Steven Madden, Ltd.’s SHOO strong digital momentum and improving full-price channel performance significantly boosted its direct-to-consumer (DTC) business, reinforcing the brand’s ability to drive profitable growth through owned channels. In fourth-quarter 2025, DTC revenues surged 79.9% year over year to $316.6 million. Even after excluding the contribution from the Kurt Geiger acquisition, DTC sales still increased 1.6%, reflecting steady organic momentum.

A key highlight was the return of comps growth in Steve Madden’s U.S. DTC business during the fourth quarter. Management noted that strong performance in full-price channels more than offset continued softness in outlet stores. This signals improving brand desirability and healthier consumer demand, especially in premium and full-price assortments.

The digital channel was particularly strong, with management emphasizing that e-commerce growth outpaced physical stores in the fourth quarter. Online brand searches for Steve Madden increased 10% year over year, showing rising brand heat among Gen Z and millennial consumers. The company’s investments in richer product storytelling and always-on marketing campaigns appear to be translating into stronger online traffic and conversion.

Store productivity also showed encouraging trends. While outlets remained weak, full-price stores posted a solid increase, and performance improved further heading into the first quarter of 2026. The company ended 2025 with 399 company-operated stores, alongside seven e-commerce websites and 133 international concessions, underscoring the scale of its DTC platform.

Looking ahead, management remains optimistic about continued DTC momentum. For 2026, excluding Kurt Geiger, DTC revenues are expected to grow 7.5% at the mid-point. This strength, supported by digital traction, better full-price sell-through and sustained marketing investment, positions DTC as a critical long-term growth engine for Steven Madden’s brand portfolio. We foresee DTC revenues to increase 21.3% year over year in 2026.

SHOO’s Price Performance, Valuation & Estimates

Shares of the company have surged 80.2% in the past year against the industry’s 17.6% decline.

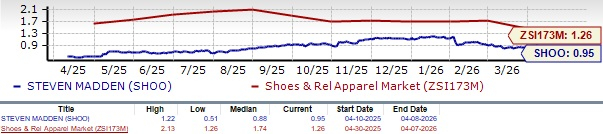

Image Source: Zacks Investment Research

From a valuation standpoint, Steven Madden is trading at a forward 12-month price-to-sales ratio of 0.95X, down from the industry average of 1.26X. It has a Value Score of B.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Steven Madden’s 2026 earnings implies a year-over-year growth of 22.9%, whereas the same for 2027 indicates an uptick of 16.8%. Estimates for 2026 and 2027 have been revised upward by 5 cents and 7 cents, respectively, in the past 30 days.

Image Source: Zacks Investment Research

SHOO’s Zacks Rank & Key Picks

Steven Madden currently has a Zacks Rank #3 (Hold).

Some better-ranked stocks are FIGS Inc. FIGS, Tapestry, Inc. TPR and Abercrombie & Fitch Co. ANF.

FIGS is a direct-to-consumer healthcare apparel and lifestyle brand, and it currently sports a Zacks Rank of 1 (Strong Buy). The company delivered a trailing four-quarter earnings surprise of 187.5%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FIGS’ current financial-year sales and earnings indicates growth of 11.7% and 15.8%, respectively, from the year-ago reported numbers.

Tapestry, which was formerly known as Coach, Inc., is the designer and marketer of fine accessories and gifts for women and men in the United States and internationally. It presently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Tapestry’s current fiscal-year earnings and sales implies growth of 26.5% and 11.2%, respectively, from the year-ago actuals. TPR delivered a trailing four-quarter average earnings surprise of 12.8%.

Abercrombie & Fitch operates as a specialty retailer of premium, high-quality casual apparel for men, women and kids. It currently has a Zacks Rank of 2.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current fiscal year earnings and sales implies growth of 8.6% and 4.3%, respectively, from the year-ago actuals. ANF delivered a trailing four-quarter average earnings surprise of 8.4%.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF): Free Stock Analysis Report

Steven Madden, Ltd. (SHOO): Free Stock Analysis Report

Tapestry, Inc. (TPR): Free Stock Analysis Report

FIGS, Inc. (FIGS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).