Since its historic public debut earlier this month, Elon Musk-led Space Exploration Technologies (SPCX), better known as SpaceX, has quickly become one of Wall Street's most closely watched stocks, capturing the attention of both institutional and retail investors. The enthusiasm has been so strong that the stock generated retail trading volume more than 3.5 times that of chip giant Nvidia Corporation (NVDA), underscoring its growing popularity among investors.

According to a recent CNBC report, the company has landed another significant deal that showcases the growing value of its data center infrastructure business. Under the agreement, artificial intelligence (AI) startup Reflection will gain access to Nvidia's cutting-edge GB300 chips housed within SpaceX's Colossus data center infrastructure to train and deploy AI models. The deal, which begins on July 1, 2026, and extends through 2029, carries a price tag of $150 million per month.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Like several of SpaceX's other infrastructure agreements, either party can terminate the deal with 90 days' notice after the initial three-month period. However, if the contract remains in place for its full duration, it could generate a staggering $6.3 billion in revenue for SpaceX. The latest win further demonstrates how SpaceX is transforming its massive AI infrastructure investments into lucrative recurring revenue streams.

Notably, the company recently signed similar, though substantially larger, computing-capacity agreements with Alphabet’s (GOOG) (GOOGL) Google and AI startup Anthropic. These data center leasing arrangements, combined with its planned acquisition of the popular AI coding platform Cursor, are creating powerful new revenue streams following the company's IPO. So, with a potential $6.3 billion opportunity now added to its growing AI infrastructure business, let’s take a closer look at SpaceX stock.

About SpaceX Stock

Founded in 2002, SpaceX has grown into the largest space company in the U.S. and the world's most active launch provider, conducting more launches annually than any other company. The company is best known for its reusable Falcon 9 rockets, which have helped reduce launch costs and increase access to space for a wide range of customers. SpaceX serves a diverse customer base that includes NASA, the U.S. Department of Defense, international space agencies, and commercial satellite operators, making it a significant participant in the global space industry.

In addition to launch services, the company operates Starlink, a satellite internet network that has become an increasingly important part of its business. Starlink is estimated to contribute between 50% and 80% of SpaceX's revenue and provides a source of funding for the company's broader technology development and exploration initiatives.

The company's scope expanded further in February with the merger of SpaceX and xAI, combining a major space and defense contractor with a rapidly growing artificial intelligence company that is investing heavily in data center infrastructure. The transaction reflects the growing overlap between AI, communications, and space-related technologies. A key area of focus for SpaceX is Starship, a fully reusable transportation system consisting of the Super Heavy booster and the Starship upper stage.

Designed to carry both crew and cargo, the system is intended to support future missions to the Moon, Mars, and other destinations. Starship remains central to Elon Musk's long-term goal of enabling human transportation to Mars and establishing a sustained presence beyond Earth. While substantial technical and operational challenges remain, the project is among the most closely watched developments in the aerospace industry.

While SpaceX's IPO was nothing short of historic, the stock's journey as a public company has been far from smooth. The company raised approximately $87 billion in its June 12 debut at $135 per share, making it the largest IPO in history. Despite the recent volatility, SpaceX still commands a massive market capitalization of roughly $2.02 trillion, placing it among the world's most valuable companies. Investor enthusiasm initially sent the stock soaring to a record high of $225.64 on June 16, representing a gain of 67% from its listing price of $135.

However, the rally proved short-lived. Shares have since retreated sharply and now trade 30.7% below that peak. The selling pressure intensified on June 22, when the stock tumbled 16.43% after reports emerged that the company plans to raise $20 billion in debt. The move sparked concerns about SpaceX's cash flow position and the significant capital required to fund its expanding AI infrastructure investments, highlighting the growing costs associated with its ambitious growth strategy.

www.barchart.com

www.barchart.com A Look Inside SpaceX’s Q1 Financials

SpaceX's first-quarter 2026 results painted a picture of a company investing aggressively for future growth, even as those investments weighed heavily on near-term profitability. According to its prospectus, consolidated revenue climbed 15% year-over-year (YOY) to $4.694 billion, up from $4.07 billion in the prior-year quarter. While the growth was solid, it represented a slower pace than the 33% revenue expansion the company delivered for full-year 2025.

The results also highlighted the increasingly diversified nature of SpaceX's business. For the three months ended March 31, 2026, the company's Space segment generated $619 million in revenue, while the Connectivity segment, anchored by Starlink, contributed $3.257 billion. Meanwhile, the AI segment added $818 million in revenue, underscoring its growing role within the company's broader business following the merger with xAI.

