A little-known $2.6 billion market capitalization company called Cohu (COHU) received a vote of confidence last week, but hardly anyone noticed. Baird initiated coverage of COHU stock with an “Outperform” rating and a $65 price target. The bullish outlook helped shares jump 10% during early trading before ending the day up by 6% on July 9. Cohu isn’t a household name, but it does play a quietly important role in the chip industry, making test and inspection equipment used to check that semiconductors work as intended before they are shipped.

Baird’s optimistic view mainly comes down to artificial intelligence (AI). Analyst Quinn Fredrickson believes Cohu is well-positioned to benefit from growing demand in high-performance computing, memory inspection, and power chip testing. Fredrickson expects the firm’s high-performance computing revenue to more than double this year, going from $40 million in 2025 to as much as $100 million. The analyst also sees a large pipeline of potential deals that customers are still testing before fully committing, which could open up a new growth avenue for Cohu heading into 2027.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The AI story isn’t the only driver. Fredrickson cited recovery across core automotive, industrial, and mobile markets as another reason for the positive outlook, with earnings and margins expected to surge from low levels. This isn’t the only recent bullish call for Cohu stock, either, as a number of analysts have lifted their price targets after the latest strong quarter. On July 10, Stifel increased its COHU stock price target from $50 to $70 while maintaining a “Buy” rating, signaling strong confidence in near-term growth.

About Cohu Stock

Cohu is a semiconductor company that supplies test and inspection equipment used by chip manufacturers to improve product quality and production efficiency. Its product portfolio includes automated test equipment, test handlers, inspection and metrology, and data analytics software. Founded in 1947, the company is headquartered in San Diego, California, and led by CEO Luis Müller.

Over the last 12 months, COHU stock has surged 168%, outperforming the iShares Semiconductor ETF’s (SOXX) 119% gain over the same period. The growth has been driven primarily by rising demand for testing AI and high-performance computing chips.

www.barchart.com

www.barchart.com Cohu’s valuation reflects a company that the market expects to bounce back strongly. Since the company is currently loss-making, the forward price-to-earnings (P/E) ratio isn’t meaningful yet. However, the forward price-to-sales (P/S) ratio of 5.8 times sits well above its own five-year average of 2.4 times. This means that COHU stock is trading at more than double its historical norm.

What considerably justifies the steep premium is the earnings outlook. The EPS growth trajectory points to 128% growth in fiscal 2026, followed by more than 580% growth in fiscal 2027. That sharp rebound reflects a recovery in the chip cycle and Cohu’s growing exposure to AI demand. This is part of why Baird initiated bullish coverage for the firm. Cohu's balance sheet is also solid; the company holds $489 million in cash against $330 million in debt. Being net cash positive by around $159 million provides a healthy financial cushion for a firm still working its way back to profitability.

Overall, COHU stock is already priced for a strong recovery. As long as that happens, the valuation holds up.

Cohu Sees a Path Back to Profit in 2026

Cohu announced its first-quarter fiscal 2026 earnings on April 30. During the quarter, the company generated $125.1 million in revenue, which comfortably beat the Wall Street consensus of $122.1 million. Despite revenue being up more than 2% from the forecast, non-GAAP EPS came in at $0.01, missing the analyst estimate of $0.03 Operating expenses of $55 million also came in higher than guidance. This mixed performance suggests that, while the company faces challenges in cost management, its revenue-generating capabilities remain strong.

Moving forward, Cohu projects Q2 revenue of $144 million, representing 15% sequential growth. For full-year 2026, the company also expects revenue growth of 20% to 25%, driven by high-performance computing opportunities and a recovery in the automotive and industrial segments. EPS is expected to be $0.54 for fiscal 2026, representing a significant turnaround from Cohu's loss per share over the last 12 months. Management sees a computing segment opportunity pipeline of approximately $750 million, including around $650 million related to test handlers and another $100 million from high-bandwidth memory (HBM) inspection, according to CEO Luis Müller. Cohu is set to announce Q2 results on July 30.

What Are Analysts Saying About Cohu Stock?

On July 9, Baird initiated coverage of Cohu with an “Outperform” rating and a $65 price target. The firm believes the semiconductor company is well-positioned to benefit from the AI tailwind. Moreover, analyst Quinn Fredrickson views shares as attractively valued and expects earnings and profit margins to improve significantly from current levels. Any broader weakness in the semiconductor sector would be viewed as a buying opportunity for COHU stock, according to the analyst.

