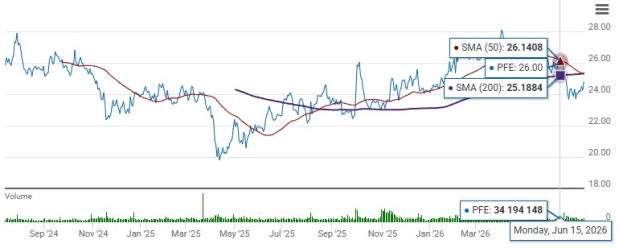

Pfizer’s PFE stock has been trading below both its 50-day and 200-day simple moving averages (SMAs) since mid-June, indicating continued caution among investors regarding the company's long-term growth outlook. While the stock has experienced periodic rebounds, the broader market remains focused on Pfizer's ability to generate consistent earnings growth as its COVID-related revenues fade gradually.

Trading below the 50-day SMA points to subdued near-term price momentum, whereas remaining below the 200-day SMA suggests that the stock is yet to establish a sustained long-term upward trend. Investors are closely watching whether Pfizer's expanding pipeline, recent product launches and cost-reduction initiatives can offset declining COVID-related sales and support a stronger earnings trajectory over the coming years.

To make an informed decision on whether to buy, sell or hold the stock in such a scenario, it is important to evaluate the company’s fundamentals by examining its key strengths and weaknesses.

Declining Sales of PFE’s COVID Products

During the pandemic, Pfizer generated extraordinary COVID-related sales from Comirnaty and Paxlovid. Those revenues have fallen sharply as the pandemic faded.

Sales of Pfizer’s COVID products, Comirnaty and Paxlovid, came down to around $11 billion in 2024 and $6.7 billion in 2025 from $56.7 billion in 2022. Sales of Comirnaty are declining due to a narrow recommendation for COVID vaccines in the United States, while Paxlovid is experiencing reduced demand from lower infection rates.

In 2026, Pfizer expects its COVID revenues to be around $5 billion, representing a decline from 2025 COVID sales of around $6.7 billion as COVID infection rates are expected to continue to decline.

PFE’s LOE Headwinds

Pfizer faces a significant patent cliff later this decade. Pfizer expects a significant negative impact on revenues from the loss of exclusivity (“LOE”) cliff in the 2026-2030 period as several of its key products, including Eliquis, Ibrance, Xeljanz and Xtandi, face patent expirations. The LOE cliff is expected to hurt sales by approximately $1.5 billion in 2026.

PFE’s 2026 Financial Outlook Dull

Pfizer’s revenue and earnings guidance for 2026 represents mostly flat to slightly negative growth.

The company expects total revenues for 2026 to be between $59.5 billion and $62.5 billion. The range represents a decline from 2025 revenues of $62.6 billion due to lower revenues from COVID products, Comirnaty and Paxlovid, and loss of revenues from the upcoming patent cliff.

In 2026, Pfizer expects adjusted earnings per share in the range of $2.80-$3.00, which represents a decline from 2025 EPS of $3.22 due to the dilutive impact of 3SBio and Metsera deals, lower COVID revenues and higher taxes.

However, not everything is going wrong at Pfizer. Let’s see the positives.

PFE’s New & Acquired Products Drive Top-Line Growth

Pfizer’s dependence on its COVID business has now reduced. Its non-COVID operational revenues are improving, driven by key in-line products like Vyndaqel, Padcev and Eliquis, new launches and newly acquired products like Nurtec and those from Seagen. In 2026, Pfizer expects its recently launched and acquired products to record continued double-digit growth.

The company is also trying to rebuild its pipeline through acquisitions. Seagen, Metsera and Biohaven are the most significant strategic acquisitions in recent years.

The company is rebuilding its pipeline in oncology and obesity, which it believes can drive growth in 2028 and beyond. Pfizer plans an extensive phase III program for berobenatide, its monthly GLP-1 receptor agonist added from last year’s Metsera acquisition, in 2026. Pfizer plans to start more than 20 obesity studies in 2026, including 10 phase III studies for berobenatide for obesity and obesity-related comorbidities, including knee osteoarthritis and obstructive sleep apnea. Pfizer is targeting the first of a series of potential approvals for berobenatide in 2028. However, in the obesity space, Pfizer lags far behind leaders like Eli Lilly LLY and Novo Nordisk NVO.

The company expects its recently launched and acquired products and a strong pipeline to help revive top-line growth toward the end of the decade.