Despite the healthy revenue growth, profitability moved sharply in the opposite direction. SpaceX reported a consolidated net loss of $4.28 billion for the quarter, significantly wider than the $528 million loss recorded a year earlier. The primary driver behind the expanding deficit was an extraordinary surge in investment spending as the company ramps up both its space exploration and AI infrastructure ambitions.

Capital expenditures more than doubled YOY to $10.107 billion, representing a staggering 144% increase from the first quarter of 2025. The spending spree reflects Elon Musk's push to simultaneously scale next-generation space systems and build the computing infrastructure needed to compete in the rapidly evolving AI market. Perhaps most notably, AI, not rockets, accounted for the largest share of spending during the quarter.

Following SpaceX's blockbuster merger with xAI in February 2026, the company poured an eye-catching $7.72 billion into AI infrastructure in just three months, funding the expansion of massive compute clusters such as the Colossus data centers. While these investments are intended to position the company for long-term growth, they came at a significant cost in the near term. The AI segment posted an operating loss of $2.5 billion during the quarter, making it the biggest contributor to the company's overall earnings shortfall.

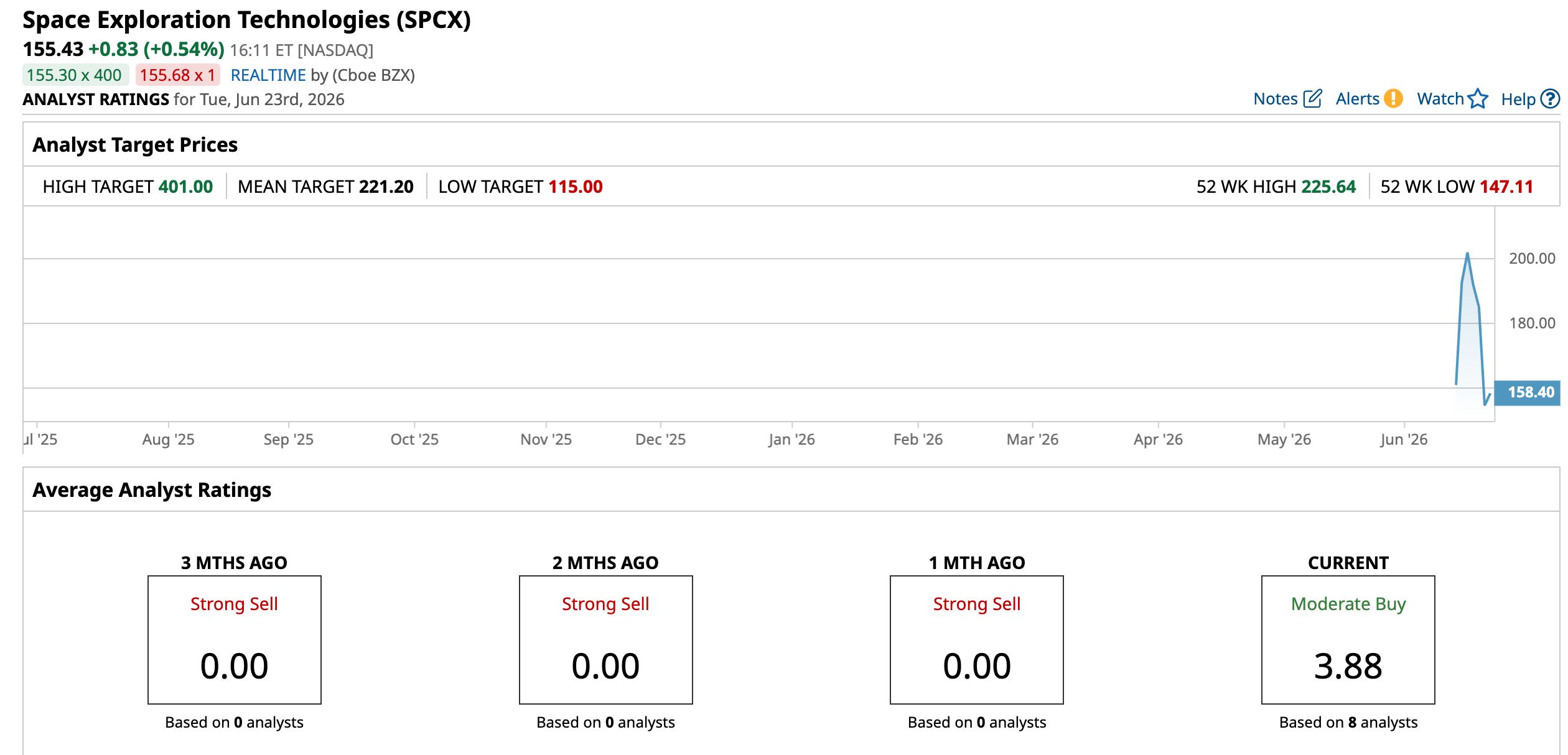

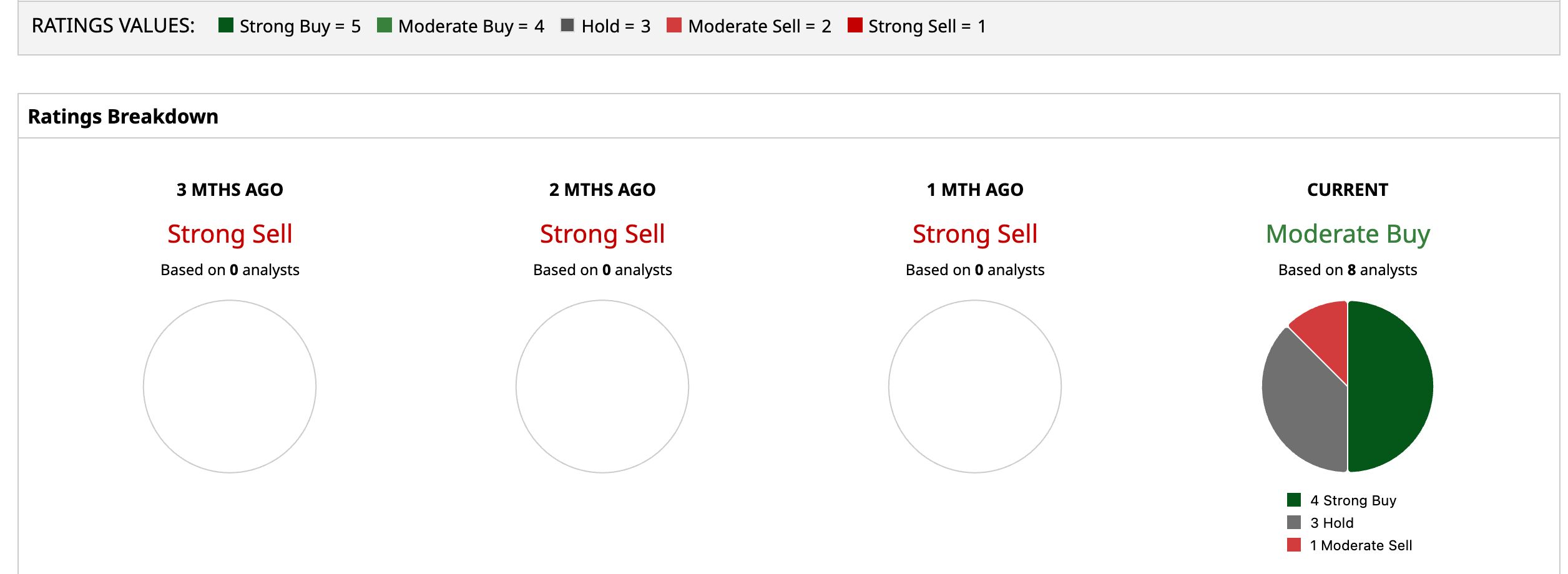

How Do Analysts View SpaceX Stock?

