Apple (AAPL) just a few days ago reported that its deal with Intel (INTC) is bigger than a simple supply-chain tweak. President Trump said Apple agreed to work with Intel to design and build chips in the U.S., and I believe that the market treated it like a real catalyst, not just noise.

Intel jumped about 7% to 10.6% on the news, while Apple was steady to slightly higher. The big idea is simple. Apple wants more domestic chip capacity. Intel wants a real blue-chip customer. And investors want to know whether this is the start of a smarter supply chain or just a headline that fades fast.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

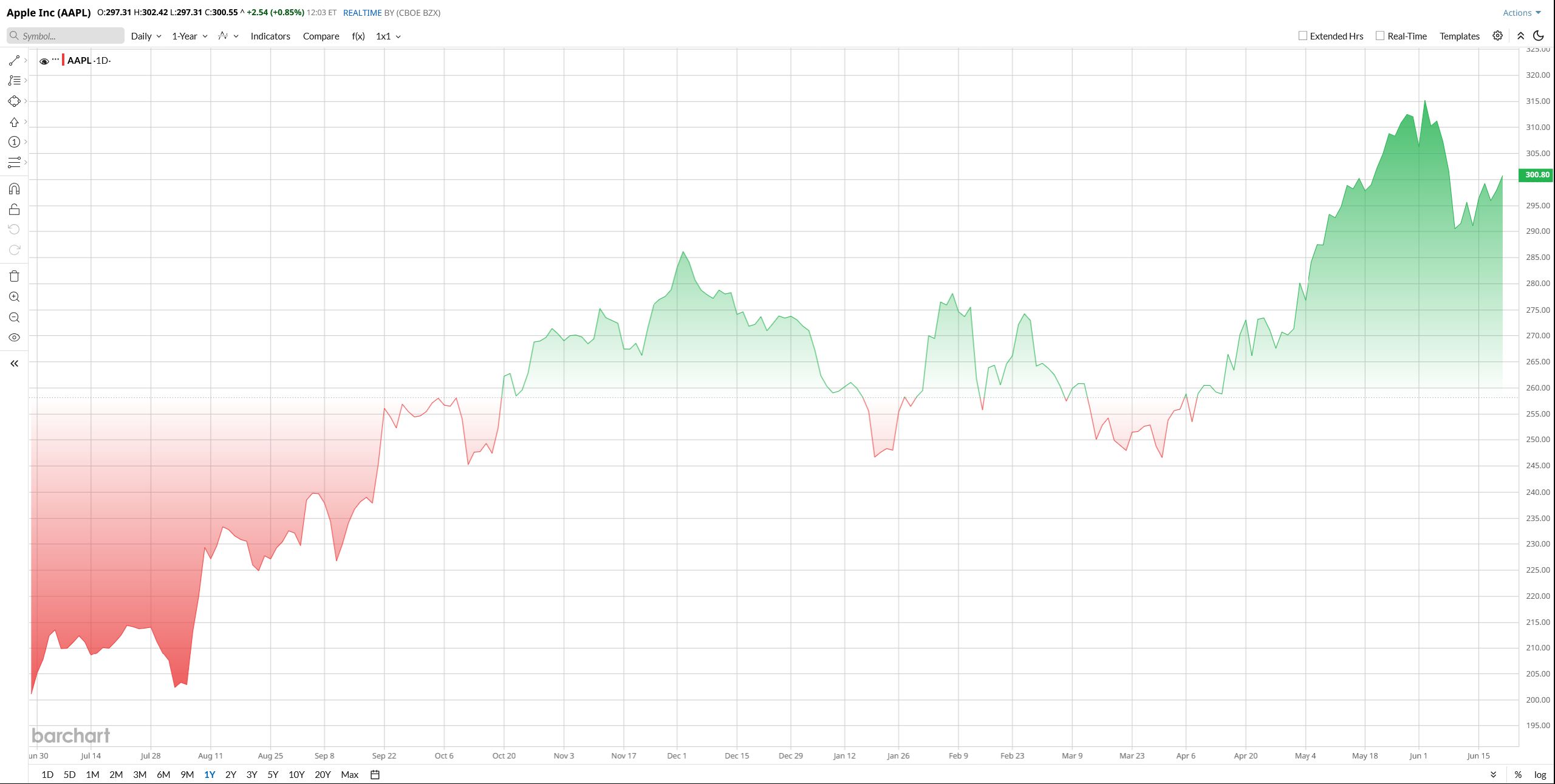

Apple Stock Has Run, Yet the Chart Still Looks Healthy

AAPL stock has had a strong year. The stock is up 49% over the past 52 weeks, and it is up about 10% year-to-date (YTD). That is a good run, even after some recent chop. The shares are still above the 50-day moving average of $288.74 and the 200-day moving average of $268.19, which tells me the trend is still intact. The recent pullback from the June 8 high near $317 looks more like digestion than damage.

This is where the story gets less exciting. Apple’s forward P/E is 32.71, and its EV/EBITDA is 26.97. That is not bargain-bin pricing. It is a premium multiple, especially when you compare it with the technology sector’s much broader valuation backdrop. On the EV/EBITDA side, Apple sits above the tech sector median of 23.9x. Clearly, Investors are paying up for quality, cash flow, and brand power. That can work. But it also leaves less room for mistakes.

www.barchart.com

www.barchart.com Why the Intel Deal Matters Now

