British semiconductor juggernaut Arm Holdings plc (ARM) reached an all-time high of $210.80 today, and is only slightly down from that level. The stock reached this level after a six-day bull run on Wall Street (as of the writing of this article), with a 12% intraday gain on April 22. The stock is facing heightened demand for semiconductors as the artificial intelligence (AI) boom keeps a strict hold on the market. Investors are also looking forward to its upcoming earnings early next month.

Should you buy the stock now?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Arm Stock

Arm Holdings plc, headquartered in Cambridge, England, operates as a leading British semiconductor and software design company. It specializes in developing central processing unit cores based on the ARM architecture, along with graphics processing units, neural processing units, and system-on-chip infrastructure.

Rather than manufacturing chips, Arm licenses its intellectual property to partners worldwide, enabling efficient production of processors for smartphones, tablets, automobiles, networking gear, and data centers. This model supports diverse applications through product lines tailored for high-performance computing, real-time systems, microcontrollers, and security features, while providing software tools and platforms to streamline development for its licensees. The company has a market capitalization of $207.7 billion.

Driven by robust demand for its architecture in AI-powered chips, data centers, and Internet of Things devices, Arm’s stock has gained 93.72% over the past 52 weeks and 86.37% year-to-date (YTD).

www.barchart.com

www.barchart.com Its 14-day RSI of 81.81 indicates the stock is currently in overbought territory. On a forward-adjusted basis, Arm’s price-to-sales ratio of 42.60 times is considerably higher than the industry average of 3.20 times.

Arm Smashed Q3 with AI Licensing Surge, Data Center Boom

For the third quarter of fiscal 2026 (quarter ended Dec. 31), Arm reported record results. The company’s revenue increased by 26% year-over-year (YOY) to $1.24 billion. This was due to a 25% growth in licensing revenue to $505 million, while royalty revenue increased 27% to $737 million. The increase in royalty revenues was led by growth across its target end markets, while the licensing revenue growth was led by more leading companies signing high-value licenses for next-generation technologies.

The top line performance also boosted Arm Holdings' bottom line by double-digit rates. Its non-GAAP operating income grew 14% YOY to $505 million, while non-GAAP EPS surged 10% to $0.43. Its annualized contract value by the end of the third quarter was $1.62 billion, up 28% YOY. However, its remaining performance obligations dropped by 8% to $2.15 billion.

Wall Street analysts have a tepid outlook on Arm’s future earnings. For fiscal year 2026, EPS is projected to drop 19.8% annually to $0.85 (to be reported on May 6, after the market closes), followed by a 38.8% surge to $1.18 in the fiscal year 2027. Analysts expect the company’s EPS to drop by 11.9% YOY to $0.37 for the fourth quarter of FY2026.

Here’s What Analysts Think About Arm’s Stock

Recently, Wall Street analysts have shown their mixed feelings about Arm. This month, analysts at Susquehanna raised Arm’s price target from $170 to $210, while keeping a “Positive” rating on the stock. Analysts at the firm believe there is an attractive risk/reward opportunity in the stock, supported by long-term TAM expansion driven by AI and advanced computing. On the other hand, while acknowledging market opportunities in the semiconductor ecosystem, Goldman Sachs kept a “Sell” rating on the stock, but raised the price target from $110 to $125.

Morgan Stanley analysts downgraded Arm’s stock from “Overweight” to “Equal Weight.” Analyst Lee Simpson sees potential in the company’s new AGI-oriented CPU design, which is specifically built for agentic AI workloads. However, the analyst also believes that the commercial ramp will take time, while near-term risks remain.

