Global investment bank J.P. Morgan has stepped up and made its stance clear, signaling that Seagate Technology Holdings plc (STX), the mass capacity storage leader, may still have more upside in store as rising data center demand keeps the growth engine running strong.

The firm has placed Seagate on its Positive Catalyst Watch, reinforcing its confidence in the company’s path ahead. Samik Chatterjee and his team see Seagate holding a clear edge in the hard disk drive (HDD) space, where firm data center demand and supportive pricing trends continue to build momentum.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

The company has kept its foot on the gas with technology transition and has already begun shipping next-generation Heat Assisted Magnetic Recording (HAMR)-based solutions to data center customers, keeping ahead of the curve. Also, Chatterjee noted that near- and medium-term fundamentals have tightened up, as the industry has shown discipline in adding capacity and has leaned into profitable growth.

At the same time, he flagged a key risk that could cloud the picture. A slowdown in cloud capex spending on artificial intelligence (AI) infrastructure could weigh on demand growth forecasts for the HDD industry, even with a solid pipeline of investment announcements already in place.

Still, J.P. Morgan’s call to place Seagate on its Positive Catalyst Watch highlights the company’s strong strategic footing. As data center demand keeps climbing and storage needs expand, Seagate’s push into HAMR technology strengthens its growth case, leaving investors to weigh whether STX stock still has room to run.

About Seagate Stock

Singapore-based Seagate builds the backbone of the digital world and delivers data storage technologies and infrastructure solutions. With a market cap of about $116 billion, the company packs a serious punch, rolling out hard drives, solid state drives, and storage systems that cater to enterprise, personal, and gaming needs.

Over the past 52 weeks, Seagate’s shares have soared 623.9%, and this year has kept the ball rolling with a 99% gain year-to-date (YTD). The last month alone delivered a brisk 30.28% jump, and the past five trading sessions chipped in another 9%, keeping the momentum alive and kicking.

