Resmed Inc. RMD is well poised to grow in the coming quarters, driven by its sharpened focus on growing its core sleep apnea franchise, expanding into other adjacencies and investing in the digital health ecosystem. Ongoing supply of both AirSense 10 and AirSense 11 sleep devices is driving strong underlying demand trends worldwide. Solid financial health also adds to the stock’s appeal. Meanwhile, the company’s exposure to macroeconomic pressures and strong competitive dynamics poses risks to its operations.

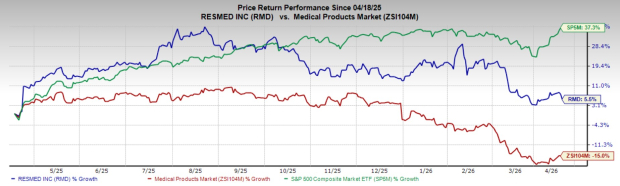

In the past year, this Zacks Rank #3 (Hold) stock has risen 5.5% against the 15% decline of the industry and the S&P 500 Composite’s 37.3% growth.

The renowned medical device company has a market capitalization of $33.33 billion. RMD has an earnings yield of 4.8% compared with the industry’s yield of 2.4%. The company’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 2.74%.

Let’s delve deeper.

Upsides for RMD Stock

Growth Strategy Impressive: Resmed’s execution against its three core pillars — growing its core sleep health and breathing health business, expanding into adjacent areas, and investing in a fully integrated, home-based digital health ecosystem — underpins its updated financial outlook through 2025-2030. In the second quarter of fiscal 2026, Resmed's pipeline of margin improvement initiatives drove 310 basis points of year-over-year gross margin expansion. The company continues to make progress on its newest U.S. distribution center in Indiana, which is expected to enable shipment to roughly 90% of U.S. customers in less than two business days.

Further, patient and provider feedback for its new F30i Comfort and the F30i Clear range of masks has been remarkably positive. Resmed rolled out Comfort Match, an AI-enabled comfort setting technology that sits on the myAir platform, via a limited beta program in Australia. On the inorganic growth strategy front, the company continues to pursue tuck-in size acquisitions, such as Somnoware, a software for sleep physicians and pulmonary physicians and Ectosense, the developer of the NightOwl wearable, a fingertip-sized sleep home sleep apnea test, and VirtuOx.

Image Source: Zacks Investment Research

Recovery in Device Sales: Resmed’s increased device sales continue to drive overall revenue growth, reflecting the ongoing combined availability of AirSense 10 and AirSense 11 sleep devices to support strong underlying global demand. Global device constant-currency sales increased 7% in the second quarter of fiscal 2026, including 8% growth across the United States, Canada and Latin America and an increase of 5% in combined Europe, Asia and other markets. The company continues to increase the availability of the AirSense 11 platform to more countries by securing market-by-market regulatory clearances. Resmed launched Airsense11 in India in calendar year 2025. Additionally, it introduced the AirSense 11version of VPAP Tx, a sleep lab testing and titration platform built specifically for both hospital and outpatient sleep lab environments.

Favorable Solvency: Resmed exited the second quarter of fiscal 2026 with cash and cash equivalents of $1.42 billion and $260 million in current debt. Long-term debt dropped 1.2% sequentially to $404 million. The company’s debt-to-capital ratio was 6% at the end of the fiscal second quarter, down 0.3% on a sequential basis.

What Ails Resmed?

Challenging Macroeconomic Scenario: Resmed’s operations remain exposed to global macroeconomic conditions, geopolitical instability, the impact of tariffs and trade wars on its suppliers and other factors. These factors could dampen product demand and pricing, reduce reimbursement rates from third-party payers and drive higher operating costs. Meanwhile, global supply chain disruptions, leading to limited availability and higher costs of raw materials and electronic components, could continue to hamper the company’s financials. Persistent inflationary pressures also pose a headwind to Resmed’s future profitability.

Competitive Landscape: The SDB product market remains highly competitive with respect to product price, features and reliability. Resmed's primary competitors include Philips BV, DeVilbiss Healthcare, Fisher & Paykel Healthcare Corporation Limited, Apex Medical Corporation, BMC Medical Co. Ltd. and regional manufacturers. Competitive pressures may intensify as healthcare industry consolidation widens the resource gap. Moreover, some of Resmed's competitors, such as Löwenstein Medical GmbH + Co. KG, are affiliates of its customers, which may make it difficult for the company to compete with them.

RMD Stock’s Estimate Trend

The Zacks Consensus Estimate for RMD’s fiscal 2026 earnings per share (EPS) has remained constant at $11.04 in the past 30 days.

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $5.63 billion, up 9.4% from the year-ago reported figure.

Key Picks

Some better-ranked stocks in the broader medical space are Globus Medical GMED, BrightSpring Health Services BTSG and Cardinal Health CAH.

Globus Medical has an earnings yield of 4.9%, well ahead of the industry’s negative 2.2% yield. Its earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed on one occasion, the average surprise being 18.8%. The company’s shares have rallied 30.7% compared with the industry’s 7% growth in the past year.

GMED sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

BrightSpring Health Services, sporting a Zacks Rank #1 at present, has an estimated long-term earnings growth rate of 47.2% compared with the industry’s 14.5% growth. Shares of the company have surged 176% compared with the industry’s 1.8% growth in the past year. BTSG’s earnings beat estimates in three of the trailing four quarters and missed on one occasion, with the average surprise being 40.4%.

Cardinal Health, carrying a Zacks Rank #2 (Buy), has an earnings yield of 4.8% compared with the industry’s 6.5% yield. Shares of the company have rallied 58.5% compared with the industry’s 12.7% growth. CAH’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 9.3%.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

ResMed Inc. (RMD): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

BrightSpring Health Services, Inc. (BTSG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).