Hasbro, Inc.’s HAS Wizards of the Coast segment is increasingly emerging as its primary growth driver, and first-quarter 2026 results provided further evidence of the importance. While Hasbro's broader Consumer Products business remained relatively stable, Wizards delivered exceptional growth fueled by the continued success of Magic: The Gathering and expanding digital initiatives.

The segment generated revenues of $582 million in the first quarter, up 26% year over year, while operating profit climbed 29% to $298 million. Its operating margin exceeded 51%, highlighting the strong profitability of the business. Magic: The Gathering remained the key catalyst, with the Lorwyn Eclipsed release becoming the best-selling premier set in the franchise's history. Momentum continued into the second quarter as Secrets of Strixhaven surpassed Lorwyn Eclipsed's launch performance.

Hasbro's strategy of blending original content with popular external franchises is also paying off. Collaborations with Teenage Mutant Ninja Turtles, Marvel, Final Fantasy and Avatar: The Last Airbender helped attract new players and drive record backlist sales. Management noted that Universes Beyond has become one of the most successful player-acquisition tools in Magic's history.

Beyond tabletop gaming, Wizards is broadening its reach through digital platforms. The expansion of Magic Arena, upcoming AAA game launches such as Exodus and Warlock, and growing Dungeons & Dragons engagement are creating additional revenue opportunities. Hasbro also reiterated that Wizards, digital gaming and licensing remain its top investment priorities.

Although Consumer Products faces tariff, input-cost and cybersecurity-related challenges, Wizards continues to deliver strong growth, high margins and expanding fan engagement. Based on current trends, the segment appears well positioned to remain Hasbro's most powerful earnings and growth engine in the years ahead.

How Do Hasbro's Rivals Compare in Collectibles and Gaming?

While Hasbro is benefiting from the rapid growth of Wizards of the Coast, competitors are also investing heavily in toys, collectibles and entertainment-driven products.

Mattel MAT has been expanding beyond traditional toys through digital gaming, entertainment content and franchise development. The company continues to leverage iconic brands such as Barbie, Hot Wheels and UNO to create cross-platform experiences. However, unlike Hasbro's Wizards segment, Mattel lacks a trading-card franchise with the same level of recurring engagement, collectible demand and high-margin revenue streams. As a result, its growth remains more dependent on toy sales and entertainment partnerships.

JAKKS Pacific JAKK competes in several toy categories, including action figures, role-play toys and licensed merchandise tied to major entertainment properties. The company benefits from relationships with leading franchises such as Disney and Nintendo, which help drive product demand during major movie and gaming releases. However, JAKKS' business is largely tied to seasonal toy sales and licensing cycles, whereas Hasbro's Wizards segment generates recurring revenues through trading card releases, organized play events, digital offerings and a highly engaged global player community.

The key differentiator for Hasbro is Wizards of the Coast's ability to combine collectibles, gaming, digital expansion and licensing into a powerful ecosystem, creating a more durable and profitable growth engine than traditional toy-focused rivals.

HAS’ Stock Price Performance & Valuation Trend

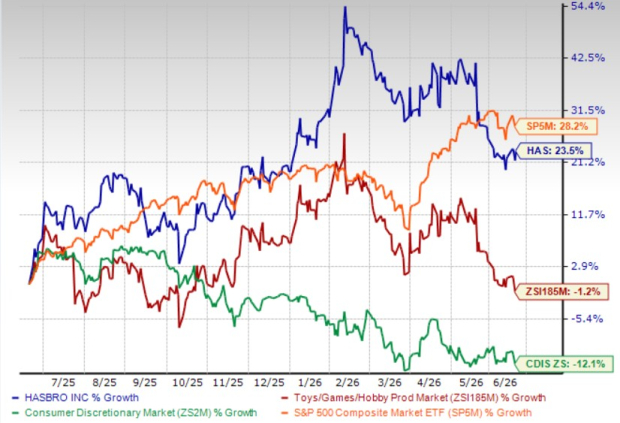

Shares of this games and toys manufacturer have gained 23.5% in the past year, outperforming the Zacks Toys - Games - Hobbies industry and the broader Consumer Discretionary sector, but underperforming the S&P 500 Index.

Price Performance

Image Source: Zacks Investment Research

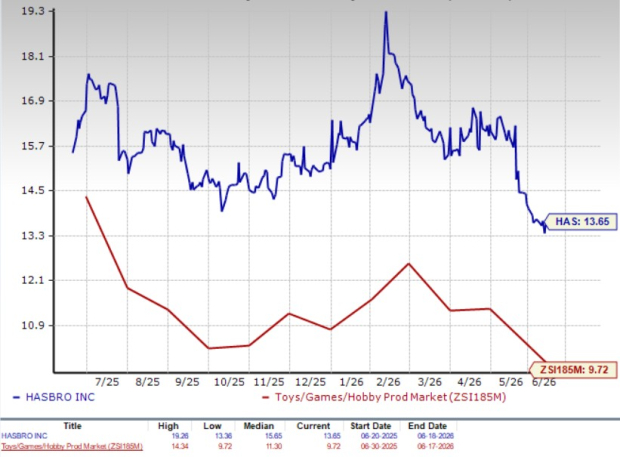

HAS stock is currently trading at a premium to its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 13.65, as shown in the chart below.

P/E (F12M)

Image Source: Zacks Investment Research

Earnings Estimate Revision of HAS

HAS’ earnings estimates for 2026 and 2027 have trended upward in the past 60 days to $6.01 and $6.44 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 8.5% and 7.2%, respectively.

Image Source: Zacks Investment Research

HAS stock currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hasbro, Inc. (HAS): Free Stock Analysis Report

Mattel, Inc. (MAT): Free Stock Analysis Report

JAKKS Pacific, Inc. (JAKK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).