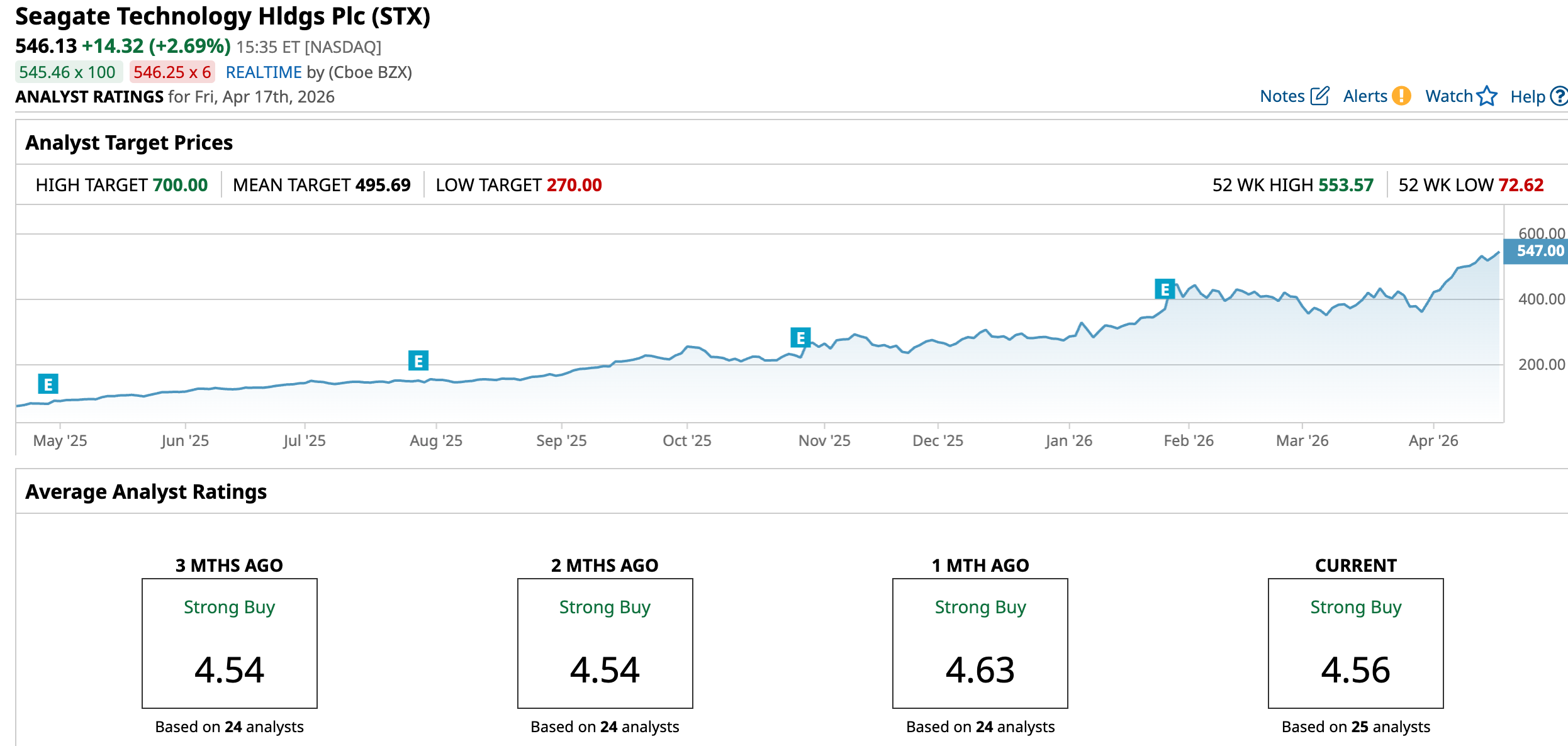

In fact, the stock hit a fresh 52-week high of $534.23 on April 14, right when the company revealed the date for its latest earnings release.

www.barchart.com

www.barchart.com STX stock does not come cheap. The stock is currently trading at 42.90 times forward adjusted earnings and 10.33 times sales, which places it comfortably ahead of industry benchmarks and shows investors have been willing to pay up for a seat at the table.

At the same time, it still keeps shareholders in the loop with a steady payout. The company dishes out an annual dividend of $2.96 per share, which works out to a yield of 0.57%. It paid its latest dividend of $0.74 on Apr. 8 to shareholders who were on record as of March 25.

Seagate Surpasses Q2 Earnings

On Jan. 28, Seagate’s shares jumped 19.1% after the company rolled out its Q2 fiscal 2026 numbers that beat expectations on both the top and bottom line. Revenue climbed 21.5% year-over-year (YOY) to $2.83 billion and cleared the $2.75 billion analyst estimate. Adjusted EPS rose 53.2% from last year’s quarter to $3.11 and topped the $2.84 forecast.

The company shipped 190 exabytes in the quarter, marking a 26% YOY rise, while it kept overall unit capacity on an even keel. The data center market pulled most of the weight and accounted for 87% of shipment volume, as steady demand from global cloud customers and sequential growth across the enterprise OEM market kept the engine humming.

Non-GAAP income from operations reached $901 million and surged 67.5% YOY, while non-GAAP net income rose 62.1% to $702 million. Capital expenditures came in at $116 million, roughly 4% of revenue, while the company held its full-year fiscal 2026 outlook steady at 4% to 6%.

Free cash flow shot up 304.7% from the prior year period to $607 million, marking its highest level in eight years. Plus, cash reserves moved past $1 billion, supported by total liquidity of $2.3 billion, which gives the company enough breathing room to play offense without losing its footing.

Looking ahead, the company guided for fiscal Q3 2026 revenue of $2.9 billion, give or take $100 million, and non-GAAP diluted EPS of $3.40, with a margin of $0.20 on either side. Seagate plans to report its third quarter fiscal 2026 earnings after the closing bell on Tuesday, Apr. 28, which puts the next checkpoint right around the corner.

Nevertheless, analysts expect Q3 fiscal 2026 EPS to climb 94.6% YOY to $3.25. For the full fiscal 2026 year, they see earnings rising 66.8% to $12.11, and they expect another 57.1% jump to $19.03 in fiscal year 2027.

What Do Analysts Expect for Seagate Stock?

Erik Woodring at Morgan Stanley joined the chorus, lifting his price target from $468 to $582 while standing firm on an “Overweight” stance. Citigroup analyst Asiya Merchant has kept her “Buy” rating intact and cranked STX’s price target up from $480 to $595.

