Artificial intelligence (AI) infrastructure spending continues to accelerate as cloud providers, enterprises, and governments invest heavily in the computing capacity required to train and deploy advanced AI systems. This wave of capital expenditure has led to a significant rally in many companies within the AI ecosystem. However, a handful of high-quality AI stocks are still undervalued despite strong growth and their significant role in the AI build-out.

Among the companies that look compelling on the valuation front are Micron (MU) and Nvidia (NVDA). Both firms occupy critical positions within the AI hardware supply chain, yet their valuations still leave room for meaningful upside.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Micron is a key supplier of memory chips, including high-bandwidth memory (HBM), which is increasingly essential for AI accelerators and data center workloads. Nvidia, meanwhile, remains the dominant force in AI computing. Its graphics processing units (GPUs) power the majority of large-scale AI training systems used by technology companies and research organizations worldwide.

Why Buy Micron Stock Now?

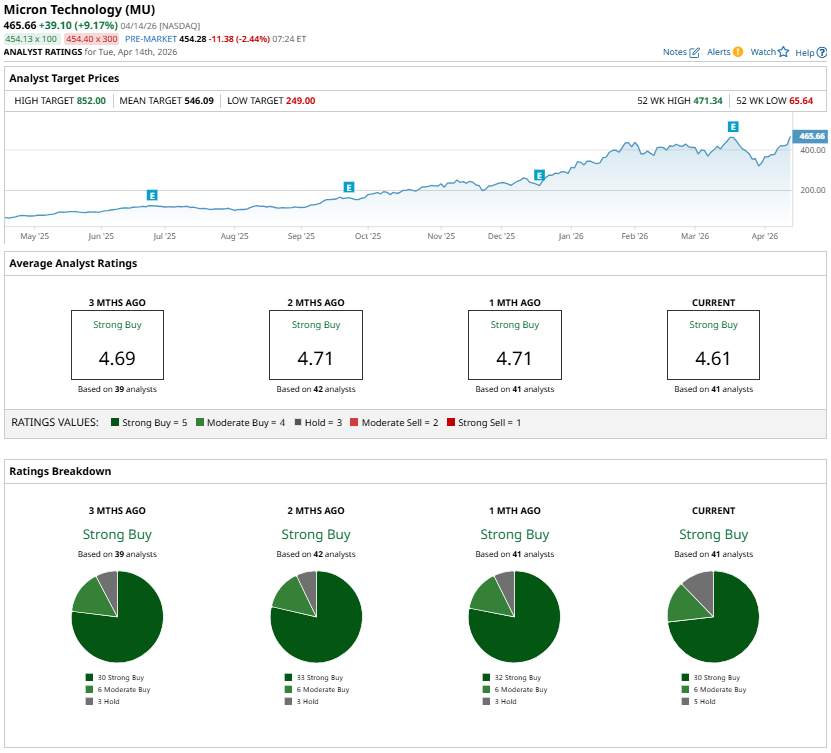

Micron has rallied significantly, with its stock rising more than 55% year-to-date (YTD) and over 525% in the past year. The surge reflects strong demand for the company’s high-performance memory products, driven by AI systems. As AI systems become increasingly memory-intensive, Micron’s advanced DRAM and storage solutions position the company well to capitalize on the growing demand.

The broader industry backdrop has also worked in Micron’s favor. Memory supply remains relatively tight, which has helped push pricing higher across the market. This favorable balance between supply and demand is expected to continue supporting Micron’s margins and earnings, allowing the stock to maintain momentum in the near term.

Demand trends in data centers further support Micron’s growth outlook. Expanding server infrastructure and the rise of AI workloads are increasing the need for specialized memory solutions. Micron has strategically focused on higher-value offerings such as HMB, large-capacity server modules, and data-center solid-state drives, which are expected to support its growth.

Management’s guidance adds further optimism. During the company’s second-quarter conference call, executives indicated that third-quarter revenue could reach approximately $33.5 billion, representing year-over-year (YoY) growth of more than 260%. Profitability is also expected to improve substantially. Gross margins are projected to approach 81%, a sharp increase from the 39% adjusted margin reported in the same period last year. Earnings per share (EPS) are forecasted to rise to $19.15, compared with $1.91 a year earlier.