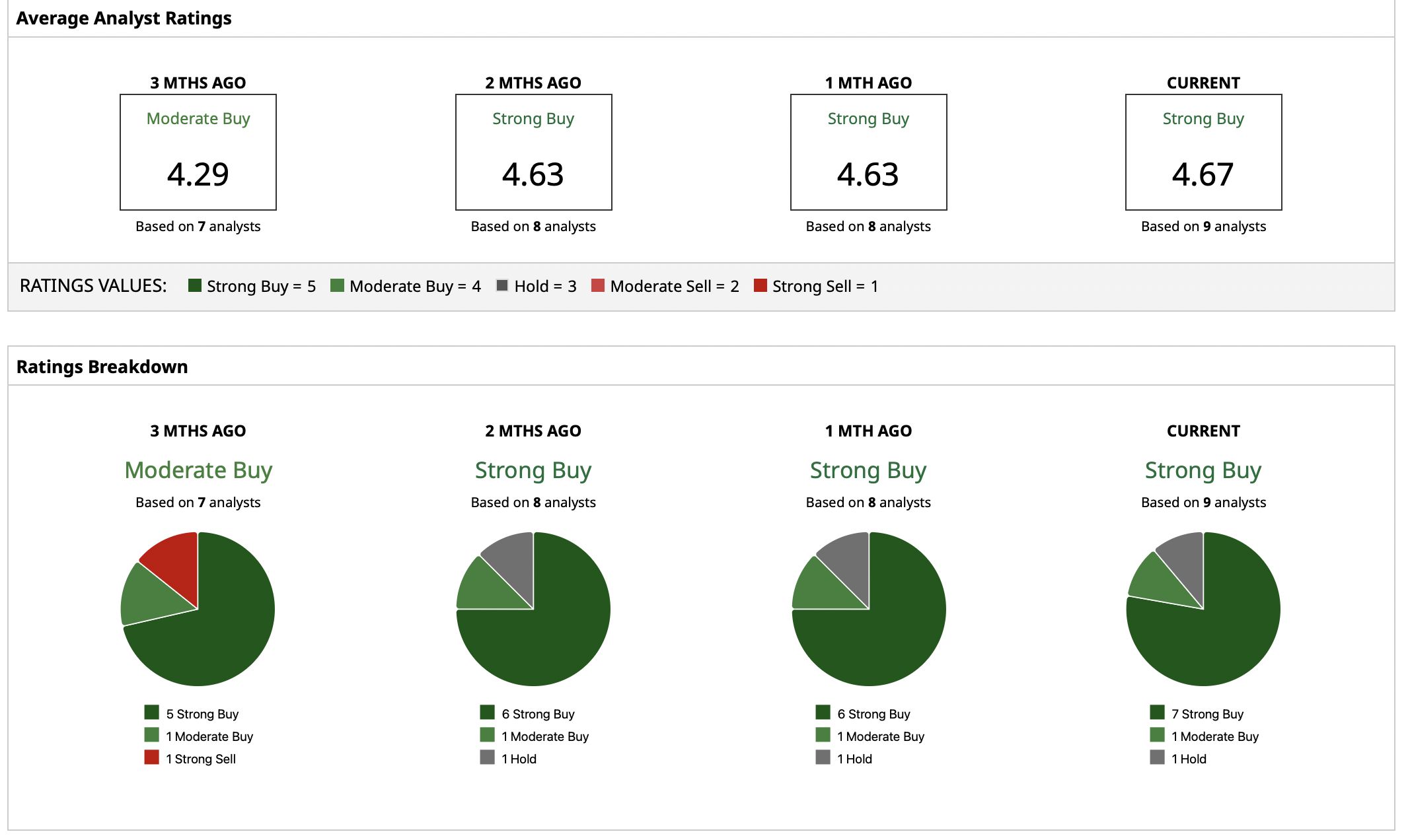

Based on nine Wall Street analysts with coverage, Cohu carries a consensus “Strong Buy” rating. COHU stock currently sits below the mean price target of $65, reflecting 26% potential upside from here. The high target of $80 implies potential upside of 55%, while even the lowest analyst price target of $53 suggests limited upside from current levels.

www.barchart.com

www.barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

AAP’s Unusually Active $62.50 Call Isn’t a Covered Call. It’s a Bullish Bet on a Beaten-Down Stock. How to Play Cognizant Stock After a Major IBM-Driven Sell-Off Eli Lilly Is Buying AtaiBeckley in $2.8 Billion Deal. What It Means for LLY Stock Wall Street Is Suddenly Bullish on This Under-the-Radar Chip Stock