Pfizer’s significant cost reduction and efforts to improve R&D productivity measures are also driving profit growth. Pfizer’s dividend yield stands at around 7%, which is also impressive.

PFE Enjoys a Strong Position in Oncology

Pfizer is one of the largest and most successful drugmakers in oncology. Its position in oncology was strengthened with the acquisition of Seagen in 2023.

Oncology sales comprise around 27% of its total revenues. Its oncology revenues grew 7% to $3.8 billion in the first quarter of 2026, driven by drugs like Lorbrena, the Braftovi-Mektovi combination and Padcev. Pfizer has also ventured into the oncology biosimilars space and markets six biosimilars for cancer.

Pfizer is also advancing its oncology clinical pipeline across areas such as breast, thoracic, gastrointestinal and blood cancer. Several oncology candidates have entered late-stage development. Pfizer plans to start four pivotal studies for PF-08634404, a dual PD-1/VEGF inhibitor in-licensed from Chinese biotech 3SBio in 2025.

By 2030, it expects to have eight or more blockbuster oncology medicines in its portfolio.

PFE Stock’s Price, Estimates & Valuation

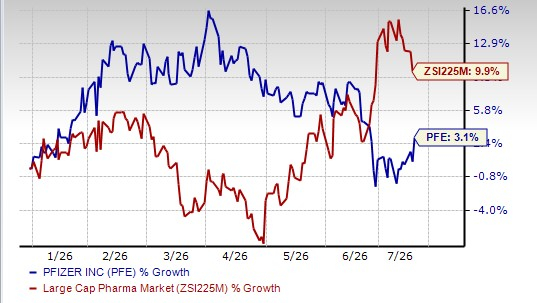

Pfizer’s stock has risen 3.1% so far this year compared with an increase of 9.9% for the industry.

PFE Stock Underperforms Industry

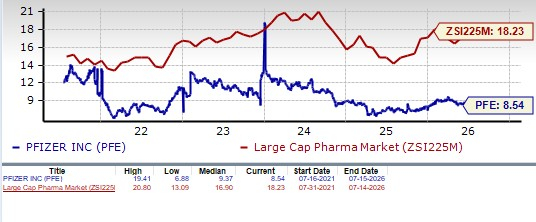

From a valuation standpoint, Pfizer appears attractive relative to the industry and is trading below its five-year mean. Going by the price/earnings ratio, Pfizer’s shares currently trade at 8.54 forward earnings, significantly lower than 18.23 for the industry as well as the stock’s five-year mean of 9.37. The stock is also trading below most large drugmakers like Lilly, Novo Nordisk, AstraZeneca, AbbVie, J&J and others.

PFE Stock Valuation

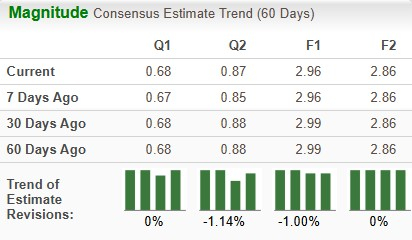

The Zacks Consensus Estimate for 2026 earnings has declined from $2.99 per share to $2.96 per share, while that for 2027 has been stable at $2.86 per share over the past 60 days.

PFE Estimate Movement

Stay Invested in PFE Stock

Pfizer is navigating a difficult transition following the sharp decline in COVID-related sales from Comirnaty and Paxlovid. The market is concerned about Pfizer’s ability to replace declining COVID-related revenues and offset upcoming patent expirations through new product launches, pipeline development and contributions from acquisitions.

Despite these challenges, Pfizer's valuation is relatively inexpensive compared with many large pharmaceutical peers, and the stock offers one of the highest dividend yields in the sector. The company is rebuilding its pipeline in oncology and obesity, which it believes can drive growth in 2028 and beyond. Although Pfizer’s 2026 sales guidance indicates minimal growth, the company expects a high single-digit revenue CAGR for five years starting in 2029.

Pfizer expects the growth to be driven by its advancing R&D pipeline and the continued progress of new and acquired products. If Pfizer can successfully execute on this strategy and generate meaningful growth from its newer assets and restore revenue growth, the shares could eventually recover above their long-term moving averages.

Long-term investors may consider retaining this Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pfizer Inc. (PFE): Free Stock Analysis Report

Novo Nordisk A/S (NVO): Free Stock Analysis Report

Eli Lilly and Company (LLY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).