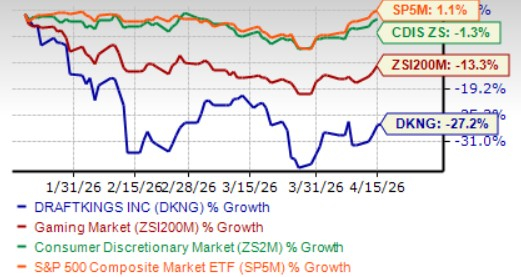

Shares of DraftKings Inc. DKNG have lost 27.2% in the past three months, sharply underperforming the Zacks Gaming industry’s decline of 13.3%. The stock has also underperformed the broader Zacks Consumer Discretionary sector and the S&P 500 in the same period, as evidenced by the chart below.

DKNG’s Past 3 Months’ Price Performance

Image Source: Zacks Investment Research

Investor sentiment has weakened amid rising investment intensity and signs of moderation in key operating metrics. DraftKings is stepping up spending on its Predictions platform, with tens of millions in incremental costs, creating a near-term margin overhang. At the same time, Sportsbook handle growth has slowed, and user trends reflect a normalization in customer acquisition. This combination of higher spending and cooling operating momentum has likely weighed on the stock.

With DKNG stock under pressure, investors face a key question: Is this a buying opportunity or a sign of deeper fundamental challenges? Let’s take a closer look.

Heavy Investments Likely to Pressure DKNG’s Margins

A major near-term headwind for DraftKings is its aggressive push into the Predictions business. The company is expanding capabilities across product development, exchange integration and market-making while increasing spending on customer acquisition and marketing.

Management indicated that this initiative will involve tens of millions in incremental costs, with no revenue contribution assumed at this stage. As a result, expenses are being incurred ahead of monetization, limiting near-term margin visibility.

DraftKings also retains the flexibility to scale marketing spend based on customer response, indicating that investment levels could remain elevated as it builds out the platform.

DKNG’s Handle Growth Dynamics Reflect Operating Trade-Offs

DraftKings’ recent performance highlights the interaction between profitability and betting volumes. Net revenue margins expanded from roughly 6.5% earlier in 2025 to over 9% in recent months, driven by improved hold rates and efficient promotional spend.

However, this improvement has coincided with a moderation in handle growth, with January handle increasing just 4% year over year. Management noted that higher hold and reduced promotional intensity can influence betting activity, as these factors tend to move together.

This dynamic introduces variability in key operating metrics and makes growth trends less straightforward to interpret.

DKNG’s Customer Growth Normalizes After Strong 2024

Customer acquisition trends have moderated following elevated levels in 2024. Management noted that acquisition in 2025 declined from prior peaks and aligned more closely with expected levels, contributing to flat year-over-year trends in monthly unique players.

The company also cited factors such as Jackpocket as contributing to this trend. While retention remains strong, new customer additions have slowed compared to earlier periods.

Conservative Outlook Weighs on DKNG’s Prospects

DraftKings has adopted a more measured approach to its forward outlook following prior guidance misses. Management emphasized setting expectations at levels it is confident in achieving, reflecting a reset in forecasting discipline.

For 2026, DraftKings expects revenues between $6.5 billion and $6.9 billion and adjusted EBITDA of $700 million to $900 million. Notably, the outlook excludes any contribution from the Predictions business while incorporating associated investment costs, highlighting a cautious stance on near-term monetization.

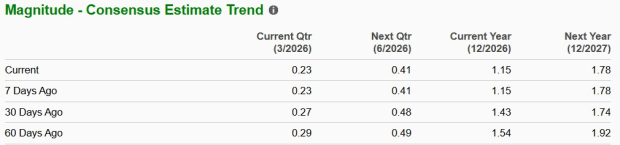

The Zacks Consensus Estimate for DKNG’s fiscal 2026 earnings per share has declined 25.3% over the past 60 days, reflecting weakening analyst confidence.

DKNG’s Earnings Estimate Trend

Image Source: Zacks Investment Research

Among other industry players, Accel Entertainment, Inc. ACEL has experienced a 9.5% upward revision in its earnings estimates over the past 60 days, whereas estimates for Boyd Gaming Corporation BYD and Bally’s Corporation BALY have declined by 0.1% and 107.3%, respectively.

Valuation Insights for DKNG Stock

DKNG stock is currently trading at a discount. It is currently trading at a forward 12-month price-to-sales (P/S) multiple of 1.66, below the industry average of 2.16. Conversely, industry players, such as Accel Entertainment, Bally's and Boyd Gaming, have P/S ratios of 0.69, 0.17, and 1.56, respectively.

DKNG’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

How to Play DraftKings Stock?

While DraftKings’ recent sell-off reflects rising concerns around moderating operating momentum and increased investment intensity, the broader fundamental picture remains mixed. Elevated spending on the Predictions platform, the absence of near-term revenue contribution from this initiative and a normalization in customer acquisition trends continue to weigh on margin visibility. At the same time, variability in handle growth alongside improving hold rates highlights shifting operating dynamics.

Although DKNG trades at a discount to the industry on a P/S basis, the valuation does not adequately compensate for execution risks, sustained investment pressure and continued downward revisions in earnings estimates. With growth visibility weakening and margin trends becoming increasingly unpredictable, the risk-reward profile appears unfavorable. Considering its current Zacks Rank #5 (Strong Sell), it may be prudent for investors to avoid the stock for now.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boyd Gaming Corporation (BYD): Free Stock Analysis Report

Accel Entertainment, Inc. (ACEL): Free Stock Analysis Report

DraftKings Inc. (DKNG): Free Stock Analysis Report

Bally's Corporation (BALY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).