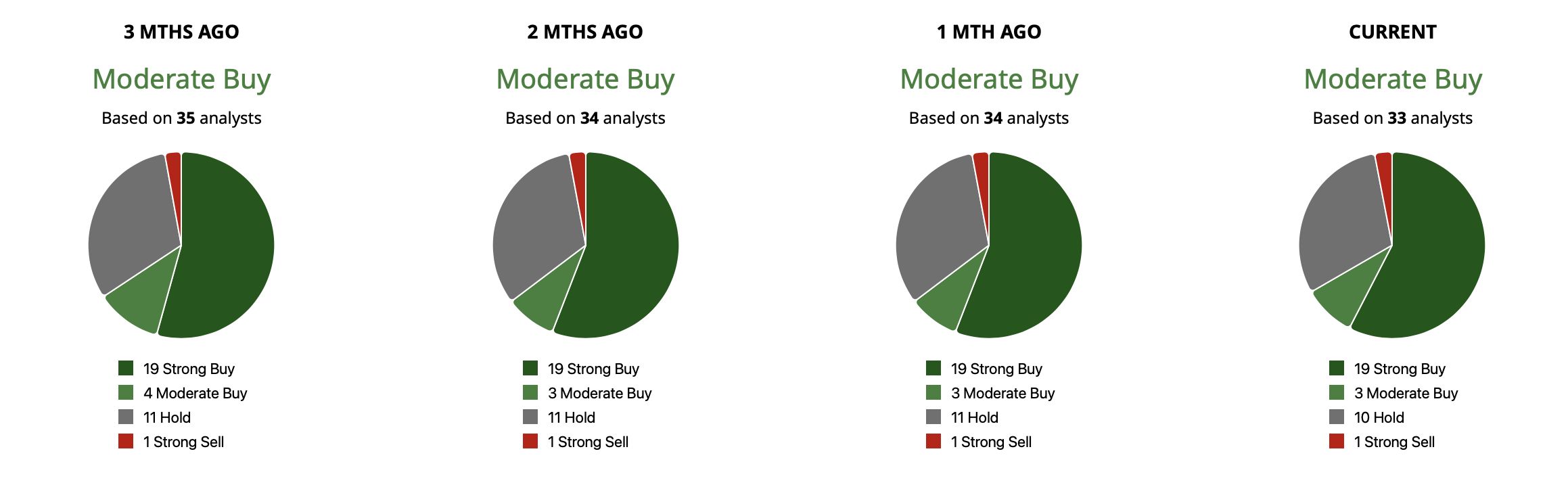

What Do Analysts Say About COST Stock?

Of the 33 analysts covering COST stock, 19 have a “Strong Buy” rating, three have a “Moderate Buy” rating, 10 have a “Hold” rating, and one analyst has a “Strong Sell” rating, making for a consensus “Moderate Buy" rating. The mean target price of $1,108.14 implies potential upside of 15% from current levels. Meanwhile, the high price target of $1,315 implies as much as 36% possible growth from here.

By cutting prices on select Kirkland Signature items, Costco is reinforcing value, strengthening customer loyalty, and potentially driving even higher traffic with memberships to boot. For investors, the bigger picture remains intact. Membership growth continues to climb, renewal rates remain exceptionally strong, and earnings momentum has stayed robust even amid a challenging retail environment.

www.barchart.com

www.barchart.com On the date of publication, Ian Cooper did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Weakness in Dividend-Paying Costco Stock Is a Strong Buying Opportunity Cutting Jobs and Chasing AI: How to Play the Rackspace Stock Transformation Story Here 6 Simple Questions to Ask Yourself So You Can Survive (and Maybe Thrive) Even in a True Bear Market QS Stock Alert: QuantumScape Strikes a Solid-State Battery Deal With Honda