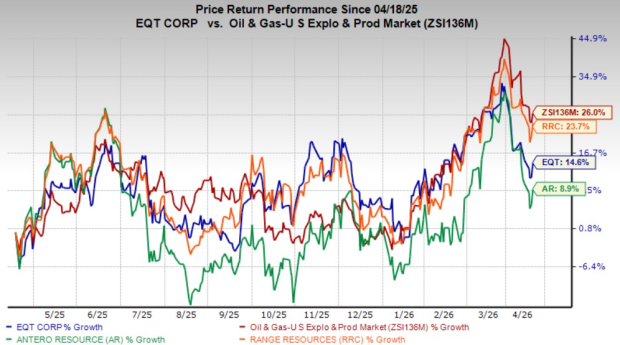

EQT Corporation EQT shares have gained 14.6% compared with the industry’s 26% growth over the past year. Shares of its peers, Antero Resources Corporation AR and Range Resources Corporation RRC, have returned 8.9% and 23.7%, respectively, over the same time frame. EQT is primarily involved in the exploration and production of natural gas in the prolific Appalachian Basin in the United States. The company is involved in gathering and transmission operations within the basin, along with the marketing of natural gas.

The company’s strong fundamentals and vertically integrated business model make EQT a favorable choice in the energy sector. Before offering any investment advice, it would be wise to closely examine the company’s current business environment.

EQT’s Vertically Integrated Business Model

EQT has an extensive inventory of core drilling locations within the highly productive Appalachian Basin in the United States. The company is a large-scale natural gas producer in the Appalachian Basin, with a vast midstream infrastructure. This positions EQT to meet the growing demand for the commodity from various sources, including domestic data center development, power consumption and liquefied natural gas (LNG) exports. The integrated nature of its business adds resilience across various commodity pricing cycles.

When commodity prices are low, the company’s midstream business provides stable and predictable revenues that support its free cash flows. During periods of favorable commodity prices, its low-cost production profile enables the company to lower financial hedging. This provides increased exposure to higher commodity prices, thereby supporting higher revenues and cash flows. The vertical integration of its upstream and midstream operations provides EQT with greater control over the entire value chain and the flexibility to move its natural gas production to high-demand markets.

Structural Rise in Natural Gas Demand

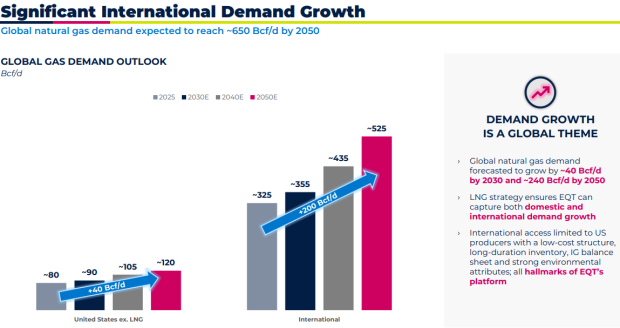

EQT is well-positioned to cater to the structural growth in natural gas demand. This growth is driven by the rapid development of natural gas-fired power plants, the rise in data centers and the use of artificial intelligence, as well as the increase in LNG exports. The company had previously forecasted that global natural gas demand is expected to grow to approximately 40 billion cubic feet per day (Bcf/d) by 2030 and nearly 240 Bcf/d by 2050. These trends provide EQT with an attractive opportunity to expand production and capture growing demand across domestic and international markets over the long term.

The growth of artificial intelligence and cloud computing infrastructure presents a compelling growth opportunity for EQT. With 45 gigawatts (GW) of data center capacity under construction in the United States, nearly 12 GW of capacity lies within its core operating footprint. EQT highlights that the location of these data centers and its high-quality resource base will enable it to capture a significant part of this incremental power demand. Thus, EQT is well-positioned to benefit from the rise in natural gas demand from power generation, growing LNG exports and the expansion of data centers in the United States.

Valuation Snapshot

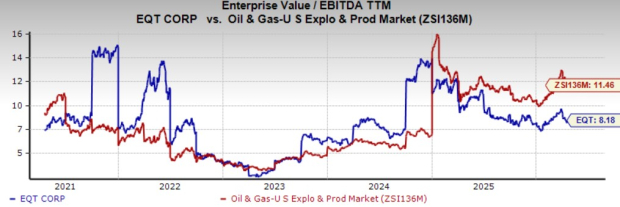

Coming to the valuation story, EQT is currently considered cheap on a relative basis. The stock is trading at an 8.18x trailing 12-month Enterprise Value to Earnings Before Interest, Taxes, Depreciation and Amortization (EV/EBITDA), which is a discount compared with the broader industry average of 11.46x. Its peers, AR and RRC, are currently trading at 8.84x and 8.21x trailing 12-month EV/EBITDA, respectively.

Image Source: Zacks Investment Research

Time to Invest in the Stock or Wait?

EQT is well-positioned to benefit from the structural growth in natural gas demand from domestic data center development, power consumption and LNG exports. Its vertically integrated business model provides resilience across various commodity pricing environments and greater control over the natural gas value chain. The rise in LNG exports and expansion of data centers offer future expansion opportunities and a long runway of growth for EQT.

Despite all the positives, investors should not rush to bet on the stock, given its exposure to commodity price volatility and lack of geographical diversity, stemming from its status as a pure-play Appalachian producer. As such, investors who have already invested can retain the stock, which currently carries a Zacks Rank #3 (Hold). AR and RRC each carry a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Range Resources Corporation (RRC): Free Stock Analysis Report

EQT Corporation (EQT): Free Stock Analysis Report

Antero Resources Corporation (AR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).