Abbott Laboratories ABT is slated to report its second-quarter 2026 results on July 16, before the opening bell.

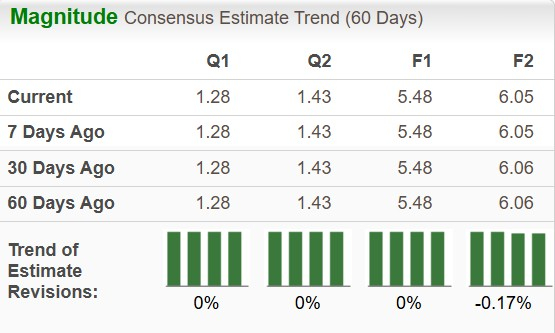

The Zacks Consensus Estimate for the company’s second-quarter earnings per share (EPS) suggests 1.6% year-over-year growth to $1.28. The estimate has remained constant in the past 60 days. The consensus mark for second-quarter revenues currently stands at $12.48 billion, implying a 12% increase over the prior-year period.

Image Source: Zacks Investment Research

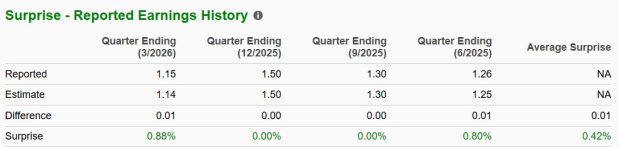

In the trailing four quarters, the company topped earnings estimates twice and broke even on two occasions, the average surprise being 0.42%.

Image Source: Zacks Investment Research

Q2 Earnings Whispers for Abbott

Per our proven model, a stock with a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold), along with a positive Earnings ESP, has a higher chance of beating estimates. This is not the case here, as you can see below.

Earnings ESP: Abbott has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

Zacks Rank:The company currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks Rank #1 stocks here.

Factors Likely to Have Shaped ABT’s Q2 Performance

Diagnostics

Within this segment, Abbott may have delivered mixed performance in the second quarter. Rapid and Molecular Diagnostics are likely to have continued to face reduced demand for respiratory virus testing. At the same time, steady demand for the Core Lab diagnostic tests may have been a tailwind, with strong performance across the United States, Europe and Latin America.

Following the acquisition of Exact Sciences, Abbott added the Cancer Diagnostics business, expanding into one of the fastest-growing areas of healthcare. We assume the division to have favorably impacted the quarter’s results, driven by the Cologuard colorectal cancer (CRC) test momentum and contributions from the international markets.

A positive development in the quarter was the American Cancer Society’s updated CRC screening guidelines, reaffirming Cologuard and Cologuard Plus as preferred non-invasive screening options for adults aged 45 and older who are at average risk. This is expected to have positively boosted adoption trends and revenues.

The Zacks Consensus Estimate anticipates Diagnostics revenues to increase 41.6% year over year.

Established Pharmaceutical Products (“EPD”)

The segment is expected to have maintained its growth momentum in key emerging markets, supported by favorable long-term health care, economic and demographic trends, with a broad product offering across five therapeutic areas. The biosimilars portfolio, which has expanded to include several market-leading oncology therapies, may have been a positive driver as well for the segment’s top line.

Going by the Zacks Consensus Estimate, EPD revenues are likely to grow 6.6% from the prior-period levels.

Medical Devices

Abbott’s cardiovascular businesses are expected to have been the biggest contributor to Medical Devices’ top line in the second quarter of 2026.

Electrophysiology performance may have been boosted by contributions from the Volt and TactiFlex Duo pulsed field ablation (PFA) catheters. Rhythm Management likely continued to outpace the market, driven by the Aveir leadless pacemaker. Heart Failure business results may have benefited from the Heart Assist Devices portfolio.

In Vascular, the company secured FDA clearance and CE Mark for its next-generation Ultreon 3.0 Software in the quarter, bringing coronary imaging and AI-automated insights together in one system. The enhanced coronary portfolio likely contributed positively to the quarter’s results.

In Neuromodulation, Abbott’s rechargeable spinal cord stimulation device Eterna may have continued to see strong international adoption trends.

Further, the Diabetes Care business may have regained growth momentum following the easing of temporary headwinds, including a delay in the international tender renewal process and a challenging prior-period comparison.

The Zacks Consensus Estimate expects Medical Devices revenues to increase 8.5% year over year.

Nutrition

The segment is expected to have faced revenue pressure in the second quarter, as Abbott continues to transition toward a more sustainable balance between price and volume-driven growth. Sales volumes across both pediatric and adult nutritional product portfolios in the United States and internationally may have been lower. Although management reported early progress from these strategic actions in the previous quarter, it is yet to fully materialize.

The Zacks Consensus Estimate indicates Nutrition revenues will decline 4.3% year over year.

Abbott’s Peers Reporting Next Week

Quest Diagnostics DGX is set to report second-quarter 2026 results on July 23, before the opening bell. The company’s Diagnostic Information Services segment is expected to have maintained its growth momentum, supported by organic growth across the physician, hospital and consumer channels. Contributions from recent acquisitions may have been a key driver. Productivity gains from the company’s automation and AI initiatives are likely to have favored the bottom line.

Thermo Fisher TMO is also slated to report its 2026 second-quarter results before the market opens on July 23. Strength in the bioproduction and clinical research business, and the research and safety market channel may have supported the pharma and biotech end-market performance. Several recently launched high-impact innovations may have lifted revenues. The continued adoption of accelerated drug development offering is likely to have translated to share gain in its clinical research business.

ABT’s Price Performance & Valuation

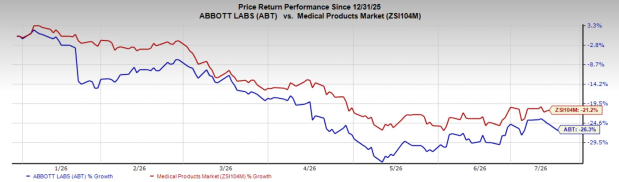

In the three months ended June 30, Abbott shares have dropped 11.4%, underperforming the industry’s 10.1% decline.

Image Source: Zacks Investment Research

In terms of valuation, Abbott trades at a forward five-year Price/Earnings (P/E) of 15.93X, lower than its median of 23.28X and 16.21X industry average.

Image Source: Zacks Investment Research

Endnote

Abbott is well-positioned to benefit from strength across several of its key businesses in the second quarter of 2026, including Core Lab Diagnostics, EPD and Electrophysiology. The newly added Cancer Diagnostics portfolio is also expected to have contributed. Nutrition may have continued to navigate the near-term impact of its pricing and volume transition, with the benefits of these strategic actions expected to build over time. In the trailing four quarters, Abbott beat earnings estimates twice and came in line on two occasions.

Despite its recent underperformance, ABT is trading at a relatively cheaper valuation. Given Abbott’s strong fundamentals and diversified growth drivers, we believe existing shareholders should continue to retain their positions to enjoy long-term gains.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abbott Laboratories (ABT): Free Stock Analysis Report

Quest Diagnostics Incorporated (DGX): Free Stock Analysis Report

Thermo Fisher Scientific Inc. (TMO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).