AI technology has brought winners and losers in the software sector; however, the controversy surrounding Figma (FIG) remains quite heated. After the stock fell by about 85% from its 52-week high, fears were raised that generative AI would commoditize digital design and damage the competitive edge of the company. Nevertheless, the sentiment turned positive this week as Bank of America resumed coverage of FIG stock with a “Buy” rating and a $30 price target, saying that AI could accelerate Figma's long-run growth rather than disrupt it.

The optimistic view comes in light of the ongoing search for software companies that will be able to capitalize on AI technology instead of defending from it. While the question of valuation has become one of the most important when it comes to recently listed software names, better enterprise adoption and monetization trends have become the main metrics for the street.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Figma Stock

Figma is a maker of cloud-native collaborative design software for designers, developers, and product teams to develop digital applications and user experiences. The company is headquartered in San Francisco, California, and it operates a SaaS model based on collaborative workflows. Currently, Figma's market capitalization is approximately $9.9 billion, which makes it one of the most followed recently public software names.

FIG stock has shown extreme volatility since its public debut. The shares trade now at about $21.50, which means that they are down approximately 85% from their 52-week high of $142.92, but up more than 30% from their 52-week low of $16.60. Figma's shares rose almost 11% in the last five trading days on a positive reaction to BofA's bullish coverage initiation.

www.barchart.com

www.barchart.com Despite the massive decline in the stock, it still trades at about 8.9 times revenues and 6.4 times book value. The company is unprofitable on a trailing basis, which means that the comparison via P/E ratio becomes meaningless. Therefore, investors are valuing the business mainly based on revenue growth potential, customer growth, and the operating leverage that could become available once Figma turns profitable.

Figma Beats on Earnings

Investor sentiment was also lifted by Figma's recent earnings report. In the first quarter, the company beat consensus on both revenues and earnings and showed 28% revenue growth year-over-year (YoY). Net revenue came in at $159.9 million, driven by improved customer acquisition, higher average order values, and better repeat purchasing.

The bottom line also got significantly better. The gross margin rose slightly to 67.7%, while the operating expenses decreased as a percentage of revenues despite bigger investments in marketing. Net income was reported at $6.3 million, or $0.03 per diluted share, compared to a small loss in the same quarter of the previous year. Adjusted EBITDA rose to $13.9 million, yielding an 8.7% adjusted EBITDA margin.

Management also raised guidance for FY26 following the better-than-expected quarterly report. The company managed to pass the mark of three million active customers for the first time, which corresponds to 12.2% annual growth, while the revenue per active customer was up 5.8% to $220. The average order value was up 4.2%, reflecting both improvements in pricing and the better product mix.

Moreover, BofA expects that AI technology could become a monetization opportunity for Figma rather than a threat. According to the bank's research, 75% of enterprise customers bought extra AI credits as they ran out of their free allowances in Q1. The number of enterprise customers generating over $100,000 in annual recurring revenue was up 48% YoY, while the net dollar retention remained exceptional at 139%.

What Do Analysts Expect for FIG Stock?

Bank of America's “Buy” rating supports the growing belief that the AI strategy of Figma could be very helpful for the competitive positioning of the company. According to the bank, AI-generated content enhances the need for collaborative workflows, and here Figma has a great advantage due to its shared design platform and enterprise ecosystem.

