Tesla (TSLA) is making a bigger push in Taiwan as part of its artificial intelligence chip plans. The company has posted new engineering jobs there for its Terafab AI chip complex, which fits into CEO Elon Musk’s $20 billion to $25 billion plan to bring more of Tesla’s chip work in-house instead of relying heavily on suppliers like Taiwan Semicondutor Manufacturing (TSM) and Samsung.

This is not some small side project. Terafab is being built to produce up to 200 billion AI and memory chips a year, with a goal of 100,000 wafer starts a month using 2-nanometer technology. Earlier this month, Intel (INTC) joined the Terafab effort alongside Tesla, SpaceX, and xAI. Together, the project is aiming for up to 1 terawatt a year of compute capacity across two planned sites, with one site focused on vehicles and robots and another built for space-based AI data centers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

That is why the Taiwan hiring matters. Tesla is going after talent in the same place where Taiwan Semiconductor is based, at a time when Musk says outside suppliers cannot fully meet Tesla’s demand for the AI5 chip, which is tied to Full Self-Driving IFSD), the Cybercab robotaxi, and the Optimus robot.

With Tesla stepping up hiring in Taiwan and spending heavily on this chip buildout, the real question is simple: does this make TSLA stock a buy near $400? Or are investors getting ahead of the story again?

The Numbers Behind the Tesla Case

Tesla makes and sells electric vehicles (EVs), but the company is no longer just about cars. Tesla also has growing businesses in energy storage, software, and other areas of tech. TSLA stock has had a strong run over the past year, rising more than 70% in the last 52 weeks, although the stock is still down more than 13% so far this year.

