The AI-driven semiconductor upcycle has created significant opportunities for emerging chip suppliers positioned in high-growth infrastructure markets, and both AXT AXTI and Diodes DIOD are benefiting from this trend.

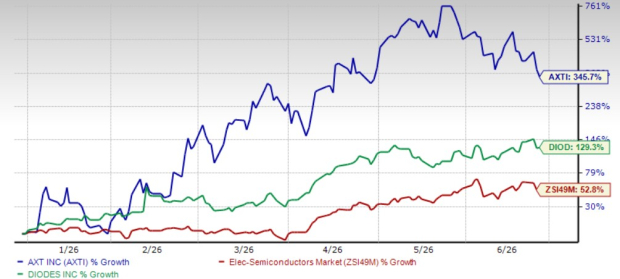

AXT has rapidly become a critical supplier of Indium Phosphide substrates used in optical transceivers supporting hyperscale AI data centers, while Diodes is capitalizing on demand growth across automotive semiconductors, industrial applications, and AI server-related power management solutions. Although both stocks have delivered exceptional gains in 2026, with AXTI surging 345.7% and DIOD climbing 129.3%, AXT’s direct leverage of the AI infrastructure boom makes its long-term story increasingly compelling.

Looking ahead, both companies appear positioned for continued growth through the second half of 2026. However, the nature of their growth trajectories differs considerably. AXT is entering an aggressive multiyear capacity expansion cycle supported by record customer backlog and hyperscaler-driven optical demand.

Diodes continues to execute a diversified semiconductor strategy centered on automotive electrification, industrial automation, and data center infrastructure. While both are benefiting from AI-related tailwinds, AXT appears more directly exposed to one of the fastest-growing segments of the semiconductor industry.

YTD Price Chart AXTI vs DIOD

Image Source: Zacks Investment Research

Case for AXTI

AXT is increasingly emerging as one of the most direct beneficiaries of hyperscale AI infrastructure spending. The company’s first-quarter revenues grew 39% year over year to $26.9 million. Indium Phosphide revenues totaled $13.6 million, representing more than half of total revenues.

Management emphasized that demand is being driven primarily by optical transceivers and high-speed photodetectors used in AI data center infrastructure, with the company now supplying multiple U.S. hyperscalers indirectly through Tier 1 optical customers.

The company’s biggest strength lies in its extraordinary growth visibility. Management disclosed record backlog exceeding $100 million, with the second quarter expected to become the largest Indium Phosphide quarter in the company’s history.

AXT is aggressively scaling its production capacity, targeting a doubling of its Indium Phosphide capacity by the end of 2026, followed by another doubling in 2027, with additional expansion plans extending into 2028. The company is also positioning for future demand from co-packaged optics (CPO), silicon photonics, and China’s accelerating AI supply-chain expansion. The primary risk relates to export permit uncertainty and geopolitical exposure, though demand momentum currently remains extremely favorable.

AXT currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

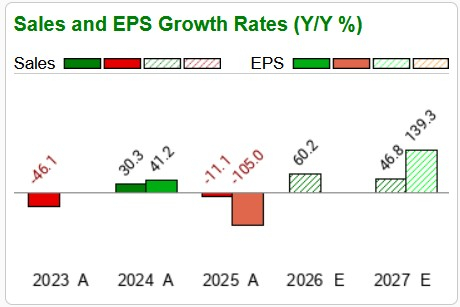

AXTI’s Sales & EPS Estimate

Image Source: Zacks Investment Research

Case for DIOD

Diodes has demonstrated strong operational execution, though its growth profile remains more diversified and less focused on AI infrastructure than some of its peers. First-quarter revenues rose 22% year over year to $405.5 million, marking its sixth consecutive quarter of double-digit growth.

Management highlighted strong momentum across automotive, industrial, and AI server-related applications, with automotive and industrial now accounting for 44% of total product revenues. Growth is being driven by semiconductor demand linked to EV content expansion, factory automation, and data center power management systems.

The company continues to expand its AI-related opportunities across server power supply units, networking infrastructure, PCIe connectivity solutions, battery backup units, and silicon carbide MOSFET products targeting high-voltage data center power systems. Unlike AXT’s concentrated exposure, Diodes operates a far more diversified business model spanning industrial automation, automotive electronics, consumer devices, communications infrastructure, and computing.

This diversification provides stability, but growth is likely to be moderate compared to AXT’s explosive trajectory. Challenges include lengthy customer qualification cycles, gradual fab utilization improvement timelines extending into 2027-2028, and slower direct AI monetization compared to pure-play infrastructure suppliers.

Diodes currently carries a Zacks Rank #3 (Hold).

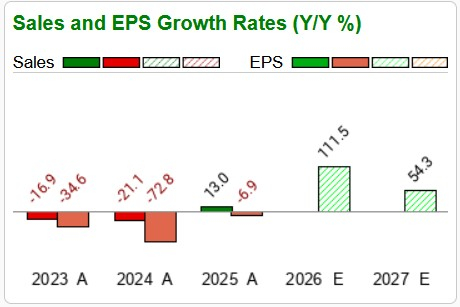

DIOD’s Sales & EPS Estimate

Image Source: Zacks Investment Research

Valuation Comparison

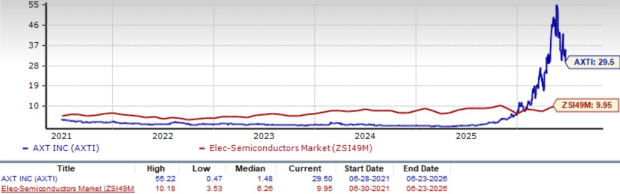

AXTI now trades at a forward 12-month price-to-sales (P/S F12M) ratio of 29.5X, significantly above the semiconductor industry average of 9.95X and dramatically above its own five-year median valuation multiple of 1.48X. The premium clearly reflects investor expectations for sustained AI-driven growth. While valuation appears stretched, the market is pricing in AXT’s unique position within the rapidly expanding optical infrastructure supply chain.

AXTI’s P/S F12M Chart

Image Source: Zacks Investment Research

DIOD trades at P/S F12M multiple of 3.17X, well below the semiconductor industry average of 9.95X, though still above its five-year median multiple of 1.93X. The lower valuation suggests investors remain more cautious about its long-term growth outlook. Although it trades at a lower valuation than AXTI, the market appears to be assigning it a lower premium because of its diversified business model and less direct exposure to AI-driven growth.

DIOD’s P/S F12M Chart

Image Source: Zacks Investment Research

Conclusion

Both AXT and Diodes are positioned to benefit from favorable semiconductor industry tailwinds in 2026, but the magnitude and nature of their growth opportunities differ meaningfully. Diodes offers investors diversified semiconductor exposure supported by strong execution across automotive, industrial, and AI server markets.

However, AXT currently presents the more attractive upside opportunity. Its direct exposure to hyperscale AI infrastructure buildouts, rapidly expanding Indium Phosphide demand, record backlog, aggressive capacity expansion roadmap, and differentiated supply-chain advantages create a significantly stronger long-term growth narrative. Despite premium valuation levels, AXTI’s superior AI-driven positioning makes it the more attractive emerging semiconductor stock currently.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Diodes Incorporated (DIOD): Free Stock Analysis Report

AXT Inc (AXTI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).