Winnebago Industries WGO reported third-quarter fiscal 2026 results with continued demand softness, missing both top and bottom line estimates as consumers and dealers remained cautious. Revenues fell to $698.7 million, lagging the Zacks Consensus Estimate of $776.9 million by 10.1%. Adjusted EPS came in at $0.66, missing the consensus estimate of $0.82 by 19.5%.

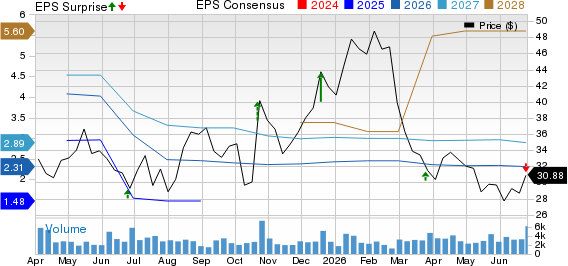

Winnebago Industries, Inc. Price, Consensus and EPS Surprise

Winnebago Industries, Inc. price-consensus-eps-surprise-chart | Winnebago Industries, Inc. Quote

Management emphasized disciplined production, cost control and portfolio repositioning as retail trends weakened through the quarter. While Motorhome improved, Towables and Marine remained pressured, prompting updated guidance and continued focus on inventory turns and affordability initiatives.

WGO Sees Softer Demand and Dealer Caution Rise

CEO Michael Happe said that the quarter reflected sustained demand pressure driven by affordability constraints, elevated interest rates and macro uncertainty. He noted that consumer engagement in outdoor recreation remained intact, but purchase timing continued to shift later amid caution.

Happe emphasized that demand deteriorated as the quarter progressed, particularly from late March onward, with dealers remaining conservative on inventory intake. Management described the environment as one of limited near-term visibility.

The company also pointed to disciplined production alignment with retail demand as a central operating priority. Leadership stressed that protecting balance sheet strength and managing working capital remained key priorities.

Motorhome Shows Early Stabilization Signals

Motorhome RV emerged as the most constructive segment, with revenues rising year over year to $320.7 million. Operating income improved sharply to $9.6 million from a loss in the prior year period.

Management credited gains to Grand Design Motorized and Newmar execution, along with improving mix from product introductions. Happe highlighted retail share gains across multiple time horizons as evidence of improving competitive positioning.

CFO Bryan Hughes said Motorhome margin progress reflected both higher volumes and selective pricing actions. He expects continued efficiency gains and product refreshes to support improvement.

Towables Remain Under Pressure From Promotions

Towable RV remained the most challenged segment, with revenues falling to $274.7 million and operating margin compressing to 5.8%. Management attributed weakness to softer retail conditions and heightened promotional activity.

Happe noted that pricing adjustments tied to model year transitions occurred late in the quarter, while competitive intensity remained elevated. He also pointed to targeted pressure in higher-priced categories, particularly fifth wheels.

The Winnebago Towables portfolio showed early traction from newer products such as Thrive and Access. However, management acknowledged that dealer caution on inventory replenishment remained a meaningful headwind.

Marine Strength Anchored by Barletta Share Gains

Marine performance declined year over year, with revenues falling to $92.4 million, though Barletta continued to gain share in the aluminum pontoon market. Trailing 12-month share reached 9.3% through April.

Happe said Barletta’s momentum reflected strong dealer relationships and continued product expansion, including the Sanza introduction. He added that demand remained more stable than RV but still below historical norms.

Chris-Craft performance remained steady, supported by resilient high-income consumers. Management characterized Marine demand as mixed but comparatively less volatile than towables.

Guidance Cut Indicates Softer Demand

Winnebago updated its fiscal 2026 guidance, lowering expectations for revenues and earnings amid weaker demand visibility. The company now expects revenues between $2.65 billion and $2.75 billion.

Hughes said fourth-quarter sales are expected to decline sequentially and fall in the double digits year over year, driven by continued dealer inventory management. He expected margins to remain relatively stable due to cost actions offsetting volume deleverage.

Cash flow generation remains a key focus, with management highlighting further working capital improvement opportunities in the fiscal fourth quarter. Net leverage increased slightly to 3 times due to lower EBITDA.

Dealers Tighten Orders as Inventory Discipline Intensifies

Analysts from Baird and Jefferies focused on dealer behavior and inventory discipline across the channel. Management confirmed dealers are prioritizing turns and cash flow over new inventory accumulation.

Happe described dealer sentiment as disciplined but cautious, with model year 2027 ordering slower than recent cycles. He emphasized that inventory quality and turns are now more important than shipment volume.

Pricing strategy was also a key focus in Q&A, with management noting variability across brands depending on cost pressure and competitive dynamics. Adjustments ranged from low single digits to high single digits, depending on segment conditions.

Operational Discipline and Cost Actions Intensify

Management reiterated that cost containment and footprint optimization are accelerating across both RV segments. Hughes noted ongoing actions to reduce excess capacity and improve manufacturing efficiency into fiscal 2027.

Happe highlighted strategic sourcing initiatives aimed at lowering material costs and improving supplier alignment. He stressed that procurement scale and SKU harmonization remain central to margin defense.

The company also emphasized SG&A discipline, with cost reductions helping offset top-line pressure. Management framed these actions as critical to sustaining profitability through a prolonged demand cycle.

Closing Outlook Points to Controlled Positioning Strategy

Winnebago leadership maintained that current conditions remain challenging but manageable through disciplined execution. The company continues to prioritize profitability over volume expansion across its portfolio.

Management reiterated focus on product innovation, affordability improvements and operational efficiency as key levers heading into fiscal 2027. Product launches were highlighted as long-term growth drivers.

Zacks Rank and Style Score

Winnebago carries a Zacks Rank #4 (Sell) at present, reflecting ongoing estimate pressure following the earnings miss versus the Zacks Consensus Estimate. The company has a Value Score of A, a Growth Score of B, a Momentum Score of D and a VGM Score of B.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The combination of a weak momentum profile alongside stronger value and growth characteristics signals mixed near-term sentiment. The Zacks Rank remains sensitive to future estimate revisions, which may shift following updated guidance and post-earnings analyst adjustments.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Winnebago Industries, Inc. (WGO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).