The timing of Intel deals matters here. Apple has been dealing with higher memory costs, and Tim Cook told the Wall Street Journal that price increases are unavoidable. That tells you margin pressure is real. So a domestic Intel partnership makes sense. It gives Apple more supply-chain flexibility and reduces reliance on Asian manufacturing. It also fits the next AI-driven device cycle, where chip availability could matter as much as product design. Intel shares reacted like the market suddenly had a new reason to believe in the turnaround story. Apple shares did not need a giant move to prove the point. The strategic value is the headline.

The Latest Quarter Was Very Strong

Apple’s fiscal second quarter of 2026 was a good one. Revenue came in at $111.2 billion, up 17% year-over-year (YoY). Diluted EPS was $2.01, up 22% YoY, and net income was about $29.6 billion. Tim Cook said, “Today Apple is proud to report our best March quarter ever, with revenue of $111.2 billion and double-digit growth across every geographic segment.”

The product mix was solid, too. iPhone revenue hit $57 billion, up 22%. Mac revenue rose to $8.4 billion, iPad revenue reached $6.9 billion, wearables, home, and accessories brought in $7.9 billion, and Services hit a record $31 billion, up 16%. Apple also said operating cash flow was over $28 billion and cash on hand was about $147 billion. It raised the dividend 4% and added another $100 billion to its buyback plan. That is a very sturdy financial picture.

For the next quarter, Apple does not give formal guidance. Still, Wall Street expects June-quarter EPS of about $1.88 and revenue near $110.77 billion. For the full fiscal year, analysts model about $478.08 billion in revenue and $8.75 in EPS.

Analysts Still Lean Bullish On APPL Stock

Wedbush’s Dan Ives kept an “Outperform” rating and a $400 target, calling AI monetization and services a big source of upside. Morgan Stanley raised its target to $360 from $330 and kept an “Overweight” rating, citing a better product roadmap and clearer AI monetization.

Goldman Sachs lifted its target to $340 and kept a “Buy” rating, pointing to strong iPhone, Mac, and Services momentum.