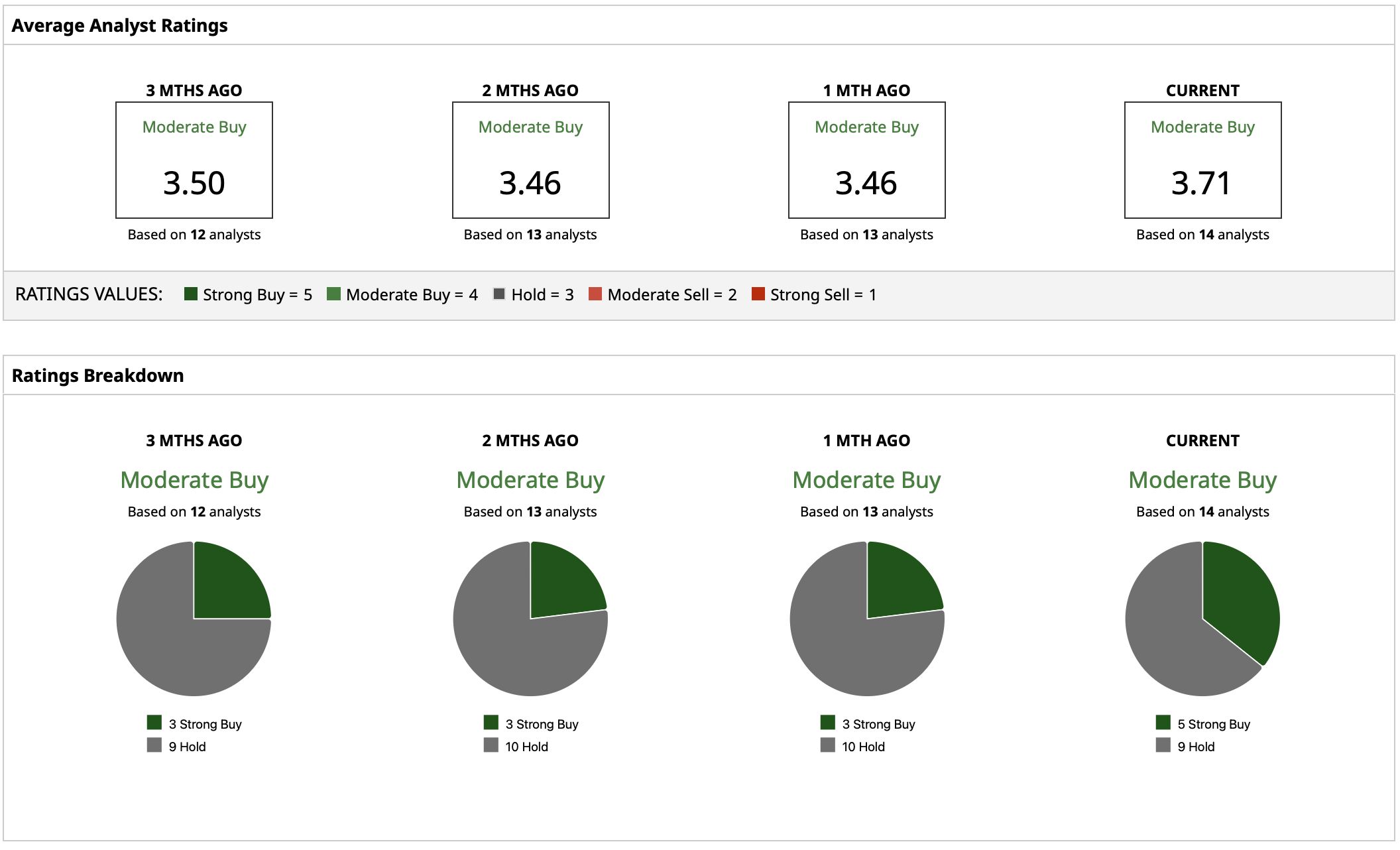

Analysts assign a “Moderate Buy” rating consensus and a mean price target of $31.10 for FIG stock. Given that the current share price stands at $21.54, the mean price target gives the potential upside of about 44%. The highest target stands at $42, while the lowest target is at $22.

www.barchart.com

www.barchart.com On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

With Iran Tensions Heating Up Again, Chevron Stock Looks Enticing Samsung Plans to Raise DRAM Prices by 20% in Q3. What That Means for Rival Micron. Palantir Stock: Accelerating Growth Improves the Risk-Reward Profile Palantir Wins Larger Contract With Major Mexican Insurer GNP Seguros. This Could Move the Needle for PLTR Stock.