The artificial intelligence (AI) boom has created massive winners across the market, but it has also added some risks. Massive AI spending, sky-high valuations, and insufficient earnings growth have made investors more skeptical about pure-play AI bets. Accordingly, companies that combine AI exposure with strong fundamentals, predictable revenue, and disciplined execution are becoming increasingly attractive.

Oracle (ORCL) might be one of those rare opportunities that offers a compelling, risk-adjusted way to play the AI trend. ORCL stock is down 11% year-to-date (YTD) and down 49% from its 52-week high of $345.72, compared to the S&P 500 Index's ($SPX) gain of 4% YTD.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Here are three reasons to buy Oracle stock on the dip now before it soars by 128% to reach $400.

www.barchart.com

www.barchart.com Reason #1: Oracle's $553 Billion Backlog Locks in Future Growth

One of the most striking numbers in Oracle’s third-quarter fiscal 2026 earnings report was the company's massive $553 billion backlog. This represents contracted future revenue that has yet to be recognized. While many AI companies are still struggling to secure deals, Oracle has already secured a pipeline that will last for years. What makes this backlog particularly appealing is its link to AI infrastructure demands. The company stated that demand for GPU and CPU capacity continues to outpace supply, which is directly reflected in its enormous remaining performance obligations (RPO).

For investors, this backlog is a positive sign of stability. Even if future AI demand becomes unstable, Oracle's contracted revenue base provides a consistent stream of growth. Oracle's switch to a recurring model has resulted in more predictable and less cyclical revenue than traditional license-based businesses. In Q3 fiscal 2026, total revenue rose 22% year-over-year (YOY) to $17.2 billion. Analysts expect full-year revenue to rise 17% to $67.1 billion in fiscal 2026, followed by 31% growth to $88.2 billion in fiscal 2027.

Reason #2: Scaling AI Without Burning Capital

This year, investors are increasingly scrutinizing AI stocks for their cash burn and return on investment. But Oracle is showing that it can grow its AI business without sacrificing financial discipline. Unlike many of its peers pouring tens of billions of dollars into data centers and chips, Oracle has developed a model that allows it to scale AI infrastructure aggressively without straining its balance sheet.

While the company has a comparatively high debt-to-equity ratio of about 3.19, its interest coverage ratio is 4.96. This means that its operating income covers its interest expenses nearly five times more. No doubt, the company is using leverage to fuel growth, but it is also doing it with sufficient earnings power to manage that debt. In the third quarter, adjusted earnings increased 21% to $1.79 per share. Analysts expect earnings to increase by 23% for fiscal 2026, followed by another 7% in fiscal 2027.

At the same time, Oracle has secured more than 10 gigawatts of power capacity through partners, with over 90% of that capacity already funded externally. Furthermore, it is employing new business formats, such as upfront client payments and "bring your own hardware" agreements. This initiative has already resulted in over $29 billion in new contracts. With a 60% reduction in the time from rack delivery to revenue, the company is not only growing effectively but also monetizing more quickly.

Simply put, Oracle has struck a unique mix between growth, discipline, and increased returns in a capital-intensive AI market.

Reason #3: Turning AI Into an Ecosystem Advantage

Oracle is integrating AI throughout its whole ecosystem. It has already integrated over 1,000 AI agents directly into its applications, enabling automation in sales, finance, healthcare, and supply-chain management. Furthermore, incorporating these agents within the platform rather than selling them as separate add-ons has helped boost value and customer stickiness. Additionally, Oracle is making its database services available on platforms such as Microsoft's (MSFT) Azure, Alphabet's (GOOGL) Google Cloud, and Amazon's (AMZN) Amazon Web Services (AWS). By doing so, it taps into a vast installed base of cloud customers that want to use its technology in a variety of situations. This has already resulted in extraordinary growth, with multi-cloud database revenue up 531% YOY in the third quarter.

Oracle is building the infrastructure and applications that allow entire industries to automate and scale. Its full-stack approach gives it a resilience that many single-focus AI companies lack.

Wall Street Is Bullish About ORCL Stock

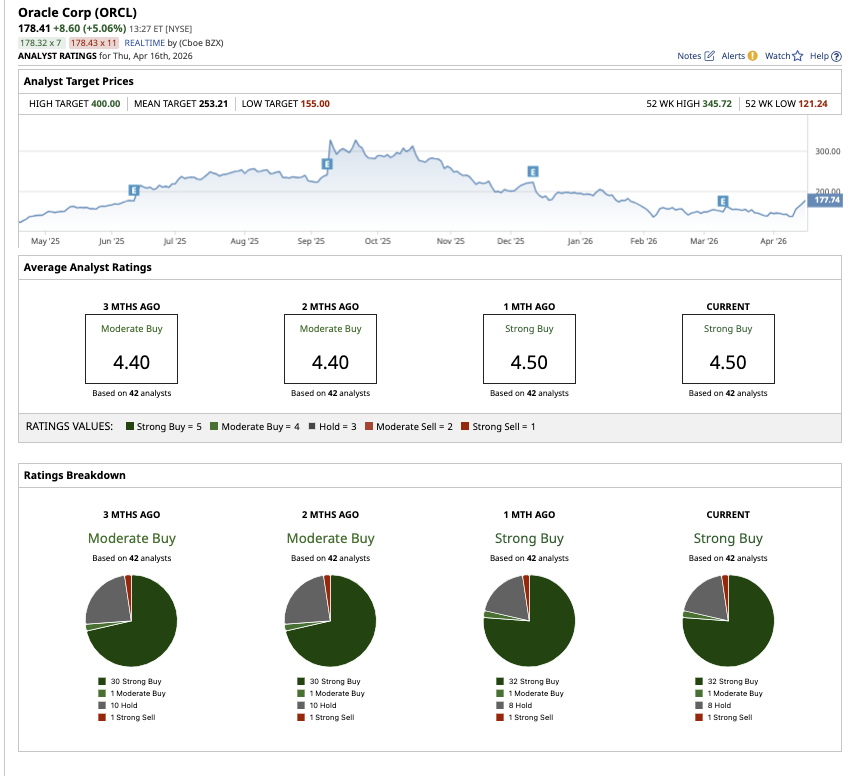

Overall, Wall Street has a consensus “Strong Buy” rating for Oracle stock. Out of the 42 analysts covering ORCL stock, 32 analysts have a “Strong Buy,” one has a “Moderate Buy,” eight have a “Hold” rating, and one analyst has a “Strong Sell" rating. The average target price is $253.21, representing potential upside of 44% from current levels. ORCL stock also has a high price estimate of $400, which suggests potential upside of 128% over the next 12 months.

Oracle still offers a compelling entry point as the AI trade matures. A move to $400 within 12 months would require continued execution and robust AI demand. However, a rally toward the average target price appears achievable, making the stock an attractive buy at current levels.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Many (or Most) of Your Stock Picks Have Not Been Successful Beyond Meat Just Launched a New Beverage Line. Should You Buy BYND Stock Here? 3 Reasons to Buy Oracle Stock as the AI Trade Gets Riskier Pershing Square USA IPO: What Is the PSUS Stock IPO Price Range and IPO Date? And Should You Buy Shares?