ASE Technology Holding ASX and Lam Research LRCX are both important players in the semiconductor industry, but they operate in different parts of the supply chain. ASE Technology is a major player in outsourced semiconductor assembly and testing, offering advanced packaging and testing services for AI, high-performance computing and automotive chips, while Lam Research provides wafer fabrication equipment that enables chipmakers to manufacture advanced semiconductors.

Both ASX and LRCX are well-positioned to benefit from the rising demand for AI chips, as hyperscalers continue to increase investments in AI infrastructure. However, from an investment point of view, one stock offers a more favorable outlook than the other right now. Let’s break down their fundamentals, growth prospects, market challenges and valuation to determine which stock offers a more compelling investment case.

The Case for ASE Technology Stock

ASE Technology is benefiting from the growing demand for AI chip packaging. In the first quarter of 2026, ASX's Assembly, Testing and Materials (ATM) business performed better than expected, despite having fewer working days and did not see the usual seasonal slowdown. Management said AI-related products are changing the normal demand pattern, helping reduce the impact of seasonality on the business.

Advanced packaging continues to be the main growth driver. ASE reported record ATM revenues of NTD 112.4 billion in the first quarter, up 2% sequentially and 30% year over year. Higher factory utilization and a larger contribution from Leading Edge Advanced Packaging (LEAP) services were the key contributors to growth. The company said demand for AI and computing products remained strong, while growth in advanced packaging and wirebond services helped offset softer demand in some consumer markets.

ASE Technology is also increasing investments to support future growth. The company raised its 2026 capital spending plan and increased its LEAP revenue outlook by 10%. It now expects LEAP revenues to exceed $3.5 billion in 2026. Management said the additional investment will help expand capacity to meet growing customer demand and help drive further growth in the company's LEAP in the upcoming years.

The company is seeing demand not only from AI accelerator chips but also from AI-related power management, connectivity, sensors and edge devices. At the same time, it is expanding its advanced packaging technologies, including full-process packaging, CoWoS-like packaging and panel-level packaging, to support future AI applications. If AI infrastructure spending remains strong, ASE Technology is well-positioned to benefit from the growing demand for advanced semiconductor packaging.

The Case for Lam Research Stock

Lam Research expects its advanced packaging business to be one of its fastest-growing businesses in 2026. Revenues from the advanced packaging business are expected to grow more than 50% in 2026. Management said AI is increasing demand for advanced packaging because AI chips need higher performance, higher bandwidth and better power efficiency than traditional chips.

LRCX supplies equipment used in key advanced packaging processes, including through-silicon via etch and copper plating. These technologies are used to connect chips and memory more efficiently in AI systems. As semiconductor companies build more AI processors and high-bandwidth memory, they need more advanced packaging equipment, creating additional demand for Lam Research's products.

The advanced packaging business is already contributing to LRCX's growth. In the third quarter of fiscal 2026, foundry revenues increased 35% year over year, and management said advanced packaging remained a strong growth area. The company also continues to gain market share in its PECVD business, helped by demand for advanced packaging applications.

LRCX expects demand for advanced packaging to continue to grow as AI infrastructure spending increases. The company expects more chipmakers to adopt advanced packaging technologies as AI chips become more complex. This trend should position advanced packaging to become an important contributor to LRCX's revenue growth over the next few years.

However, risks and uncertainties related to trade restrictions on exporting semiconductor tools to China do not bode well for Lam Research. Management expects China revenues to decline in the fourth quarter of fiscal 2026, while China’s wafer fabrication equipment spending is expected to remain roughly flat year over year. Further, the company remains heavily exposed to memory spending cycles, particularly NAND and DRAM. Any slowdown in AI memory demand or delays in customer spending could hurt growth.

How do Earnings Estimates Compare for ASX & LRCX?

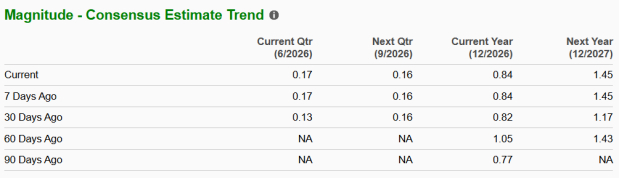

The Zacks Consensus Estimate for ASX’s 2026 and 2027 EPS is pegged at 84 cents and $1.45, respectively. The estimates for 2026 and 2027 have been revised up by 2.4% and 23.9%, respectively, over the past 30 days.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for LRCX’s fiscal 2026 and 2027 EPS is pegged at $5.68 and $7.93, respectively. The estimates for fiscal 2026 have remained unchanged over the past 30 days, while the same for fiscal 2027 have been revised up by 0.5% over the past seven days.

Image Source: Zacks Investment Research

ASX vs. LRCX: Price Performance and Valuation

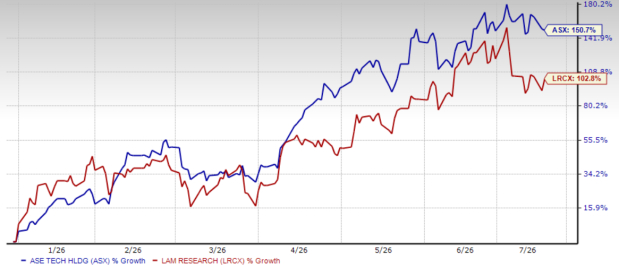

Year to date, shares of ASX and LRCX have surged 150.7% and 102.8%, respectively.

ASX Vs. LRCX: YTD Price Return Performance

Image Source: Zacks Investment Research

Currently, ASX is trading at a trailing 12-month P/S ratio of 4.20X, significantly lower than LRCX’s trailing 12-month P/S multiple of 20.07X. ASX’s reasonable valuation makes it more attractive for investors looking for value and stability.

ASX vs. LRCX: TTM 12-Month P/S Ratio

Image Source: Zacks Investment Research

Conclusion: ASX Has an Edge Over LRCX

Both ASX and LRCX are benefiting from growing demand for AI chips and advanced packaging. However, LRCX continues to face uncertainty related to semiconductor export restrictions to China and remains exposed to memory spending cycles, which could hurt the company’s prospects.

In contrast, ASE Technology continues to benefit from strong demand for AI chip packaging, supported by strong demand from AI and high-performance computing. Further, ASX’s reasonable valuation offers some downside protection as well, making the stock an attractive buy.

Currently, ASX sports a Zacks Rank #1 (Strong Buy), giving a clear edge over LRCX, which carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lam Research Corporation (LRCX): Free Stock Analysis Report

ASE Technology Holding Co., Ltd. (ASX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).