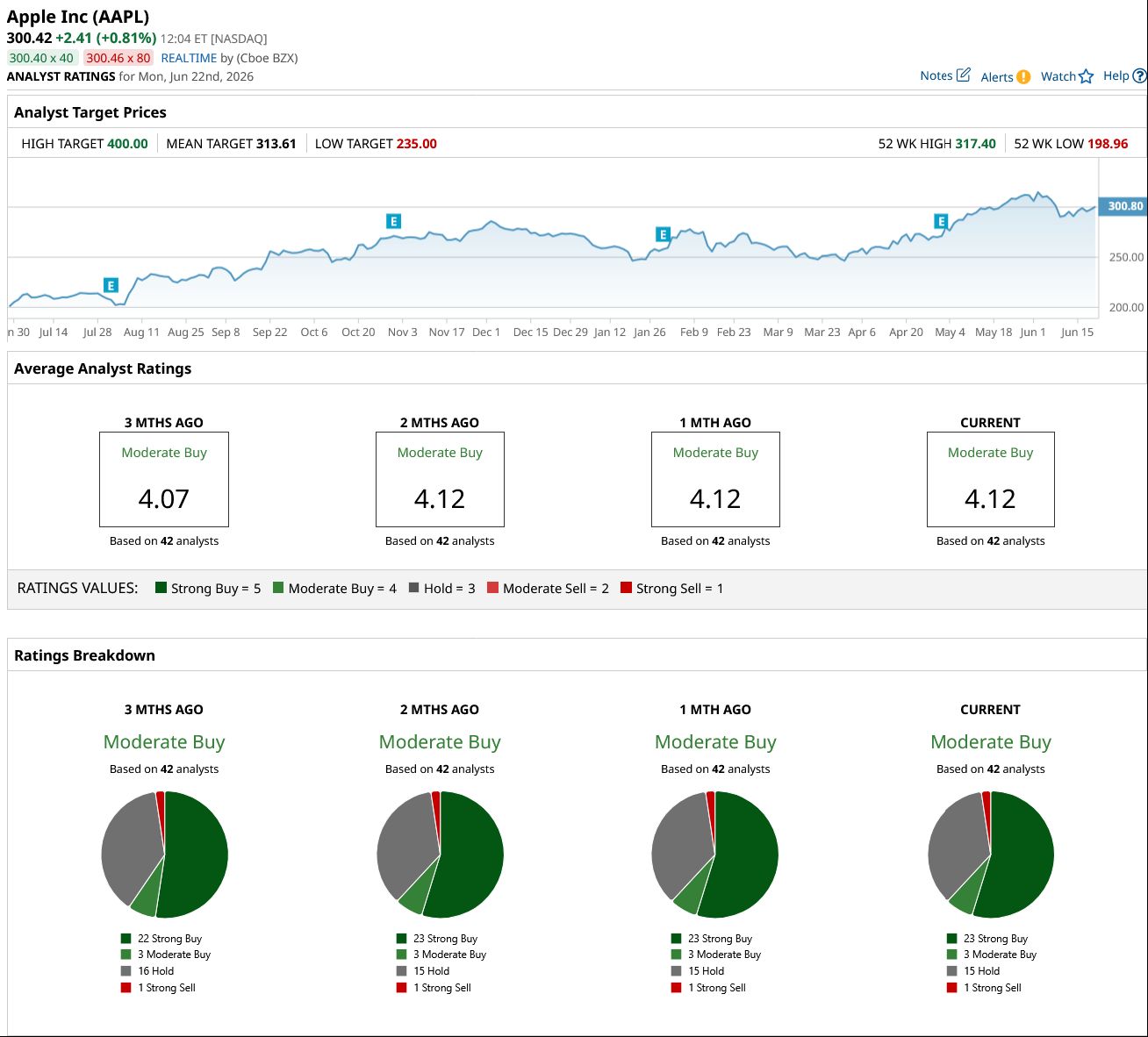

Overall, AAPL stock stands at a “Moderate Buy” consensus from 42 analysts covering the stock. The average 12-month price target of $313.61 gives a modest upside of 4% from current levels. That is not a screaming bargain. But it is still a stock Wall Street wants to own.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A New Chip Partnership Between Apple and Intel Is a Long-Term Catalyst for AAPL Stock Following Disappointing Accenture Earnings, Here's What Barchart Data Says Comes Next for ACN Stock The Smart Money Agrees That Seagate Stock Still Has Room to Surge Higher Barclays Just Upgraded Enphase Energy. Here's Why.