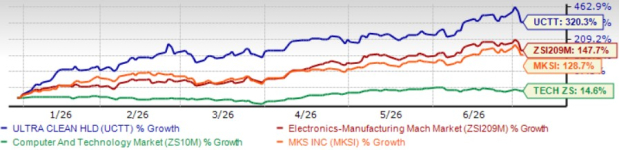

Ultra Clean Holdings UCTT shares have surged 320.3% year to date, outperforming the Zacks Electronics Manufacturing Machinery industry's return of 147.7% and the broader Computer and Technology sector's appreciation of 14.6%. The rally also outpaces peer MKS Inc. MKSI, which is up 128.7% over the same period.

The rally reflects UCTT's concentrated positioning in leading-edge foundry logic and advanced memory, two of the fastest-growing verticals in the semiconductor capital equipment market. Major equipment manufacturers such as Applied Materials AMAT and Lam Research LRCX source critical subsystems and components from UCTT. Demand from these customers is rising as they ramp tool shipments to meet accelerating fab investment, benefiting UCTT directly. Let us find out whether investors should buy UCTT stock right now.

UCTT’s Price Performance

Image Source: Zacks Investment Research

UCTT Benefits From the Fab Investment Cycle

UCTT designs and manufactures gas delivery systems, chemical delivery subsystems, precision cleaning solutions and other high-value components that are integrated directly into semiconductor fabrication equipment, positioning the company close to the equipment build cycle. As leading customers such as Applied Materials and Lam Research increase tool production to support advanced chip manufacturing, Ultra Clean benefits from rising demand for its critical subsystems and manufacturing services.

The current semiconductor investment cycle is being driven by artificial intelligence infrastructure, leading-edge foundry logic, high bandwidth memory and advanced packaging, all of which require increasingly sophisticated wafer fabrication equipment. Industry-wide wafer fabrication equipment spending is projected at $140 billion to $145 billion in 2026 after growing 18% to 20% in 2025. UCTT's customers have pointed to spending growth of at least 15% in 2027, supported by easing memory supply constraints as major producers invest in new fabrication plants and upgrade existing facilities. This is unlocking additional leading-edge factory launches and expanding the addressable opportunity for UCTT.

Ultra Clean's services business provides another long-term growth driver because it is linked to wafer starts rather than new equipment purchases alone. As fabs operate at higher utilization and process greater wafer volumes, services demand increases alongside equipment shipments, creating a more resilient revenue stream throughout the semiconductor cycle.

UCTT Ramps Up to Expand Market Share

Beyond favorable industry conditions, Ultra Clean is strengthening its competitive position through its UCT 3.0 strategy, which focuses on ramp readiness, the MPX new product introduction framework and digital transformation. These initiatives are designed to accelerate customer production ramps, improve manufacturing efficiency and position UCTT to capture a larger share of next-generation semiconductor equipment programs.

The MPX framework enables UCTT to co-innovate with customers earlier in the product development cycle, compressing new product introduction timelines and strengthening supply chain responsiveness. By expanding regional engineering capabilities and aligning manufacturing closer to customer facilities, UCTT is enhancing its ability to support leading customers such as Applied Materials and Lam Research as they transition to more advanced process nodes and ramp up AI-driven semiconductor equipment production.

UCTT's global manufacturing footprint currently supports approximately $3 billion in annual revenues and can scale to nearly $4 billion with modest incremental capital investment, providing ample capacity to meet rising customer demand while improving operating leverage. This scale advantage is notable in a supply landscape that includes larger diversified players such as MKS Inc., which spans vacuum solutions, power delivery and photonics across a wider set of end markets.

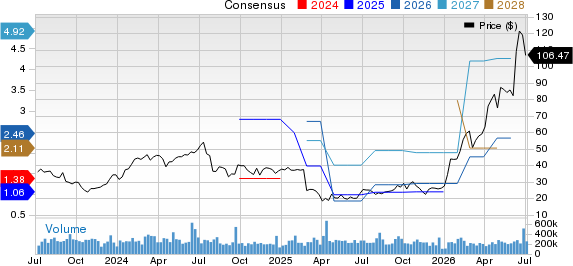

The Zacks Consensus Estimate for 2026 EPS is pegged at $2.46 per share, up 11 cents over the past 30 days, indicating year-over-year growth of 134.3%.

Ultra Clean Holdings, Inc. Price and Consensus

Ultra Clean Holdings, Inc. price-consensus-chart | Ultra Clean Holdings, Inc. Quote

UCTT Trades at Attractive Valuations

Despite its strong year-to-date rally, UCTT continues to trade at an attractive valuation. The stock trades at a forward 12-month price-to-sales (P/S) multiple of 1.67X, well below the industry's 3.54X and the broader sector's 6.32X and peer MKS' 4.71X. This discount stands out given UCTT's improving earnings outlook, scalable manufacturing capacity and exposure to the AI-driven semiconductor investment cycle. Supported by long-standing relationships with Applied Materials and Lam Research, UCTT is well-positioned to sustain above industry growth.

UCTT’s P/S F12M Ratio

Image Source: Zacks Investment Research

Conclusion

Despite UCTT's remarkable rally year to date, the company's long-term growth story remains intact. Rising wafer fabrication equipment spending and AI-driven semiconductor investments continue to create favorable demand conditions. UCTT's UCT 3.0 strategy and strong customer relationships should support additional market share gains. With the stock trading at a valuation below the industry and sector averages, UCTT remains a compelling buy for investors seeking exposure to the semiconductor capital equipment supply chain.

Ultra Clean sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ultra Clean Holdings, Inc. (UCTT): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

MKS Inc. (MKSI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).