Rithm Capital Corp. RITM is moving beyond a balance-sheet-heavy mortgage and real estate model. Its growth story now includes asset management, operating scale and technology-led efficiency at Newrez.

That shift matters because earnings still carry exposure to rates, mortgage servicing rights and fair-value swings. Investors may need to watch not only how much RITM earns, but how repeatable those earnings become.

How Rithm Capital Is Building Fee Income

Rithm Capital has been expanding its asset management platform across private credit, real estate, fund liquidity and other alternative strategies. The company had roughly $59 billion of assets under management as of March 31, 2026, up from $35 billion a year earlier.

Sculptor and Crestline are central to this push. Management has positioned the two as complementary platforms, with combined assets of roughly $60 billion managed and additional fundraising underway.

The strategy also fits Rithm Capital’s operating model. Newrez and Genesis can source asset-based finance opportunities that may feed investment products, giving the asset management arm a potential pipeline tied to businesses Rithm already controls.

Why RITM Wants More Scalable Earnings

Fee-centric operations can improve the quality of Rithm Capital’s earnings mix because they are less dependent on deploying balance-sheet capital. A larger asset management business could add recurring management fees and make growth more scalable.

That would be a meaningful contrast to income tied to mortgage assets, spreads and fair-value changes. Rithm Capital’s broader platform already spans mortgage origination and servicing, residential transitional lending, asset management, investment portfolio assets and commercial real estate.

Annaly Capital Management Inc. NLY offers a useful industry comparison because it also operates in mortgage-related assets and mortgage servicing rights. PennyMac Mortgage Investment Trust PMT, another mortgage-focused real estate investment trust, gives investors a second peer for judging how RITM’s platform breadth differs from more focused mortgage investment models. Viewed against NLY and PMT, RITM’s push toward asset management shows why scalability has become a more important part of its long-term earnings mix.

How Newrez Tech Could Change RITM Margins

Newrez remains Rithm Capital’s largest business and a core earnings engine. In the first quarter of 2026, it generated $273.7 million of pre-tax operating income, with $15.5 billion of funded production and $850 billion of servicing unpaid principal balance.

The next leg of the Newrez story is less about size alone and more about cost efficiency. Servicing costs per loan fell to $51 in the first quarter of 2026 from $54 in the prior quarter.

Technology is central to that margin effort. HomeVision automated underwriting tools, the ValonOS servicing transition and process automation are expected to reduce costs per loan over time. Management targets an additional 15% reduction from the current run rate in 2026.

Where Rithm Capital's Macro Exposure Still Dominates

The transition is still in progress, and macro exposure remains hard to ignore. As of March 31, 2026, nearly 20% of Rithm Capital’s total assets were directly tied to mortgage servicing rights and related financing receivables.

That exposure can work both ways. Higher rates generally support mortgage servicing rights valuations by reducing refinancing activity, but mortgage spreads, prepayment speeds and market volatility still affect results.

The first quarter showed how these forces can overshadow strategic progress. Rithm Capital reported a $204.2-million negative change in the fair value of mortgage servicing rights and related financing receivables, net of economic hedges.

How RITM's Ratings Reflect a Trend in Progress

The bottom line is that Rithm Capital is building a more diversified, fee-oriented platform, but the stock does not yet carry the profile of a clear momentum story. The business mix is improving, while rate sensitivity and valuation swings remain major variables.

RITM currently carries a Zacks Rank #3 (Hold). That rank suggests a more balanced earnings estimate backdrop over the next one to three months rather than a clearly positive revision trend. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for 2026 and 2027 earnings has remained unchanged over the past month, pointing to a neutral setup.

Estimate Revision Trend

Image Source: Zacks Investment Research

The Style Scores reinforce that measured view. RITM has a Value Score of C, Growth Score of F, Momentum Score of D and VGM Score of F. Since Zacks Style Scores complement the Zacks Rank, weak Growth, Momentum and VGM readings indicate limited style-based support.

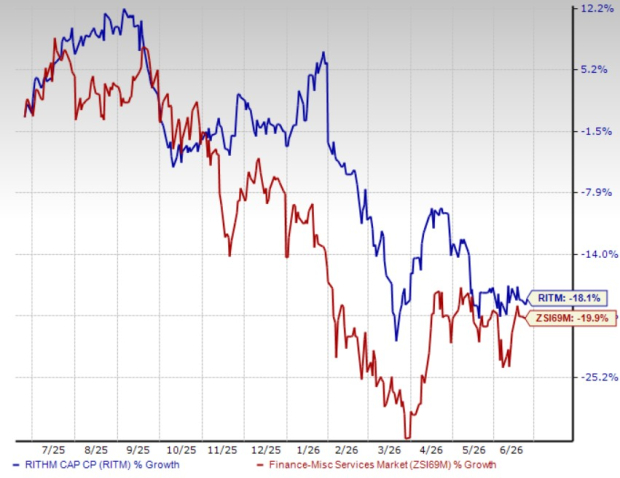

Over the past year, RITM shares have declined 18.1%, compared with the industry’s 19.1% decline.

Price Performance

Image Source: Zacks Investment Research

For now, RITM’s strategic direction is worth monitoring. The fee-income and technology-efficiency trends are encouraging, but the ratings and macro sensitivity argue for patience until estimate momentum or stock performance becomes more supportive.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PennyMac Mortgage Investment Trust (PMT): Free Stock Analysis Report

Annaly Capital Management Inc (NLY): Free Stock Analysis Report

Rithm Capital Corp. (RITM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).