Arete Research became one of the most bullish voices on Wall Street after initiating coverage of SpaceX on June 18 with a "Buy" rating and a $401 price target, the highest target issued since the company's IPO. Analyst Andrew Beale based his optimistic outlook largely on the potential of SpaceX's next-generation Starlink V3 satellites, which are expected to be deployed using the company's heavy-lift Starship rocket. Beale believes the upgraded satellite network could significantly expand Starlink's reach into underserved suburban broadband markets, creating a substantial long-term growth opportunity.

Notably, his $401 target implies a valuation of more than $5 trillion, highlighting the enormous expectations some analysts have for SpaceX's future growth prospects. Despite the stock's recent pullback, Wall Street remains broadly constructive on SpaceX's long-term prospects. The stock currently carries a consensus "Moderate Buy" rating, reflecting analysts' confidence in the company's growth opportunities while acknowledging the risks associated with its aggressive investment strategy.

Among the eight analysts covering the stock, four rate it a "Strong Buy," three recommend "Hold," and only one assigns a "Moderate Sell" rating. The bullish sentiment is also evident in analysts' price targets. The average target price of $221.20 implies potential upside of 42.32% from current levels, while Arete Research’s Street-high target of $401 suggests the shares could soar as much as 158% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

JPMorgan Just Upgraded IBM Stock. Here's Why. A $6.3 Billion Reason to Buy SpaceX Stock Here Dear ASML Stock Fans, Mark Your Calendars for July 15 Why Micron May Be the Most Undervalued Winner of the AI Boom