Enbridge Inc. ENB is a leading North American midstream energy company with an extensive crude oil, liquids and gas transportation pipeline network. The midstream company’s business is highly stable, owing to its contractual nature. A significant portion of EBITDA is underpinned by long-term “take-or-pay” contracts, which protect it from commodity price swings.

The company has highlighted that, due to the stability of its business model, it can generate predictable cash flows. The reliability of these cash flows allows ENB to operate on an equity self-funding model. This implies that it can utilize its internal cash flows to fund its growth capital, supported by the regulated and stable nature of its business. A major part of Enbridge’s “take-or-pay” contracts is with investment-grade customers, which further reduces risks and variability in earnings.

ENB has stated that a major priority for the company is returning capital to its shareholders through dividends. The midstream company intends to pay out $40-$45 billion in distributions to shareholders over the next five years. Its predictable cash flows, backed by long-term agreements, enable it to return capital to shareholders sustainably. Enbridge’s stable business model, backed by “take-or-pay” contracts and a capital allocation strategy, enables it to invest in growth while returning capital to shareholders in a sustainable manner.

KMI & WMB Have Stable Business Models

Kinder Morgan Inc. KMI is a leading midstream energy company that operates one of the largest natural-gas pipeline system in the United States. It has about 78,000 miles of pipelines, 136 terminals and more than 700 bcf of gas storage. KMI carries a Zacks Rank #2 (Buy).

The Williams Companies, Inc. WMB is another leading player in the midstream energy sector, which operates a widespread pipeline system of more than 32,000 miles, including the Transco and Northwest Pipeline systems. These pipeline systems are among the largest natural gas transportation networks in the United States and are anticipated to benefit from the rising natural gas demand. WMB carries a Zacks Rank #3 (Hold).

Both companies generate stable fee-based earnings, resulting in stable cash flows.

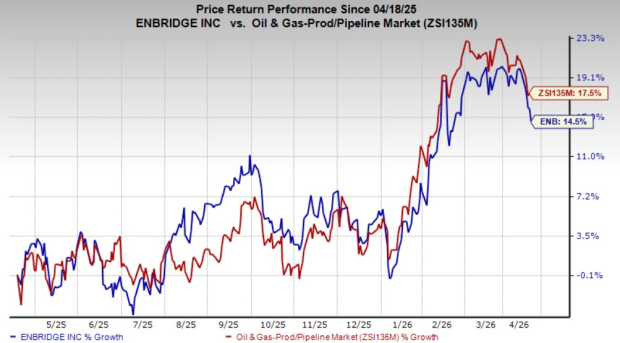

ENB’s Price Performance, Valuation & Estimates

Shares of ENB have jumped 14.5% over the past year compared with the 17.5% improvement of the composite stocks belonging to the industry.

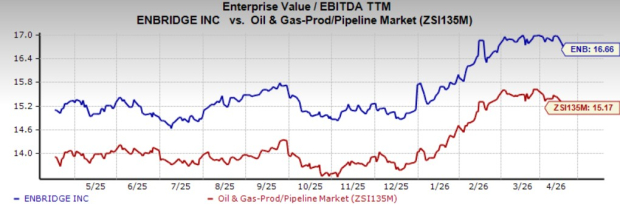

From a valuation standpoint, ENB trades at a trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 16.66X. This is above the broader industry average of 15.17X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for ENB’s 2026 earnings has seen downward revisions over the past seven days.

Image Source: Zacks Investment Research

ENB currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Williams Companies, Inc. (The) (WMB): Free Stock Analysis Report

Enbridge Inc (ENB): Free Stock Analysis Report

Kinder Morgan, Inc. (KMI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).