Charles River Associates CRAI benefits from strong demand for its economic, financial and management consulting services . The growing demand for specialized advisory services drives the company’s long-term growth. The company’s high-quality analytical and strategic consulting services across diverse industries give it a competitive edge over its rivals. Growth across segments and regions has remained strong in recent times. However, the rapid evolution of AI technologies, growing talent costs and intense rivalry within the industry remain key concerns.

The company’s second-quarter 2026 earnings are expected to increase 12.8% year over year. Earnings for 2026 and 2027 are projected to rise 3.5% and 11.2%, respectively, year over year. Revenues are expected to increase 6.5% in 2026 and 4.1% in 2027.

Factors That Bode Well for CRAI

CRAI’s revenue growth is primarily driven by its consulting and research services. Rising demand for specialized advisory services fuels demand for its offerings. The company has maintained strong revenue growth in its Management Consulting services, especially in Energy, Finance, Forensic Services and Life Sciences practices.

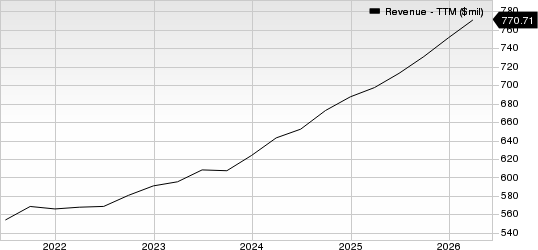

Charles River Associates Revenue (TTM)

Charles River Associates revenue-ttm | Charles River Associates Quote

The company’s Energy practice advises utility companies, system operators, regulators, private equity firms, and energy equipment manufacturers, and conducts commercial and regulatory due diligence for a large community solar portfolio acquisition. CRAI’s Life Sciences practice leverages its expertise in strategy, pricing and healthcare policy. The growing demand for these management consulting services has enabled both practices to achieve significant revenue growth.

Complex litigation, investigations, bankruptcy matters, securities disputes, and corporate governance engagements are driving growth of its Finance practice, while the Forensic Services practice has been witnessing strong demand across cybersecurity, fraud investigations, trade-secret disputes and privacy-related litigation.

CRAI’s Legal, Regulatory and Antitrust practices benefit from active markets, driven by favorable industry conditions and a resurgence in global mergers and acquisitions activity. The company reported 11.5% year-over-year growth in its Legal and Regulatory Services segment in the first quarter of 2026.

The company is witnessing growth across all major regions. Revenues from North American operations increased 8.5% year over year in the last reported quarter, while revenues from international operations expanded an impressive 20.3% year over year from the prior-year quarter.

CRAI consistently returns value to shareholders through dividends and share repurchases. The company paid dividends of $10.8 million, $12.3 million and $13.8 million, while repurchasing shares of $31.4 million, $33.3 million and $47.1 million in 2023, 2024 and 2025, respectively. This consistency instills investors’ confidence in the company.

Key Risks to Watch

CRAI faces stiff competition from large diversified global firms, such as McKinsey & Company and Boston Consulting Group. These firms have more extensive resources, which allows them to undercut competitors on price or invest in emerging technologies at a faster pace. This dampens CRAI’s profitability as it competes on price or service differentiation.

The company is also witnessing higher talent costs due to intense competition in the global labor market. These rising expenses increase operating costs and erode profitability.

Moreover, while advancements in automation and AI offer significant opportunities for the industry, these technologies enable clients to integrate new methods and techniques, potentially reducing their dependence on firms like CRAI.

CRAI currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Stocks to Consider

A couple of better-ranked stocks in the Business Services sector are Trane Technologies plc TT and TransUnion TRU.

Trane Technologies carries a Zacks Rank #2 (Buy) at present. It has a long-term earnings growth expectation of 14.6%.

TT delivered a trailing four-quarter earnings surprise of 2.7%, on average.

TransUnion also holds a Zacks Rank of 2 at present. It has a long-term earnings growth expectation of 13.5%.

TRU beat earnings estimates in each of the last four quarters, with an average earnings surprise of 6.3%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Charles River Associates (CRAI): Free Stock Analysis Report

Trane Technologies plc (TT): Free Stock Analysis Report

TransUnion (TRU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).