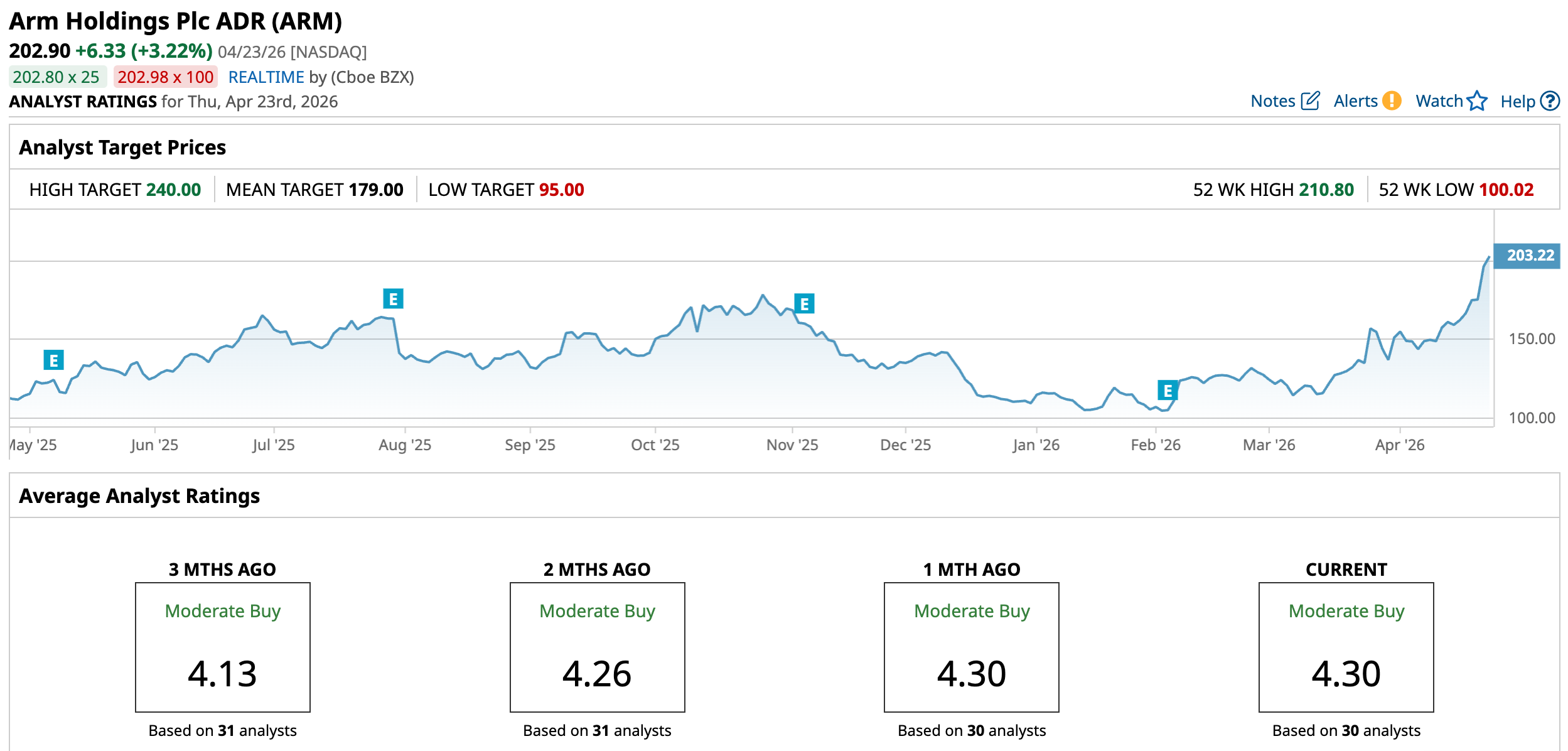

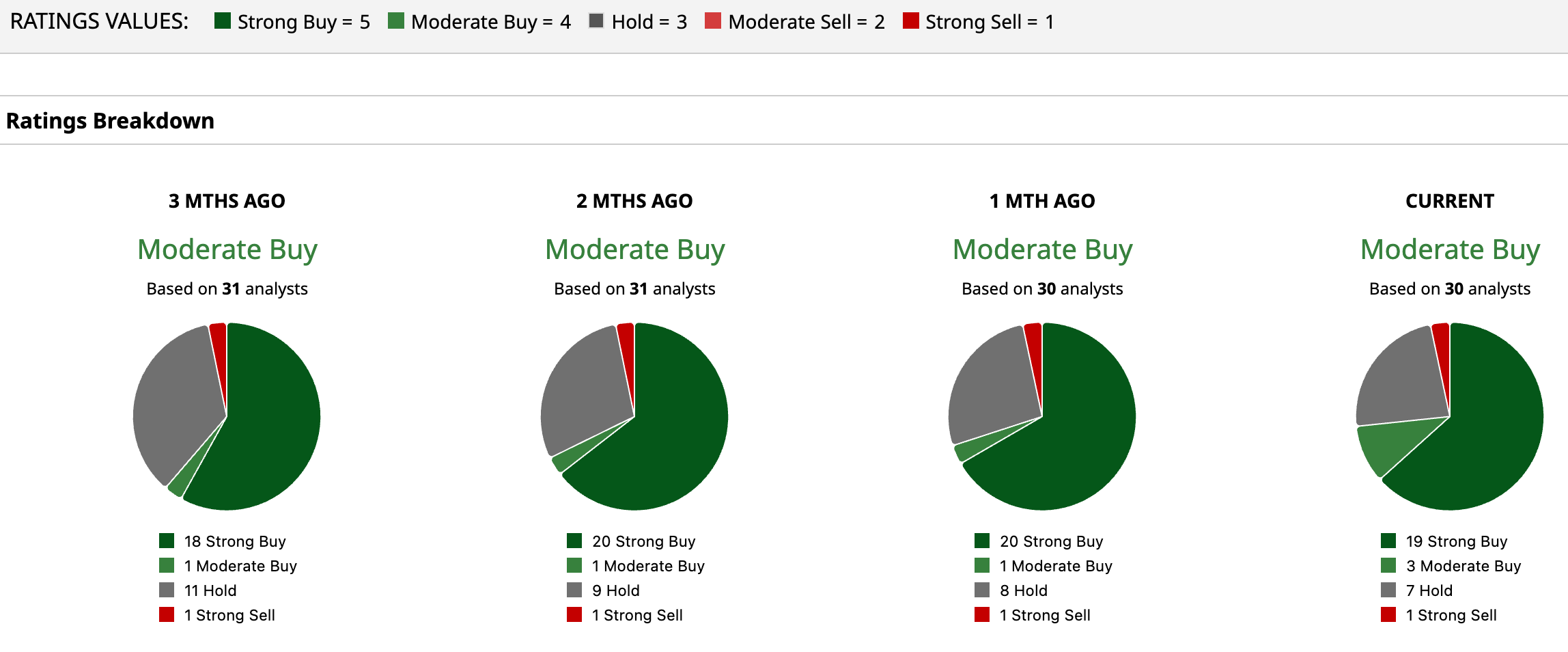

Arm Holdings is still praised on Wall Street, with analysts awarding the stock an overall “Moderate Buy” rating. Of the 30 analysts rating the stock, 19 have rated it a “Strong Buy,” three a “Moderate Buy,” seven a “Hold,” and one a “Strong Sell.” The consensus price target of $179 represents an 11.8% downside from current levels. However, the Street-high price target of $240 indicates an 18.3% upside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Key Takeaways

Arm Holdings has gained significant traction on Wall Street due to its dominant role in powering AI data centers. As the company gears up to report earnings soon, the stock might be a “Buy” for risk-loving investors, given analysts' expectations of further upside at the Street-high target.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Is Arm Stock a Buy at New All-Time Highs? Should You Buy the Dip in IBM Stock Today? Uber Has an 11.52% Stake in Lucid. Does That Make LCID Stock a Buy? Wall Street Can’t Seem to Get Enough of Intel Stock