Manulife Financial Corporation MFC closed at $33.76 on Tuesday, near its 52-week high of $38.72. This proximity underscores investor confidence. It has the ingredients for further price appreciation.

Shares of Manulife Financial are trading above the 200-day simple moving average (SMA) of $33.27, indicating solid upward momentum. SMA is a widely used technical analysis tool to predict future price trends by analyzing historical price data.

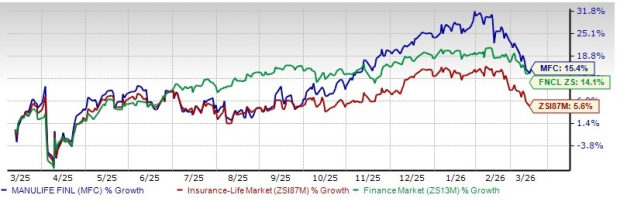

Shares of Manulife Financial have gained 15.4% in the past year, outperforming the industry’s growth of 5.6% and the Finance sector return of 14.1%.

Manulife Financial has outperformed its peers, including Primerica, Inc. PRI, Voya Financial, Inc. VOYA and Reinsurance Group of America, Incorporated RGA. Shares of RGA and VOYA have gained 10.1% and 1.8%, respectively, while PRI shares have lost 8.4% in the past year.

Image Source: Zacks Investment Research

With a capitalization of $56.59 billion, the average number of shares traded in the last three months was 2.3 million.

The life insurer has a solid track record of beating earnings estimates in two of the past four quarters and missing in the other two, with an average surprise of 3.63%.

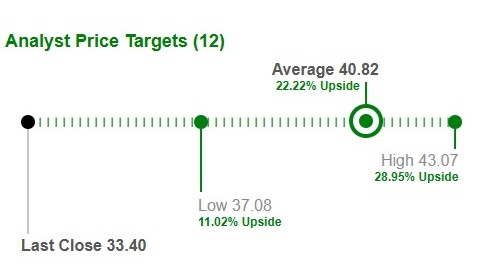

Average Target Price for MFC Suggests Upside

Based on short-term price targets offered by 12 analysts, the Zacks average price target is $40.82 per share. The average suggests a potential 22.2% upside from the last closing price.

Image Source: Zacks Investment Research

MFC’s Growth Projection Encourages

The Zacks Consensus Estimate for Manulife Financial’s 2026 earnings per share indicates a year-over-year increase of 8.9%. The estimate for 2027 earnings per share and revenues indicates an increase of 8.5% and 3.6%, respectively, from the corresponding 2026 estimates.

Optimist Analyst Sentiment on MFC

One of the two analysts covering the stock has raised estimates for 2026 and 2027 over the past 30 days. The Zacks Consensus Estimate for 2026 and 2027 earnings has moved up 1.2% and 1.1%, respectively, in the past 30 days.

Manulife Financial’s Higher Return on Capital

Return on equity in the trailing 12 months was 16.4%, better than the industry average of 15.6%. This highlights the company’s efficiency in utilizing shareholders’ funds.

Key Points to Note for MFC

Manulife is aggressively developing its business in Asia, which, in turn, is reaping solid operational results. Asia is a major contributor to the company’s earnings. New business growth in Asia has been aiding the company’s operational results. Thus, the insurer is continually scaling up its business across Asia. We believe MFC is well-positioned to benefit from continued business growth momentum, higher expected earnings on insurance contracts and higher expected investment earnings, with notable growth from the largest in-force business, Hong Kong and an expanding distribution network.

Manulife Financial is expanding its Wealth and Asset Management business and has identified Europe (and the wider EMEA market) as a significant growth area. It is making long-term investments in this region.

MFC has been accelerating growth in the highest-potential businesses. Its inorganic growth is impressive, as this life insurer prudently deploys capital in high-growth, less capital-intensive and higher-return businesses.

Banking on its sturdy capital position, MFC distributes wealth to shareholders through higher dividends and share buybacks. The company has increased its dividend at a seven-year CAGR of 10% and targets a 35-45% dividend payout over the medium term.

MFC is strengthening its balance sheet and thus targets a leverage ratio of 25%. Notably, its free cash flow conversion has remained more than 100% over the last few quarters, reflecting its solid earnings.

Conclusion

Manulife Financial is set to grow on solid Asia business, growing Wealth and Asset Management business, strong free cash flow conversion ratio and a solid capital position. A medium-term expense efficiency ratio target of less than 45%, banking on diligent expense management, should drive growth.

Consistent wealth distribution makes it an attractive pick for yield-seeking investors, and favorable ROE also poises MFC for growth. MFC also has a VGM Score of B. Stocks with a favorable VGM Score are those with the most attractive value, best growth and most promising momentum compared with peers.

Coupled with optimistic analyst sentiment and favorable growth estimates, the time appears right for potential investors to bet on this Zacks Rank #2 (Buy) insurer. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Manulife Financial Corp (MFC): Free Stock Analysis Report

Reinsurance Group of America, Incorporated (RGA): Free Stock Analysis Report

Primerica, Inc. (PRI): Free Stock Analysis Report

Voya Financial, Inc. (VOYA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).