Omnicom Group Inc. OMC presents a balanced investment case, supported by diversified capabilities, strategic investments and consistent shareholder returns. However, competitive pressures, integration risks and liquidity concerns suggest that investors may prefer a “wait-and-see” stance.

Diversified Offerings Drive OMC’s Stability and Growth

Omnicom’s biggest strength lies in its wide-ranging presence across the advertising and marketing ecosystem. The company operates across traditional advertising, digital marketing, public relations, brand consulting and precision marketing, enabling it to cater to a broad spectrum of clients, from legacy enterprises to new-age digital businesses.

This diversification reduces dependency on any single revenue stream and enhances resilience during industry shifts. By focusing on consumer-centric strategic solutions, Omnicom aligns closely with evolving client needs, fostering long-term partnerships and repeat business.

The benefits of this approach are already visible. Strong demand across segments is expected to support revenue growth, with the Advertising & Media segment projected to post robust year-over-year expansion. Combined with its global scale and deep client relationships, Omnicom appears well-positioned to deliver stable and gradually expanding revenues over time.

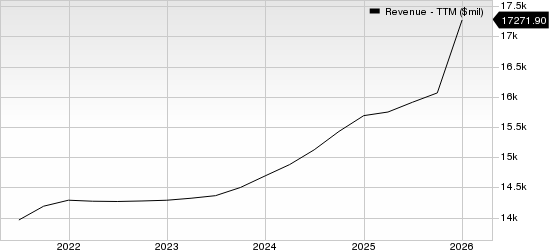

Omnicom Group Inc. Revenue (TTM)

Omnicom Group Inc. revenue-ttm | Omnicom Group Inc. Quote

Strategic Investments Enhancing Efficiency

Omnicom has made targeted investments in areas such as real estate optimization, back-office services, procurement, IT infrastructure, data analytics and precision marketing. These initiatives are not just incremental improvements; they are designed to reshape operational efficiency.

By streamlining internal processes and optimizing costs, Omnicom can allocate more resources toward innovation and client delivery. Enhanced analytics and precision marketing capabilities also strengthen its competitive positioning in an increasingly data-driven industry.

These efficiency gains have the potential to expand margins over time, even as the company continues to invest in growth initiatives. In a sector where adaptability is critical, Omnicom’s forward-looking investments provide a solid foundation for long-term profitability.

Interpublic Acquisition: A Strategic Game Changer

The acquisition of Interpublic Group represents a transformative move for Omnicom. The deal brings together complementary capabilities, expanding the company’s service portfolio and strengthening its position in modern marketing.

With shared strengths in creativity, technology, and data, the combined entity is expected to unlock new growth opportunities. The integration is also likely to accelerate innovation, enabling Omnicom to develop advanced solutions that deliver higher returns on clients' marketing investments.

Additionally, the combined organization’s strong free cash flow generation enhances financial flexibility. This allows Omnicom to reinvest in the business, pursue further acquisitions, and drive long-term value creation. While the strategic rationale is compelling, execution will be key to realizing these benefits.

Strong Shareholder Returns Support Investor Confidence

Omnicom has consistently demonstrated its commitment to returning value to shareholders through dividends and share repurchases. Over the past several years, the company has maintained substantial payouts, reflecting stable cash flow generation and disciplined capital allocation.

This consistent return profile reinforces investor confidence and adds downside support to the stock. For income-focused investors, Omnicom’s track record of shareholder-friendly policies remains an attractive feature.

Omnicom’s dividend payouts were at $581.1 million in 2022, $562.7 million in 2023, $552.7 million in 2024, and $549.6 million in 2025. Share repurchases totaled $611.4 million, $570.8 million, $370.7 million, and $707.9 million in the respective years.

Competitive Pressures Remain Intense

Despite its strengths, Omnicom operates in a highly competitive and fragmented industry. It faces stiff competition from global giants like WPP WPP and Publicis Groupe PUBGY, both of which have strong digital and data-driven capabilities.

WPP continues to invest aggressively in technology and creative services, intensifying pricing pressures across the industry. At the same time, Publicis Groupe has built a strong reputation in data-driven marketing, further raising the competitive bar.

The presence of WPP and Publicis Groupe highlights the need for continuous innovation and investment, which can weigh on margins in the short term.

Moreover, smaller, agile digital firms are capturing niche opportunities, adding another layer of competition. These dynamics make it challenging for Omnicom to sustain consistent high growth without increasing spending.

Integration and Liquidity Concerns Add Risk

The Interpublic acquisition, while strategically beneficial, introduces near-term uncertainties. Integrating two large organizations involves operational complexities, potential cultural mismatches, and restructuring costs. These factors could temporarily pressure profit margins and weigh on earnings as the company navigates integration challenges and restructuring costs. Additionally, Omnicom’s liquidity position raises some concerns. A current ratio below 1 indicates limited short-term financial flexibility, suggesting that the company may face challenges in meeting near-term obligations without relying on external financing. In an uncertain macro environment, such financial constraints could amplify risks.

Final Take: A Balanced “Hold” Story

Omnicom combines strong fundamentals with notable near-term challenges. Its diversified business model, strategic investments, and shareholder-friendly policies provide a solid base for long-term growth. At the same time, competitive intensity, integration risks, and liquidity concerns temper the near-term outlook.

Given this balance, the Zacks Rank #3 (Hold) appears appropriate. Investors may benefit from adopting a “wait-and-see” approach, monitoring how effectively Omnicom executes its integration strategy and navigates competitive pressures before taking a more decisive position. You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Omnicom Group Inc. (OMC): Free Stock Analysis Report

Publicis Groupe SA (PUBGY): Free Stock Analysis Report

WPP PLC (WPP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).