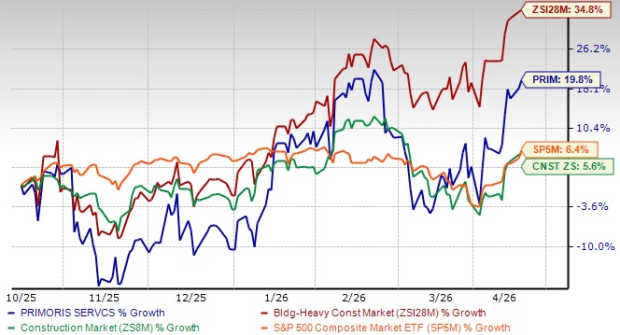

Shares of Primoris Services Corporation PRIM have gained 19.8% in the past six months, underperforming the Zacks Building Products - Heavy Construction industry’s 34.8% growth. However, the stock has outperformed the broader Construction sector and the S&P 500 in the same period, as evidenced by the chart below.

This Texas-based specialty construction and infrastructure company is navigating mixed performance across its end markets. While certain segments are facing margin pressure due to project mix, lower storm activity and execution challenges in select renewable projects, underlying demand trends remain strong. Increasing investments in power generation, grid infrastructure and data center development are supporting long-term opportunities. Strong backlog, improving pipeline visibility and continued growth in utilities, communications and natural gas projects provide a stable foundation for future revenues.

Image Source: Zacks Investment Research

Let us take a closer look at the factors shaping Primoris stock’s prospects.

Strong Backlog Strengthens PRIM’s Growth Visibility

Project awards remained healthy, supporting visibility into future revenues. As of Dec. 31, 2025, total backlog stood at approximately $11.9 billion, slightly higher than $11.86 billion as of Dec. 31, 2024. The utilities backlog was $6.4 billion, while the energy backlog was nearly $5.5 billion, reflecting steady demand across both segments.

In the fourth quarter of 2025, the company secured close to $3 billion of new awards, supporting backlog levels and reinforcing activity across core markets. A greater share of recurring program work improves revenue visibility and supports more consistent execution going forward.

Utilities Segment Activity Remains a Core Contributor

Work across power delivery, communications and gas operations continued to support trends in the Utilities segment for PRIM. MSA backlog increased more than 20% year over year in the fourth quarter of 2025, reflecting stronger contract renewals and higher expected spending from utility customers, particularly in power delivery programs.

The company also benefited from higher volumes in gas-related services, especially in regions with ongoing infrastructure expansion. Communications work continued to gain from investments in connectivity and network infrastructure. This mix of recurring program work and project-based activity provides stability to PRIM’s segment trends and supports consistent revenue contribution.

Energy Segment Opportunities Expand Across Renewables and Gas

A broad mix of projects across renewables, natural gas generation and pipeline construction continues to support activity for the company’s Energy segment. The fourth quarter saw strong project awards, reinforcing demand across key energy markets.

Renewables work remains supported by solar and storage projects, while the company is also seeing growing traction in natural gas generation as a reliable power source amid rising electricity demand. Pipeline construction activity is improving, supported by LNG-related developments. This diversified opportunity set supports PRIM’s growth across multiple energy end markets.

Earnings Estimate Trend of PRIM

Primoris’ 2026 earnings estimate has increased to $6.02 per share from $5.96 over the past 30 days. The estimated figure for 2026 earnings implies a rise of 7.1% year over year on projected revenue growth of 8.8%.

Image Source: Zacks Investment Research

Hurdles to PRIM’s Growth Trend

Despite strong demand across energy and infrastructure markets, execution-related challenges remain a key factor influencing near-term performance. Variability in project mix, along with lower-margin work and reduced storm activity, has created pressure on margins. Gross margin declined to 9.4% in the fourth quarter of 2025 from 10.6% in the prior year, reflecting these headwinds.

Some of these pressures were also linked to project-specific issues, particularly in renewables, where unexpected site conditions led to higher costs. While most of these impacts are expected to normalize, consistent execution and cost control will remain important to support margin recovery going forward.

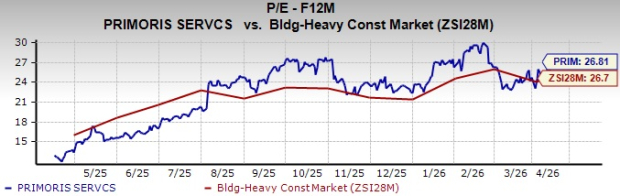

PRIM Trading at Premium

Primoris stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 26.81, as shown in the chart below.

Image Source: Zacks Investment Research

Primoris’ Competitive Landscape

Primoris’ positioning across energy and infrastructure markets reflects broader industry momentum, where peers such as Quanta Services, Inc. PWR, MasTec, Inc. MTZ and EMCOR Group, Inc. EME are also benefiting from rising demand tied to electrification, grid expansion and digital infrastructure. These companies operate across power, engineering and construction services, creating overlap in utilities, energy and mission-critical infrastructure markets.

Quanta remains a leading player in electric power infrastructure, supported by strong utility relationships and a dominant presence in transmission, distribution and renewable integration. Its scale and execution capabilities allow Quanta to secure large, complex projects tied to long-term grid modernization and electrification trends.

MasTec offers a diversified platform across pipelines, clean energy and communications infrastructure. Exposure to both traditional energy and renewables provides flexibility, though performance can vary depending on project mix and execution. Compared with Primoris, MasTec benefits from broader service capabilities and higher exposure to large-scale infrastructure projects.

EMCOR has a strong presence in electrical and mechanical construction, with growing exposure to data centers and other mission-critical facilities. Its focus on services and maintenance work provides recurring revenue streams, while expanding data center demand supports EMCOR’s growth opportunities alongside infrastructure peers.

Within this landscape, Primoris benefits from its balanced exposure to utilities and energy markets, along with growing opportunities in natural gas generation, renewables and pipeline construction. However, compared with larger peers, scale and execution consistency remain key areas to watch as the company continues to expand its positioning.

How to Play Primoris Stock?

Primoris is benefiting from steady demand across utilities, energy and infrastructure markets. A strong backlog, improving pipeline visibility and continued momentum in power delivery, communications and natural gas projects provide support for growth. The company is also seeing favorable estimate revisions for 2026, indicating improving earnings prospects as infrastructure spending remains supportive.

However, margin pressure from project mix and execution challenges may continue to create some near-term variability. In addition, the stock is trading at a premium valuation compared with peers, which could limit immediate upside. With a Zacks Rank #3 (Hold), the stock appears suitable for holding, while new investors may wait for a more attractive entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Primoris Services Corporation (PRIM): Free Stock Analysis Report

MasTec, Inc. (MTZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).