Back in April 2020, I sold my Lululemon Athletica (LULU) shares at $184.27 to buy a MacBook and a Grammarly subscription to start a copywriting business. That decision launched a career that eventually led me to Barchart, so in a real sense, Lululemon stock is part of the reason I’m writing this article today.

Brokerage account screenshot courtesy of Justin Estes for Barchart

Brokerage account screenshot courtesy of Justin Estes for Barchart Six years later, that stock is trading in the $140 range, lower than when I cashed out to chase a different dream. And based on what I’m seeing in the company’s financials and Wednesday’s CEO announcement, I’m not ready for another tight squeeze with this stock anytime soon.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Nike Executive Fails to Impress Shareholders

Lululemon selected former Nike (NKE) executive Heidi O’Neill as CEO on Wednesday, triggering a 12% plunge that wiped nearly $2 billion off the company’s valuation. Shares dropped to around $144, their lowest level since 2020.

“We do not expect the market to receive this appointment positively given O’Neill’s longstanding tenure at Nike, which overlaps with the brand developing many challenges that parallel the ones LULU is currently facing,” BTIG analyst Janine Stichter said in a note to clients.

O’Neill, who left Nike in September 2025 and won’t start at Lululemon until her non-compete expires in September 2026, was most recently president of consumer, product, and brand at Nike. She’s credited with growing the women’s business and increasing apparel sales.

But here’s the problem: Her tenure at Nike coincided with years of slowing demand, brand fatigue, and execution missteps, which are the same challenges Lululemon faces today.

The Tale of Two Struggling Apparel Giants

Nike’s stock hit a more-than-decade low this month after CEO Elliott Hill warned of a sharp sales drop and continued weakness in China. Over the past five years, Nike shares are down roughly 75% from their 2021 highs.

www.barchart.com

www.barchart.comLululemon’s five-year chart tells an eerily similar story. Shares peaked above $500 in late 2023 before sliding to the current $140 range, a decline of more than 57% from those highs.

www.barchart.com

www.barchart.comBoth companies are losing ground to nimble direct-to-consumer brands. Lululemon faces intensifying competition from upstart brands like Alo Yoga and Vuori in the U.S. Nike battles similar challengers across athletic footwear and apparel such as Hoka and On Cloud.

“Lululemon needs a turnaround CEO and not a growth CEO,” BNP Paribas analyst Laurent Vasilescu wrote.

Founder Chip Wilson Wants More Than a New Face

Lululemon founder Chip Wilson, who owns about 4.3% of the company and says the brand has lost its “cool” factor, continues pushing for a complete board overhaul. According to Reuters, Wilson believes new directors should have been installed before hiring a CEO.

The appointment ends a months-long search triggered when activist investor Elliott Investment Management pushed for change at the top. Former CEO Calvin McDonald left at the end of January after nearly eight years in the role.

Several investors, including Elliott (which built a more than $1 billion stake last year), reportedly preferred former Ralph Lauren (RL) executive Jane Nielsen. Analysts at Needham and Evercore ISI credit Nielsen, who served as CFO at Ralph Lauren for eight years until 2024 and for five years at Coach, with turning around higher-margin business models at both companies.

The Financials Don’t Inspire Confidence Either

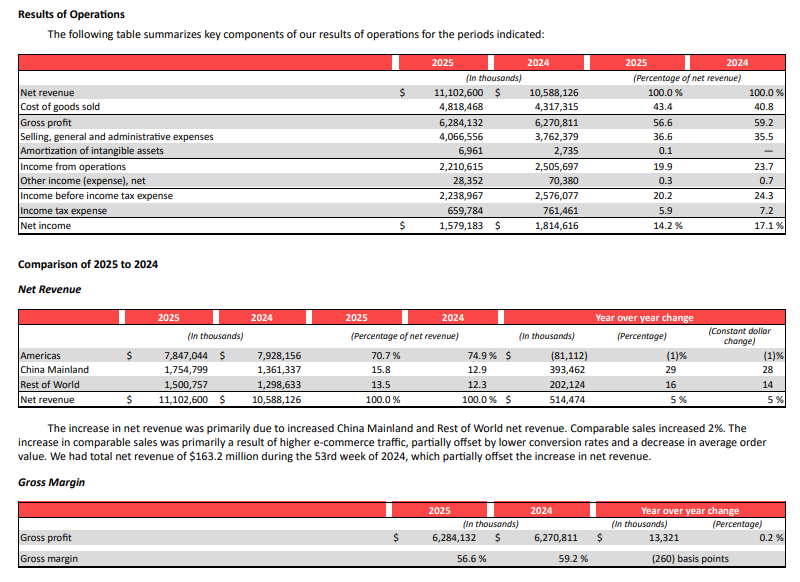

Lululemon’s latest annual report reveals a company at a crossroads. Net revenue increased 5% to $11.1 billion, but the geographic breakdown exposes a core problem:

Americas comparable sales decreased 3%. China Mainland comparable sales increased 20% (19% on a constant dollar basis). Rest of World comparable sales increased 9% (7% on a constant dollar basis).

Put simply, Lululemon is tapping out in North America and betting heavily on overseas expansion to drive growth. That’s the same playbook American brands have run for decades when domestic momentum stalls. However, that strategy can be very dangerous, especially in the Chinese market, especially if the government decides to back a domestic athleisure brand which could kneecap LULU’s growth, similarly to American automotive manufacturers like Tesla (TSLA) and Ford (F) losing ground to BYD (BYDDY).

