Royal Caribbean Cruises Ltd. RCL is currently trading at a discount compared with the Zacks Leisure and Recreation Services industry, the broader Zacks Consumer Discretionary sector and the S&P 500 Index, with a forward 12-month price-to-earnings (P/E) ratio of 15.29X. The industry’s average currently is 16.82X, with the sector’s valuation at 16.36X and the S&P 500 Index at 21.26X.

Image Source: Zacks Investment Research

Royal Caribbean’s discounted valuation reflects a favorable long-term demand backdrop despite recent market concerns. Consumer demand for cruise vacations remains healthy, supported by record booking activity, resilient onboard spending and growing engagement across the company's digital and loyalty platforms. Investments in exclusive destinations, newer ships and technology initiatives further strengthen Royal Caribbean's competitive position and support long-term revenue and earnings growth.

At the same time, investors remain cautious about several near-term headwinds. Higher fuel costs, geopolitical developments affecting Mediterranean and West Coast Mexico itineraries, and elevated airfare costs have weighed on yield expectations for parts of 2026. While booking trends have improved and the broader demand environment remains healthy, these factors could continue to create earnings volatility over the near term.

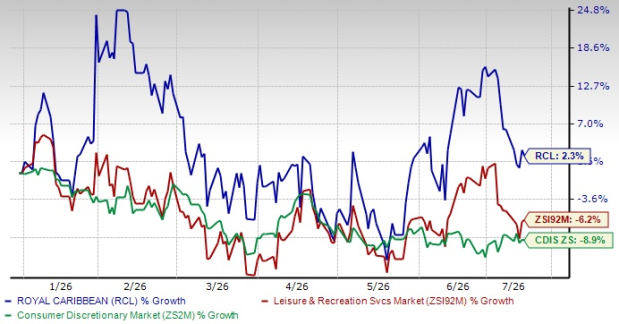

Shares of this Royal Caribbean have gained 2.3% so far in 2026, outperforming the industry and broader sector, as evidenced by the chart below.

RCL Stock’s Year-to-Date Price Performance

Image Source: Zacks Investment Research

Let us take a closer look at the factors shaping Royal Caribbean stock's prospects.

Record Wave Season Strengthens RCL’s Revenue Visibility

Strong consumer demand supported another record Wave Season for Royal Caribbean in the first quarter of 2026. The company reported revenue growth of 11% year over year while delivering more than 2.5 million vacations during the quarter. The book position remained within historical load factor ranges at record pricing, while revenue performance also benefited from healthy onboard spending and consistent demand across the company's vacation brands.

The strong booking environment provides greater visibility into future revenue generation despite near-term geopolitical uncertainties. Healthy pricing, resilient consumer demand and limited remaining inventory for upcoming sailings position Royal Caribbean to benefit from sustained travel demand while supporting another year of double-digit revenue and earnings growth.

Digital Strategy Enhances Royal Caribbean’s Guest Monetization

Growing adoption of digital platforms is strengthening Royal Caribbean's ability to engage guests and expand onboard spending. In the first quarter of 2026, digital booking penetration remained well above pre-pandemic levels, with monthly active app users increasing fivefold compared with 2019. App adoption exceeded 90%, while the pre-cruise booking engine achieved more than 70% penetration. More than half of onboard revenues were booked before guests boarded through digital channels.

Earlier guest engagement allows the company to personalize vacation experiences while increasing pre-cruise purchases and onboard spending opportunities. Continued investment in artificial intelligence and digital capabilities should further improve customer engagement, strengthen revenue per guest and enhance operating efficiency across the vacation ecosystem.

Loyalty Ecosystem Expands RCL’s Long-Term Demand Base

Royal Caribbean is strengthening customer retention through an increasingly connected loyalty platform. In the first quarter of 2026, approximately 40% of guests came from the company's existing customer base, supported by cross-brand bookings following the introduction of Status Match and broader loyalty initiatives. Cardholder accounts have also more than doubled since 2019 after expanding the Royal ONE co-branded credit card program.