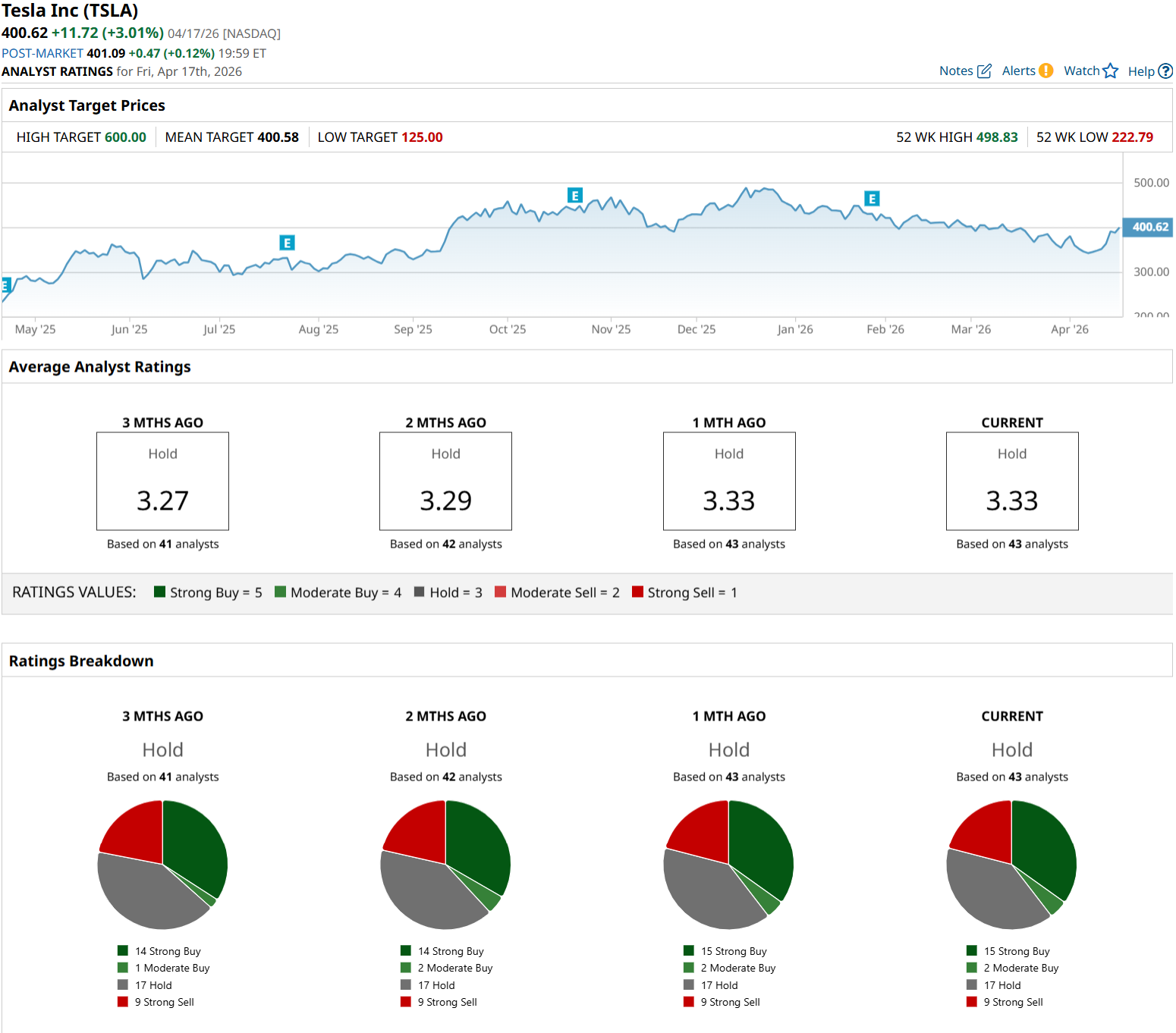

www.barchart.com

www.barchart.comThat helps explain why Tesla still trades at a very rich valuation. Its forward price-to-earnings (P/E) ratio is 292.5 times, compared to the sector average of 16.2 times.

In the fourth quarter of 2025, Tesla delivered 418,227 vehicles, which missed analyst estimates of 428,536 vehicles by 2.4%. Revenue came in at $24.9 billion, a little below the $25.12 billion Wall Street expected. Still, earnings were better than feared. GAAP operating profit came in at $1.41 billion, topping estimates of $1.29 billion by nearly 9%. Non-GAAP EPS of $0.50 beat the $0.45 consensus by almost 11%.

Automotive revenue was $17.69 billion versus the expected $17.92 billion, energy revenue was $3.84 billion compared with $3.86 billion expected, and services revenue was $3.37 billion against the $3.38 billion forecast. Gross margin improved to 20.1% from 16.3% a year earlier, while operating margin held steady at 5.7%, showing that Tesla is still doing a decent job managing profitability even as revenue growth faces pressure.

What Is Driving Tesla’s Long-Term Growth Story?

Tesla is trying to grow by reaching more buyers in its core EV business. Reports say the company is working on a smaller, cheaper electric SUV that would be a completely new model, not just another version of the Model 3 or Model Y. This EV is expected to launch first in China, then later in the U.S. and Europe. At about 14 feet long, it would be smaller than the nearly 16-foot Model Y, which could help Tesla offer a more affordable option as it tries to lift slowing sales.

The company is also putting serious money into its energy business. Tesla plans to build a $4.3 billion battery plant in Lansing, Michigan, with LG Energy Solution, with production expected to start in 2027. The plant will make batteries for Megapack 3 systems, with the cells shipped to Houston, Texas, for Tesla’s stationary storage business.

Tesla is also trying to tighten control over battery materials. The company's lithium refinery near Corpus Christi, Texas, is now up and running, and Tesla says it is the largest and most advanced facility of its kind in the United States. The site turns spodumene ore into battery-grade lithium hydroxide using a process that is reportedly “cleaner, simpler, and cheaper.” That gives Tesla more control over a key battery material as it grows both its car and energy businesses.

What Do Analysts Think of TSLA Stock?

Analysts expect Tesla to earn $0.21 per share for the March 2026 quarter, up from $0.15 a year earlier. For the June quarter, the estimate is $0.29 versus $0.27 the same time last year. For full-year 2026, Wall Street foresees earnings of $1.37 per share, up roughly 26% year-over-year (YOY) from $1.09 per share.

Barclays recently kept an “Equal Weight” rating on TSLA stock with a $360 price target, saying sentiment has improved around Tesla’s AI and software plans. However, the firm is still cautious because of pressure on auto margins.

UBS analyst Joseph Spak also became less bearish ahead of the upcoming first-quarter report, upgrading TSLA stock from “Sell” to “Neutral.” That said, the analyst kept his $352 target and still pointed to concerns about deliveries and robotaxi rollout goals.

Overall, TSLA stock has a consensus “Hold” rating from 43 analysts, with an average price target of $400.58. Because the stock recently surpassed the $400 level before retreating to around $386 as of this writing, it is basically sitting right at that target. That suggests Wall Street sees limited upside from here.

www.barchart.com

www.barchart.comConclusion

So, does Tesla’s Taiwan Terafab hiring push make TSLA stock a buy now? Not quite. The hiring wave adds another real piece to the firm's long-term AI and chip strategy, and it strengthens the argument that Tesla is serious about building more of its own silicon stack instead of staying boxed in by outside foundry limits. But with the stock already trading in line with Wall Street’s average price target and still carrying a rich premium valuation, a lot of that future promise already looks priced in. Tesla shares will most likely stay volatile in the near term and trade on earnings, delivery execution, and proof that these AI bets can turn into actual margin and profit growth.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tesla Is Ramping Up Hiring for Its Taiwan Terafab. Does That Make TSLA Stock a Buy Now? Missed Nvidia? AMD Could Be Your Second Chance to Earn Massive AI Gains TSLA Stock Catalyst: Get Ready for a Larger Model Y After the Blue Origin Satellite Failure, Is It Time to Sell AST SpaceMobile Stock?