BXP BXP is a leading office REIT that owns, develops and manages premium workplaces across six major U.S. gateway markets. Its portfolio includes office, retail, residential and hotel properties, with office assets generating most of its revenues. The company is known for high-quality buildings and long-term tenant relationships. Recent leasing activity has supported occupancy, while property sales have strengthened liquidity and helped fund redevelopment and new projects. A strong balance sheet helps finance future growth plans.

However, office demand remains competitive, resulting in higher leasing incentives and slower occupancy gains. Large development projects carry execution and funding risks, while the lower dividend makes the stock less appealing for income-focused investors.

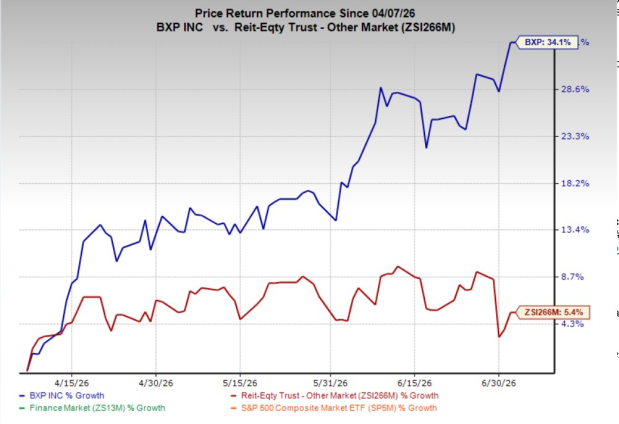

In the past three months, shares of this Zacks Rank #3 (Hold) company have gained 34.1% compared with the industry's growth of 5.4%.

Image Source: Zacks Investment Research

What Aids BXP?

BXP continues to benefit from steady demand for premium office space in major gateway markets. During the first quarter of 2026, the company completed 68 lease transactions covering more than 1.1 million square feet, with a weighted-average lease term of 8.7 years. Overall portfolio occupancy improved 70 basis points from the previous quarter to 87.4%, and the leased rate increased 150 basis points to 90.9%. Around 1.6 million square feet of signed leases have yet to begin, with nearly 90% expected to commence by the end of 2026.

The company also benefits from a diversified tenant base that provides stable rental income. As of March 31, 2026, the top 20 tenants accounted for 29.09% of BXP's share of annualized rental obligations, while their weighted-average remaining lease term was 8.9 years. This balanced tenant mix helps reduce dependence on any single customer and supports predictable cash flows.

BXP’s disciplined capital allocation strategy further strengthens its position. Since the September 2025 investor conference, aggregate net proceeds have totaled about $1.2 billion, and management continues to target approximately $1.9 billion by 2028 through additional asset sales. With several additional assets under contract and more being marketed, ongoing dispositions can help fund strategic priorities while easing leverage over time.

Growth is also supported by an active development pipeline and a strong balance sheet. BXP has six office, life science and residential projects under development totaling 3.4 million square feet, representing about $3.6 billion of investment, with 61% pre-leased as of April 24, 2026. These projects are expected to add nearly $300 million to BXP's share of cash NOI after stabilization. At the same time, the company ended the first quarter with $2.1 billion of liquidity, including about $0.6 billion in cash and $1.5 billion of available revolving credit capacity. BXP’s share of net debt to EBITDAre (annualized) was 8.50X, and fixed charge coverage was 2.40X as of March 31, 2026.

What’s Hurting BXP?

BXP continues to face intense competition from other office landlords, making it harder to increase rents and retain tenants without offering concessions. At the end of the first quarter of 2026, the portfolio was 90.9% leased but only 87.4% occupied, indicating that a sizeable portion of signed leases had not yet started.

The company's development pipeline also brings execution risk. It has six projects totaling 3.4 million square feet, representing about $3.6 billion of investment. The flagship 343 Madison Avenue project is scheduled for completion in 2029, and any delays in leasing, financing or recapitalization could postpone stabilization and put pressure on FFO.

BXP's dividend is less attractive after the 2025 reduction. The quarterly dividend was cut to 70 cents per share, down 27.4% from the previous level. As of March 31, 2026, the annualized dividend stood at $2.80 per share, offering a 5.4% yield. While the lower payout supports the balance sheet, it may reduce the stock's appeal for income-focused investors.

Stock to Consider

Some better-ranked stocks from the other REIT sector are American Healthcare REIT AHR and Apple Hospitality REIT APLE, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for AHR’s 2026 FFO per share has moved up marginally to $2.07 over the past month.

The consensus estimate for APLE’s 2026 FFO per share has moved up marginally to $1.58 per share over the past month.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

BXP, Inc. (BXP): Free Stock Analysis Report

Apple Hospitality REIT, Inc. (APLE): Free Stock Analysis Report

American Healthcare REIT, Inc. (AHR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).