Zeta Global Holdings Corp. ZETA is entering the rest of 2026 with a clear growth story and a less settled margin story. Its AI-powered marketing platform is gaining traction as enterprises consolidate vendors.

That matters because usage, revenue and platform depth are improving together. The question is whether Zeta can turn those gains into steadier profitability as agency-led business ramps through higher-cost channels.

What is Driving ZETA Growth Now?

Zeta’s growth signals remain broad-based. Revenues increased 50% year over year in the first quarter of 2026, with nine of its top 10 industries growing more than 20%. Its sales pipeline expanded roughly 40%.

The demand profile points to enterprise consolidation rather than a narrow product cycle. Customers are using Zeta across email, connected TV, mobile and social as they seek fewer vendors, faster execution and clearer performance measurement.

The Trade Desk, Inc. TTD offers a useful comparison of digital advertising platforms, while LiveRamp Holdings, Inc. RAMP fits the discussion because data collaboration and identity remain central to marketing technology workflows.

How Zeta is Building Deeper Platform Use

Athena is becoming more than a feature layered onto the existing platform. Zeta made Athena generally available to all enterprise customers in the first quarter of 2026, and agentic interactions rose more than sevenfold in the first week.

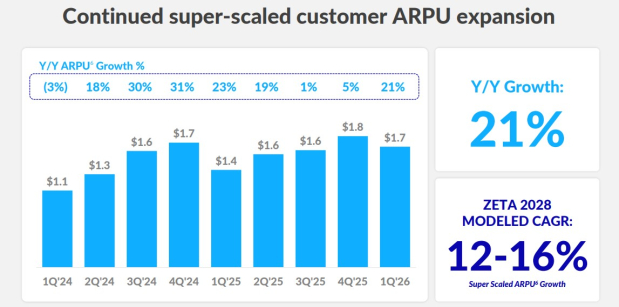

The usage data suggest customers are expanding within the platform. Super-scaled average revenue per user rose 21% year over year to $1.7 million, while multi-use-case customers increased more than 50% and customers using more than three channels rose roughly 40%.

That pattern supports the view that platform depth and customer lifetime value may be improving together. If customers automate more workflows across acquire, grow and retain use cases, Athena could help widen deal sizes, although 2026 guidance assumes minimal contribution.

Why ZETA Margins Face Near-Term Pressure

The margin debate is the main offset to the growth case. In the first quarter of 2026, GAAP cost of revenue rose to 41% as new agency wins initially ramped through social channels, a mix with less favorable gross economics.

Adjusted earnings before interest, taxes, depreciation and amortization margin was 16.7%, down 100 basis points year over year. That decline came even as adjusted earnings before interest, taxes, depreciation and amortization increased 42%.

Management expects social-led agency activity to become accretive to adjusted earnings before interest, taxes, depreciation and amortization and free cash flow as spending shifts into Zeta-owned channels. If onboarding remains weighted toward social, margins could lag expectations into the early second half of 2026.

What Recent Zeta News Means for Investors

On June 23, 2026, Zeta and Palantir announced a partnership to create an AI infrastructure layer connecting operational intelligence, customer intelligence and marketing execution.

Zeta also expanded Athena to agencies on June 18, 2026, with Athena for Insights and Measurement available in beta to agency partners. That could broaden distribution, although conversion into paid deployments remains an execution item.

The company’s participation in Snowflake-led Open Semantic Interchange adds another layer to the strategy. The initiative aims to improve interoperability across AI and analytics tools, which could reduce integration friction for enterprise customers.

How ZETA Signals Fit the Thesis

Zeta’s business setup looks promising, but the stock still carries execution risk. Growth is broad, Athena usage is rising and recent partnerships may improve distribution and interoperability, yet margins remain a near-term constraint.

ZETA currently carries a Zacks Rank #4 (Sell), reflecting weak earnings estimate revision trends over the next 1 to 3 months. That rank tempers the appeal of operating momentum, especially with the current-year earnings estimate down 1.1% over the past four weeks.

The Style Scores show a split picture. ZETA has a Growth Score of A, reflecting favorable growth characteristics, but a Momentum Score of F, indicating weak timing characteristics. Its Value Score of D limits the valuation argument, while the VGM Score of B supports a better combined profile.

For investors, the signal is not one-sided. The business story supports continued attention, but the Zacks Rank and weaker Momentum Score suggest patience may be warranted until margin execution and estimate revisions improve.

ZETA currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zeta Global Holdings Corp. (ZETA): Free Stock Analysis Report

The Trade Desk (TTD): Free Stock Analysis Report

LiveRamp Holdings, Inc. (RAMP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).