Meanwhile, Samik Chatterjee at J.P. Morgan has pushed the price target on STX stock to $600 from $525, and he held on to his “Overweight” call.

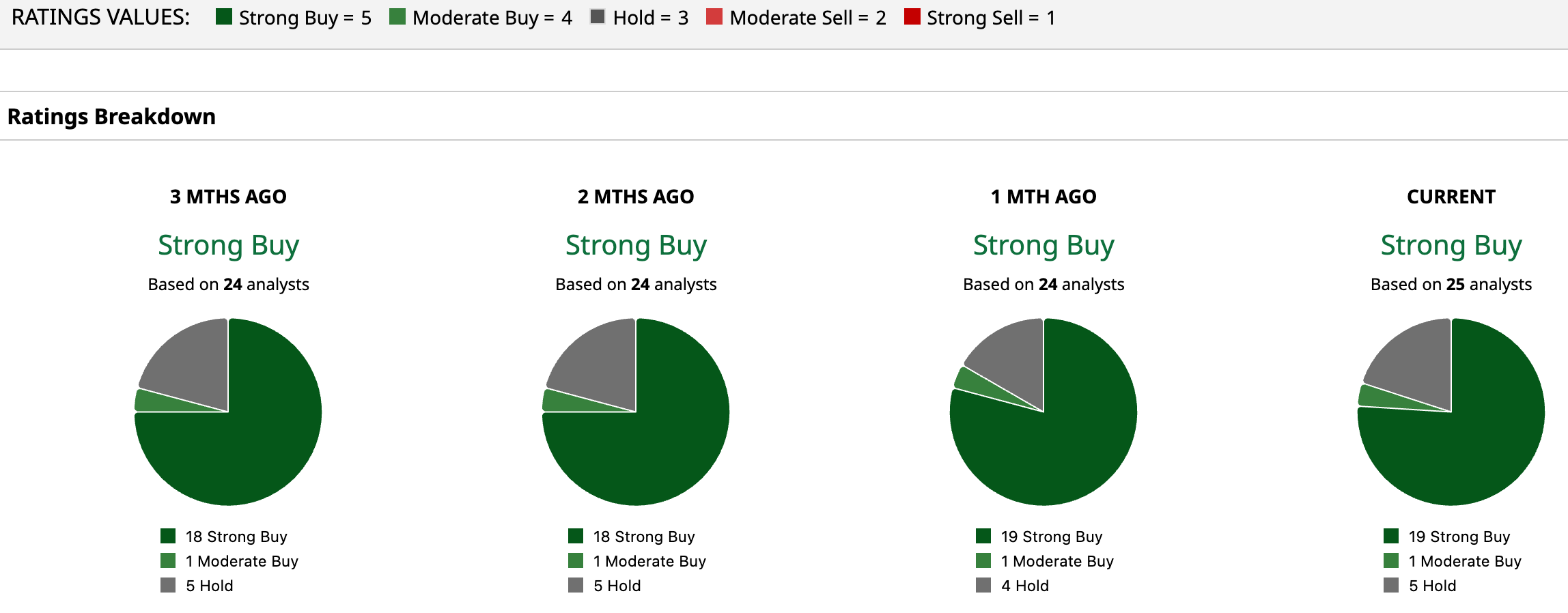

Wall Street has already made up its mind and thrown its weight behind the stock, planting it firmly in “Strong Buy” territory. Among 25 analysts covering the stock, 19 have gone all in with “Strong Buy” calls, one has taken a slightly measured path with a “Moderate Buy,” and five have chosen to hold their ground with “Hold” ratings.

The stock has already sprinted past its average price target of $495.69. Whereas the Street-High target of $700 dangles potential upside of 28.2% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

JPMorgan Says Data Center Demand Will Lift Seagate Stock Even Higher. Should You Buy STX Now? Only 3 Dividend Kings Passed This Brutal Screen. They Could Pay You Well for Years to Come. 3 Dividend Stocks Yielding Over 7% to Buy Now as Iran Ceasefire Talks Collapse As Amazon Pours Another $25B into Data Centers, Buy This 1 High-Yield Data Center Dividend Stock