A larger base of repeat guests strengthens demand quality while reducing customer acquisition costs. Repeat guests spend approximately 25% more than first-time guests, while the expanding loyalty ecosystem encourages vacationers to travel across multiple brands, increasing customer lifetime value and creating additional opportunities to drive higher onboard and pre-cruise spending.

Cost Discipline Strengthens Royal Caribbean’s Margin Outlook

Operational efficiency remained an important contributor to Royal Caribbean’s first-quarter performance. In the first quarter of 2026, adjusted EBITDA margin expanded more than 300 basis points (bps) year over year to 38%, supported by favorable cost performance and continued efficiency initiatives. Net cruise costs excluding fuel also performed better than expected during the quarter.

The company remains focused on improving productivity through technology, artificial intelligence and operational efficiencies without compromising the guest experience. Maintaining disciplined cost control alongside moderate capacity growth and healthy pricing should support continued margin expansion and stronger cash flow generation over time.

Royal Caribbean vs. Peers: Competition in the Cruise Industry

Royal Caribbean operates in a highly competitive global cruise industry alongside major players such as Carnival Corporation CCL and Norwegian Cruise Line Holdings Ltd. NCLH. All three companies are benefiting from resilient cruise demand, higher onboard spending, investments in private destinations and ongoing fleet expansion. However, each company is pursuing a different strategy to strengthen its market position.

Carnival is strengthening its competitive position through investments in exclusive destinations, disciplined fleet expansion and commercial initiatives aimed at improving pricing and onboard spending. The company is also enhancing cost efficiency while expanding its destination portfolio, including Celebration Key and RelaxAway, Half Moon Cay, to support long-term demand. Record customer deposits, a longer booking curve and continued investment in guest experiences further reinforce Carnival's position in the global cruise industry.

Norwegian Cruise Line Holdings is focused on improving execution through revenue management enhancements, marketing initiatives and organizational changes. The company is optimizing its cost structure, streamlining operations and investing in Great Stirrup Cay and new ships to strengthen demand. Norwegian Cruise Line Holdings is also building a stronger operating foundation through disciplined cost management and commercial improvements as it works to enhance long-term performance.

Near-Term Headwinds Remain for Royal Caribbean

Despite strong underlying demand, Royal Caribbean faces a few near-term challenges. Geopolitical developments have moderated bookings for high-yield Mediterranean itineraries and select West Coast Mexico sailings, prompting the company to lower its full-year net yield expectations. Although booking trends have improved in recent weeks, any further disruptions could affect demand for international itineraries.

Higher fuel prices also remain a key headwind. Even with nearly 60% of 2026 fuel consumption hedged, the company expects fuel costs to reduce full-year earnings by approximately 62 cents per share. Elevated airfares, airline capacity constraints and travel disruptions could further weigh on booking trends, particularly for long-haul destinations.

Earnings Estimate Revision of RCL

Royal Caribbean’s earnings estimate for 2026 has edged lower over the past seven days to $17.30 per share, while the 2027 estimate has remained unchanged at $19.86. The estimated figures for 2026 and 2027 still imply year-over-year growth of 10.6% and 14.8%, respectively.

Image Source: Zacks Investment Research

Should You Buy, Sell or Hold RCL Stock?

Royal Caribbean continues to benefit from healthy cruise demand, record pricing, strong guest spending and growing engagement across its digital and loyalty platforms. Investments in exclusive destinations, operational efficiencies and technology initiatives further strengthen the company's long-term growth prospects. Combined with a discounted valuation relative to the industry, these factors provide an attractive foundation for value creation.

However, near-term uncertainties remain. Higher fuel costs, geopolitical developments affecting certain itineraries and elevated travel costs have tempered the company's earnings outlook for 2026, while recent estimate revisions reflect these challenges. With a Zacks Rank #3 (Hold) at present, Royal Caribbean appears suitable for investors already owning the stock, while prospective investors may prefer to wait for a more favorable entry point or greater clarity on these near-term headwinds. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL): Free Stock Analysis Report

Carnival Corporation (CCL): Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).