The AI chip market is increasingly emerging as a long-term investment opportunity, with the rising adoption of AI innovation and accelerating digital transformation. According to Roots Analysis, the market is projected to expand at a CAGR of 24.29% through 2040 from an estimated $100 billion in 2026. Taiwan Semiconductor Manufacturing Company TSM, or TSMC, and Intel INTC remain two closely watched names in this space.

TSMC has operated a pure-play foundry business model since its inception, manufacturing semiconductors based on proprietary integrated circuit designs provided by its customers. The products serve a broad range of end markets, including high-performance computing (HPC), smartphones, the Internet of Things (IoT), automotive and digital consumer electronics (DCE).

On the other hand, Intel designs, manufactures and markets CPUs and other semiconductor solutions used by consumers, enterprises, governments and educational organizations worldwide. The company is also growing its external foundry business by leveraging its U.S.-based capabilities in leading-edge semiconductor process technology, R&D, manufacturing and advanced packaging.

Let’s take a closer look at how the two companies stack up against each other.

Reasons to Stay Bullish on TSMC

According to TSMC, robust AI-related demand continues to fuel demand for its leading-edge silicon. Management is confident in the multiyear AI megatrend, with semiconductor demand expected to remain fundamental as cloud service providers offer a strong signal and positive outlook. The company views higher capital spending as a reflection of stronger growth opportunities. Backed by its technology leadership and manufacturing expertise, TSMC is well-placed to capture long-term structural demand driven by 5G, AI and high-performance computing.

TSMC’s first-quarter 2026 revenues increased 6.4% sequentially to $35.9 billion, slightly ahead of its guidance. The top line surpassed the Zacks Consensus Estimate by 1.13%. Gross and operating margins increased 390 basis points (bps) and 410 bps, respectively, on a sequential basis, led by cost improvement efforts, a high-capacity utilization rate, favorable foreign exchange and operating leverage.

TSMC's 2-nanometer (N2) technology has entered high-volume manufacturing with good yields and is ramping up successfully across multiple phases at both Hsinchu and Kaohsiung sites, supported by strong demand from both smartphone and HPC AI applications.

The company is also expanding its global 3-nanometer (N3) capacity to meet the strong demand in AI applications, marking a departure from its usual practice of not adding capacity once a node reaches its target level. TSMC is also seeing a high level of customer interest and engagement from both smartphone and HPC applications for its A14 technology, with volume production scheduled for 2028. Featuring the company’s second-generation nanosheet transistor structure, A14 is expected to provide performance and power benefits over N2 to address the sensible need for high-performance and energy-efficient computing.

However, the initial ramp-up of N2 technology is expected to dilute gross margin by 2%-3% in 2026. Potential increases in prices for certain chemicals and gases due to Middle East tensions may also affect TSMC’s profitability.

Reasons to Stay Bullish on Intel

The company believes it is well-positioned to capitalize on the AI-driven semiconductor market, whose total addressable market is approaching $1 trillion. Management also noted that AI is expanding into the real world toward a more distributed inference and reinforced learning workloads like agentic, physical AI and robots and edge AI, with the shift already beginning to contribute to the financial results.

Intel reported first-quarter 2026 revenues of $13.6 billion, up 7% year over year and surpassing the Zacks Consensus Estimate by 10.09%. Driven by strong demand, improved product mix and pricing actions. The company’s collective AI-driven businesses now represent 60% of revenues and grew 40% year over year. Adjusted gross margin reached 41%, nearly 650 bps above guidance, while adjusted earnings per share (EPS) came in at 29 cents, exceeding both the company’s breakeven guidance as well as the Zacks Consensus Estimate of 1 cent per share.

Demand continues to outpace supply for all of Intel’s businesses, especially for Xeon server CPUs, where momentum is expected to sustain this year and beyond. Intel 3-based Xeon 6 and Intel 18A-based Core Series 3 products have entered full-volume production ramp-up, marking the company’s fastest new product ramp-up in five years.

