Texas Instruments Incorporated TXN is entering a new phase of its investment cycle, with capital expenditures expected to decline after several years of heavy spending on manufacturing expansion. This shift could significantly improve the company’s free cash flow and strengthen its ability to return more capital to shareholders.

Over the past few years, Texas Instruments invested aggressively in new 300-millimeter wafer fabrication plants and assembly and test facilities to expand internal manufacturing capacity. These investments temporarily weighed on free cash flow but positioned the company to support future demand while lowering production costs. In 2025, capital expenditures totaled approximately $4.55 billion.

The spending pace is now easing. In the first quarter of 2026, Texas Instruments’ capital expenditure nearly halved to $676 million from $1.12 billion in the year-ago quarter. Management expects 2026 capital expenditures to be between $2 billion and $3 billion, about a 34% to 56% reduction from the 2025 level. While some investment will continue to support additional assembly and test capacity, the company believes most of its major manufacturing infrastructure is already in place. This should allow a larger share of operating cash flow to convert into free cash flow.

The benefits are already becoming visible. In the first quarter of 2026, Texas Instruments generated free cash flow of $1.4 billion, a robust improvement from a negative $14 million in the year-ago quarter. Trailing 12-month free cash flow also increased to $4.35 billion in the first quarter of 2026 from $1.72 billion a year earlier. Free cash flow margin also improved sharply to 23.6% from 10.7%, supported by stronger revenue growth and lower capital intensity.

Management believes free cash flow per share could exceed $8 in 2026 if current demand trends continue. Combined with improving industrial demand, stronger data center spending and better factory utilization, lower capital expenditures could further strengthen Texas Instruments’ cash generation, giving the company greater flexibility to fund dividends, repurchase shares and invest in future growth. In the trailing 12 months, Texas Instruments returned $6.43 billion to shareholders through share buybacks and dividend payments.

TXN’s Rivals Are Also Balancing CapEx and Cash Generation

Texas Instruments’ main competitors, Analog Devices, Inc. ADI and NXP Semiconductors N.V. NXPI, are also balancing their capital expenditures and cash flows.

Analog Devices has taken a disciplined approach to capital spending while maintaining strong cash flow. The company follows a hybrid manufacturing model that combines internal production with outsourced foundries, allowing it to keep capital expenditures relatively low.

This asset-light approach has helped Analog Devices consistently generate more than $3 billion in annual free cash flow while maintaining free cash flow margins above 30% over the past few years. The strong cash generation has enabled the company to steadily increase dividends and repurchase shares without making large manufacturing investments.

NXP Semiconductors also focuses on disciplined capital allocation to maximize cash flow. The company typically keeps annual capital expenditures at about a mid-single-digit percentage of revenue, well below the levels Texas Instruments has invested in recent years. This strategy has helped NXP Semiconductors consistently generate more than $2 billion in annual free cash flow, supporting regular dividends and sizable share repurchases.

TXN’s Price Performance, Valuation and Estimates

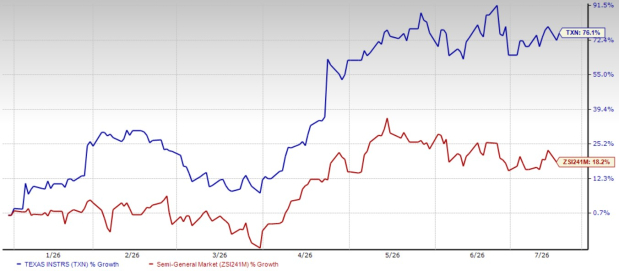

Shares of Texas Instruments have soared 76.1% year to date compared with the Zacks Semiconductor - General industry’s 18.2% growth.

Texas Instruments YTD Price Return Performance

Image Source: Zacks Investment Research

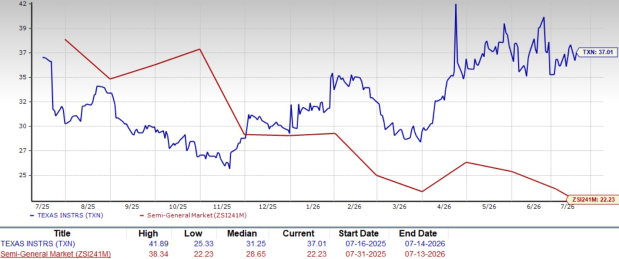

From a valuation standpoint, TXN trades at a forward price-to-earnings ratio of 37.01, significantly higher than the industry’s average of 22.23.

Texas Instruments Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Texas Instruments’ 2026 and 2027 earnings implies a year-over-year increase of 40.6% and 14.4%, respectively. Estimates for 2026 and 2027 have remained unchanged over the past 60 days.

Image Source: Zacks Investment Research

Texas Instruments currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

NXP Semiconductors N.V. (NXPI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).