Despite the strong rally, Micron’s valuation still appears attractive relative to its growth prospects. The stock currently trades at about 7.3 times forward earnings, a modest multiple given the company’s projected EPS expansion. Analyst estimates suggest MU’s earnings could surge by more than 651% in 2026 and grow another 69.4% in fiscal 2027. Reflecting this outlook, analysts broadly maintain a “Strong Buy” consensus rating on the stock.

www.barchart.com

www.barchart.com Nvidia Stock Is Too Cheap to Ignore

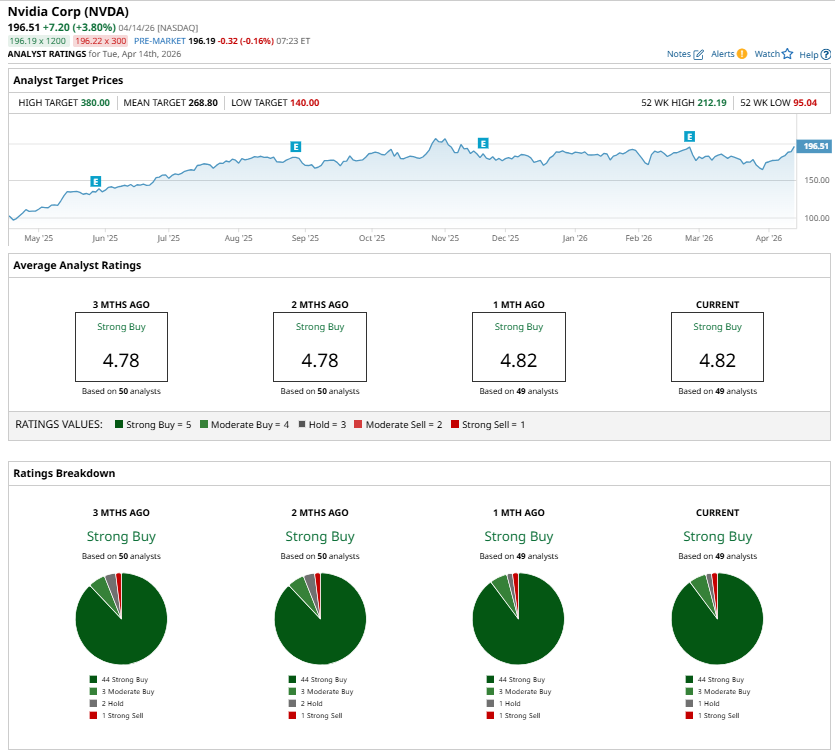

Nvidia continues to benefit from an unprecedented surge in demand for advanced graphics processing units (GPUs), driven largely by significant investment in the build-out of AI infrastructure.

The company has recently raised its demand projections for its next-generation chip architectures, Blackwell and Rubin. Previously, Nvidia estimated the cumulative GPU demand of $500 billion linked to these platforms. That figure has now doubled, with management expecting demand and purchase commitments to exceed $1 trillion by 2027. Such projections reflect the scale of capital flowing into AI infrastructure and suggest a multi-year growth runway for the company.

Nvidia’s operational performance remains solid. The company’s data center segment, the primary driver of its AI business, generated $194 billion in fiscal 2026 revenue, representing a 68% YoY increase. Management expects this growth trajectory to continue, projecting sequential revenue gains throughout calendar year 2026. Importantly, the company has secured inventory and supply commitments that provide shipment visibility well into 2027, reducing execution risk amid rising demand.

Despite its solid growth prospects, NVDA stock trades cheap. The stock trades at 24.4 times forward earnings, which appears compelling relative to its earnings growth potential. Analysts expect Nvidia’s earnings growth of more than 69% in fiscal 2027, followed by continued double-digit gains in fiscal 2028.

Overall, Nvidia’s strong demand outlook, expanding revenue base, and comparatively reasonable valuation strengthen its long-term investment thesis. Analysts remain bullish and maintain a “Strong Buy” consensus rating.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

2 Undervalued AI Stocks That Could Skyrocket Soon Bull Call Spread Screener Results For April 16th Nasdaq Futures Climb as TSMC Boosts Tech Optimism This Dividend Stock Is Becoming Too Cheap to Ignore: Should You Buy?