With customers increasingly deploying server CPUs alongside accelerators, CPU-anchored architecture remains the backbone of AI computing in production. The trend supports Intel’s x86 ecosystem and positions its CPU franchise as a key long-term growth engine.

The company also sees rapid AI infrastructure deployment as a meaningful opportunity for its external foundry business. Intel 4, Intel 3 and 18A yields are running ahead of internal projections, signaling an inflection in execution and factory finished good output. Intel is also making steady progress in its advanced packaging technologies, including additional growth in customer backlog during the first quarter.

How Do Estimates Compare for TSM & INTC?

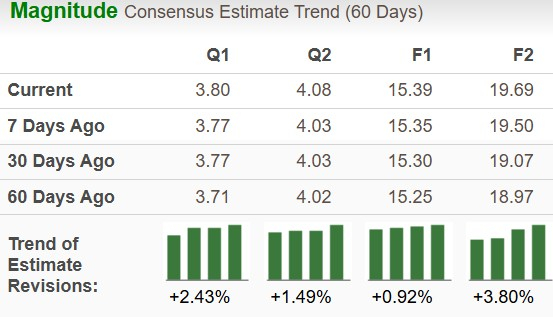

The Zacks Consensus Estimate for TSMC’s 2026 EPS currently stands at $15.39, implying a 44.5% jump over 2025. The estimate has been revised upward in the past 60 days.

Image Source: Zacks Investment Research

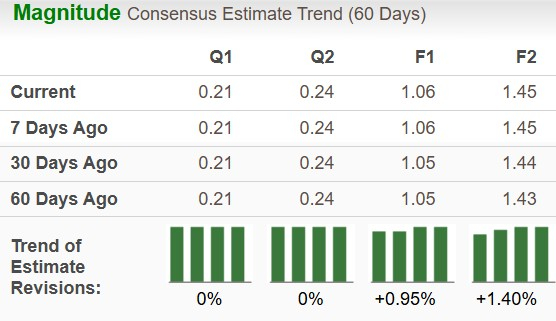

The consensus mark for Intel’s 2026 EPS implies year-over-year growth of 152.4% to $1.06. The estimate has moved upward in the past 60 days.

Image Source: Zacks Investment Research

TSM & INTC: Price Performance and Valuation

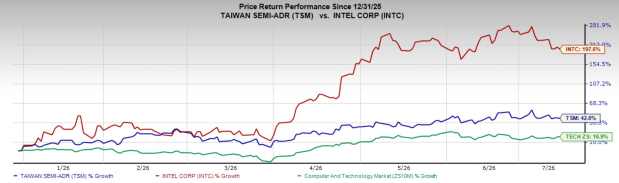

So far this year, TSMC shares have advanced 42.8%, while Intel has surged 197.6%. Both have comfortably outperformed the Zacks Computer and Technology sector’s 16.9% gain.

Image Source: Zacks Investment Research

TSM shares are trading at a forward, five-year Price/Sales (P/S) of 12.20X, while INTC sits at 8.97X.

Image Source: Zacks Investment Research

Conclusion

Intel, sporting a Zacks Rank #1 (Strong Buy) at present, delivered growth across its AI-driven businesses in its most recent quarterly results, along with stronger margins and earnings. The company’s CPU franchise remains well-positioned as anchored architecture underpins the AI computing in production. It is also progressing well with its A14 technology development and is likely to extend the company’s technology leadership position.

TSMC, carrying a Zacks Rank #2 (Buy), continues to benefit from the robust AI-driven demand for its leading-edge process technologies. The first-quarter results highlighted sequential revenue growth and margin expansion. Its N2 and A16 technologies support the growing demand for energy-efficient computing.

Earnings estimates for both companies are trending higher. While both TSM and INTC offer compelling investment opportunities, Intel’s year-to-date stock performance and relatively cheaper valuation give it an edge.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intel Corporation (INTC): Free Stock Analysis Report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).