The Goldman Sachs Group Inc. GS and Evercore Inc. EVR represent two distinct, top-tier investment banking (IB) models. Goldman represents the scale and diversification of a bulge-bracket bank, while Evercore offers the high-margin, focused model of a boutique advisory firm.

Both have shown resilience as merger and acquisition (M&A) and initial public offering (IPO) activity recovered in 2024-2025. With the IB outlook turning brighter, the main question is which stock offers the better risk-reward from here: Goldman or Evercore? Let us decipher this.

The Case for GS

Goldman continues to maintain its leadership position in global investment banking, particularly in M&A advisory, equity, and debt underwriting. Throughout 2025, Goldman’s IB division has capitalized on the resurgence in global deal-making, advising on more than $1.6 trillion in announced M&A volumes in 2025.

The company has seen high levels of client engagement across its IB business and expects the activity to accelerate in 2026. With the IB backlog at a four-year high, the company is well-positioned to benefit in the upcoming period.

Under CEO David Solomon, GS has embarked on a deliberate transformation to exit non-core consumer banking and double down on the divisions where Goldman maintains a clear competitive advantage. In sync with its restructuring efforts, in January 2026, Goldman signed an agreement to transition the Apple Card program and associated accounts to JPMorgan. The same month, GS acquired Industry Ventures to expand its exposure to the innovation economy and solidify its position in the global alternatives market. In December 2025, Goldman entered an agreement to acquire Innovator Capital Management. The deal will significantly expand Goldman’s active ETF capabilities and is part of a broader pivot toward building “durable revenue streams” through diversified asset management and wealth-management offerings. In November 2025, Goldman reached an agreement with ING Bank Slaski to divest its Polish asset management firm, TFI. The deal is targeted for completion in the first half of 2026. In the third quarter of 2025, Goldman completed the sale of its GM credit card business to Barclays.

The benefits of business restructuring began to show in the numbers. The Global Banking and Markets segment’s net revenues rose 18% year over year in 2025, whereas the AWM division’s net revenues rose 2%, reflecting growing fee income and strength in private credit. AWM division’s scale continues to expand. Total assets under supervision rose to a record $3.61 trillion in 2025.

Goldman is rolling out a firmwide AI transformation across trading, investment banking, asset management and internal operations to boost fee income and efficiency. Central to this are the OneGS 3.0 initiative and the GS AI Assistant, which embed AI into core workflows. OneGS 3.0 is a multi-year effort to make AI a core capability, focused on simplifying processes, improving productivity and enabling scalable growth through better data, shared platforms and modern infrastructure.

The Case for EVR

Evercore, though small in size, established itself as a significant player in the IB space. The company generates most of its revenues from the Investment Banking and Equities business (which constituted 97% of the total revenues in 2025). After subdued activity in 2022 and 2023, global M&As improved in 2024 and 2025 as both deal value and volume rose.

In 2025, M&A activity opened on an optimistic note, though sentiment briefly cooled, but rebounded as the year progressed. Looking ahead, transaction activity is expected to strengthen, supported by lower borrowing costs and increased focus on scale and AI integration. Investment Banking and Equities business witnessed a compound annual growth rate (CAGR) of 10.7% over the past five years (2020-2025).

Evercore is strengthening its IB business footprint by actively increasing staff. As of Dec. 31, 2025, the company employed more than 200 senior managing directors in the Investment Banking & Equities business. In February 2026, the company acquired U.K.-based independent advisory firm, Robey Warshaw. This will bolster the company’s presence across EMEA and broaden its sector and product coverage.

EVR’s efforts to boost its client base in advisory solutions, diversify revenue sources and expand geographically will likely support IB revenue growth.

A small portion of Evercore’s business is wealth management. Though the division’s profitability has been hurt in recent years due to the disposal and restructuring of several related units, decent inflows, upbeat market performance and higher fees from clients are expected to offer some support.

GS & EVR: Price Performance, Valuation & Other Comparisons

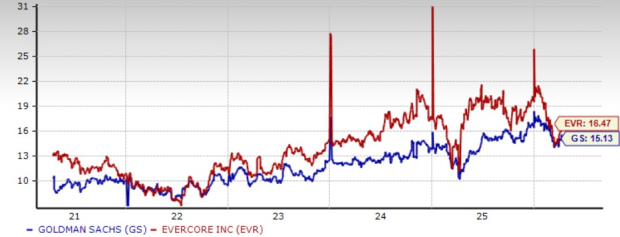

In the past year, shares of Goldman and Evercore have surged 84.9% and 86.4%, respectively, compared with the industry’s growth of 48.1%.

Price Performance

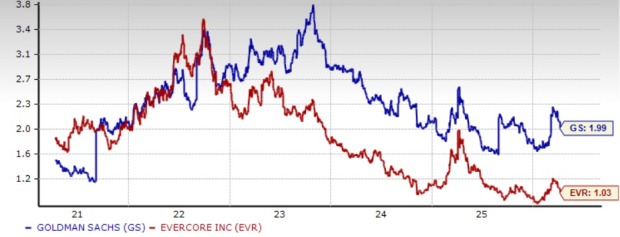

In terms of valuation, Goldman is currently trading at a 12-month forward price-to-earnings (P/E) of 15.1X, higher than its five-year median of 10.8X. The EVR stock, alternatively, is currently trading at a 12-month forward P/E of 16.5X, which is higher than its five-year median of 12.9X. Both stocks are trading at a premium compared with the industry average of 12.8X. However, GS is cheaper than the EVR Stock.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

Both companies regularly pay out dividends. GS has a dividend yield of 1.9%, whereas EVR has a dividend yield of 1%. Here also, Goldman holds an edge over Evercore.

Dividend Yield

Image Source: Zacks Investment Research

How Do Estimates Compare for GS & EVR?

The Zacks Consensus Estimate for GS’s 2026 and 2027 earnings indicates a year-over-year rise of 12.6% and 12.8%, respectively. Earnings estimates for both years have been revised upward over the past 30 days.

Estimate Revision Trend

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for EVR’s 2026 and 2027 earnings suggests a year-over-year jump of 27.2% and 25.5%, respectively. Earnings estimates for both years have been unchanged over the past 30 days.

Estimate Revision Trend

Image Source: Zacks Investment Research

GS or EVR: Which Stock Has More Upside Right Now?

While both Goldman and Evercore are well-positioned to benefit from a continued M&A upcycle, GS offers the more compelling overall risk-reward profile at this stage.

Evercore’s focused advisory model, higher earnings growth outlook and strong positioning in high-margin M&A advisory make it an attractive pure-play on deal activity. However, this strength is already reflected in its relatively higher valuation and greater sensitivity to fluctuations in deal volumes.

Goldman, conversely, combines solid investment banking momentum with increasing diversification across trading, asset management and wealth management. Its ongoing strategic transformation, exiting lower-return businesses and scaling durable, fee-based revenue streams add resilience to earnings. At the same time, initiatives like firmwide AI integration and balance sheet optimization position Goldman for more consistent long-term growth.

Remarkably, Goldman trades at a relative valuation discount to Evercore, offers a higher dividend yield and benefits from multiple growth levers beyond just M&A. This provides a better cushion in case of cyclical volatility while still allowing meaningful upside if deal activity accelerates further.

At present, both Goldman and Evercore carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Goldman Sachs Group, Inc. (GS): Free Stock Analysis Report

Evercore Inc (EVR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).