Netflix (NFLX) stock has lost nearly 24% over the past three months, putting investors on edge ahead of the streaming giant's second-quarter 2026 earnings report, scheduled for July 16.

The recent selloff reflects a combination of competitive pressures and concerns over Netflix's growth outlook. Consolidation across the streaming industry has intensified competition, while the company's guidance following its first-quarter results failed to reassure investors.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Although Netflix delivered a strong first-quarter performance, management chose to reaffirm, rather than raise, its full-year 2026 revenue guidance. That disappointed investors who had expected a more optimistic outlook after solid subscriber engagement and strong operating performance, raising concerns that growth could slow in the quarters ahead.

Profitability is another area under scrutiny. Netflix has projected a second-quarter operating margin of 32.6%, down from 34.1% a year earlier. The expected decline primarily reflects higher content amortization expenses as the company continues investing in premium programming to support long-term growth.

Despite these near-term headwinds, Netflix's strong user engagement, expanding monetization through its advertising-supported tier, and continued investment in original content could help offset slower revenue growth and support earnings over time. Let’s take a closer look.

www.barchart.com

www.barchart.com Netflix Q2: Revenue and Earnings Growth Expected to Moderate

Netflix's second-quarter results are expected to reflect slower growth, even as the streaming leader continues to benefit from higher subscription prices, expanding membership, and a rapidly growing advertising business.

A key catalyst has been Netflix's recent price increases across all U.S. subscription tiers. While higher pricing should support revenue and profitability, the company's overall revenue growth is expected to moderate from the previous quarter.

Netflix projects Q2 revenue of approximately $12.57 billion, representing year-over-year (YoY) growth of 13.5%. Although this remains a healthy increase, it marks a slowdown from the 16.2% revenue growth reported in the first quarter. This raises concerns around subscriber additions and broader market dynamics, including competition.

One of Netflix's biggest competitive advantages remains its extensive content library. A steady pipeline of high-quality original programming and licensed content keeps viewers engaged, supports subscriber retention, and gives the company the pricing power to raise subscription fees without significantly affecting demand.

Advertising is also emerging as an increasingly important growth driver. Since introducing its ad-supported subscription tier, Netflix has expanded its addressable market by attracting more price-conscious consumers while creating a new revenue stream. The company generated approximately $1.5 billion in advertising revenue in 2025 and is targeting roughly $3 billion by 2026, highlighting the rapid expansion of this business.

On the profitability front, investors should expect more modest earnings growth. Higher content amortization expenses are likely to weigh on margins, resulting in slower EPS growth than in the previous quarter. Netflix expects second-quarter earnings per share of $0.78, representing YoY growth of 8.3%, a sharp deceleration from the stronger earnings growth delivered in Q1.

Wall Street's expectations are broadly in line with management's guidance, with analysts forecasting Q2 EPS of approximately $0.79.

Should You Buy or Avoid NFLX Stock?

Netflix's recent share price weakness reflects concerns around moderating revenue growth, margin pressure, and a more cautious full-year outlook. However, the streaming giant will continue to benefit from strong user engagement and a rapidly expanding advertising business, which will boost revenue over time. Further, the pullback in NFLX stock has eased valuation concerns.

Still, investors have reasons to remain cautious. Concerns about the company's ability to sustain its growth could limit the pace of recovery in NFLX.

With Q2 earnings approaching, staying on the sidelines may be the prudent move until there is clearer evidence that advertising momentum is accelerating and subscriber growth remains resilient.

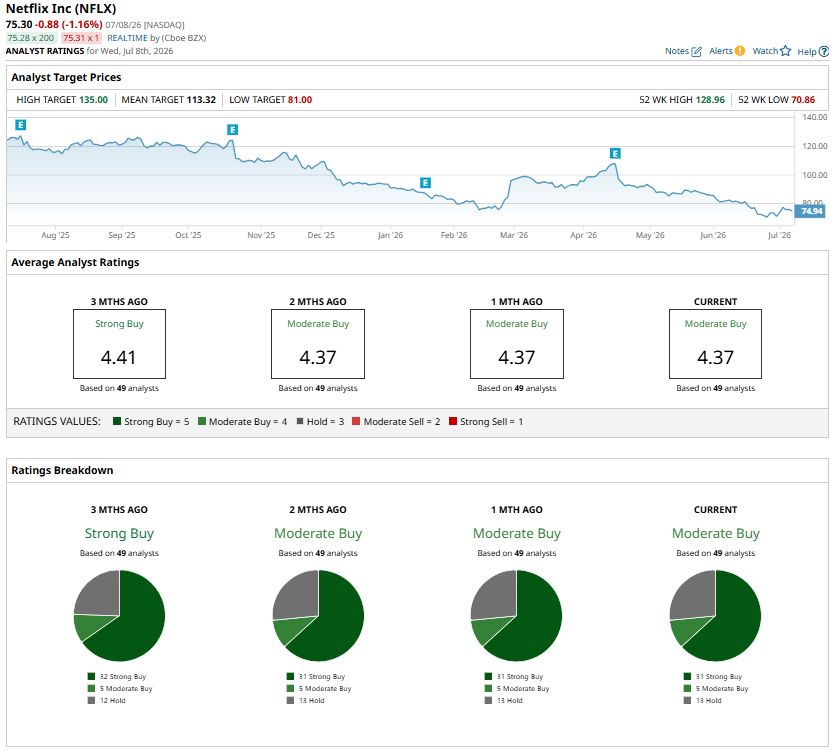

Wall Street remains cautiously optimistic, with analysts assigning NFLX stock a “Moderate Buy” consensus rating.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SpaceX Has Massive Multiyear Put Options Volume As SPCX Falls Below IPO Price Netflix Stock Slumps Ahead of Q2 Earnings. Staying on the Sidelines May Be the Smartest Move. Broadcom’s $30 Billion Jackpot: Why Apple Admitting Defeat Makes This Stock an Automatic Buy Nvidia Is Allegedly Delaying Its Kyber Rack-Scale Architecture by More Than 12 Months. What This Means for NVDA Stock.