Gross margin decreased 260 basis points to 56.6%. Income from operations fell 12% to $2.2 billion. These aren’t catastrophic numbers, but they’re not the metrics of a brand firing on all cylinders either.

Stock Buybacks Raise Questions

Lululemon spent approximately $1.178 billion on share repurchases in fiscal 2025. Warren Buffett famously loves stock buybacks because they’re not taxed like dividends and increase remaining shareholders’ proportionate interest.

But Buffett also emphasizes that buybacks only make sense when executed at attractive valuations. Lululemon has been buying back stock while shares dropped from the $300s to the $140s. That capital could have funded product innovation, supply chain improvements, or marketing to combat the Alo Yogas and Vuoris eating away at market share.

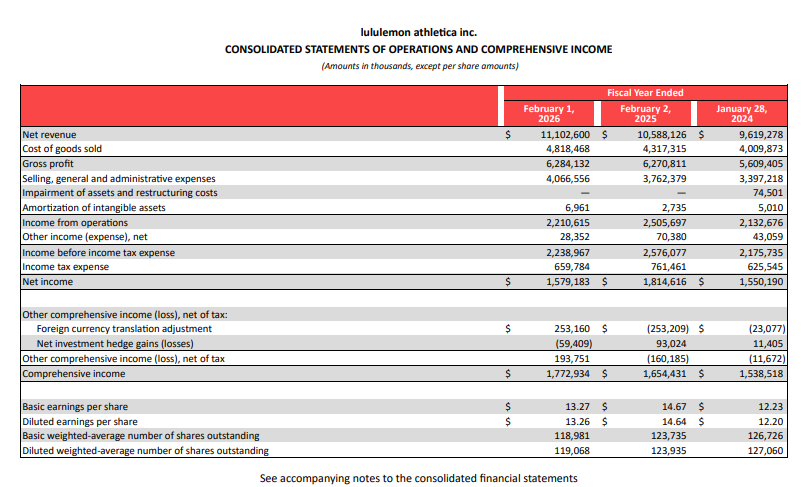

The cash flow statement indicates that Lululemon generated $2.27 billion from its operating activities. After accounting for $680 million in capital expenditures, the company had approximately $1.6 billion in operating cash flow. The decision to allocate most of this amount toward share buybacks, especially amid declining margins and domestic sales, raises questions about the company’s capital allocation priorities.

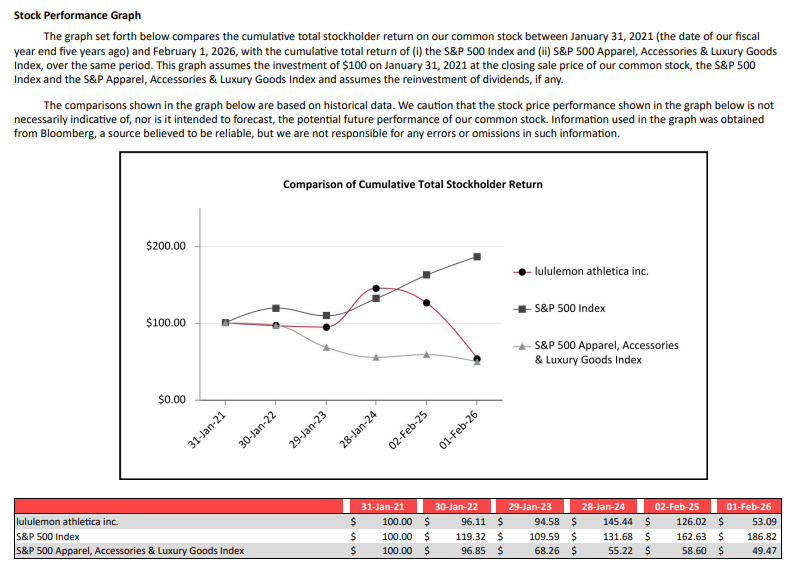

Performance vs. Benchmarks Tells the Real Story

Lululemon’s own annual report includes a brutal stock performance graph. From Jan. 31, 2021 through Feb. 1, 2026, $100 invested in Lululemon returned just $53.09. The same $100 in the S&P 500 Index ($SPX) returned $186.82. Even the S&P 500 Apparel, Accessories & Luxury Goods Index returned $49.47, only slightly trailing Lululemon.

For a company that once dominated the athleisure space with innovative products and cult-like brand loyalty, barely keeping pace with struggling peers is not a position of strength.

Leggings Can Only Do So Much

The current share price near $140 might look tempting for investors without athleisure exposure. Lululemon has significant brand power, a loyal customer base, and strong international growth.

But this feels like the beginning of a make-or-break period, not the end. The company knows it needs to improve speed to market. Management knows margins need protection. The board knows investors want change.

What remains unclear is whether Heidi O’Neill can deliver a turnaround when her previous employer struggled with nearly identical challenges throughout her tenure. The proxy fight adds another layer of uncertainty that won’t resolve until June at the earliest.

Much like their signature yoga pants, this investment thesis requires more flexibility than I’m comfortable with right now. I sold at $184 in 2020 to start something new. Six years later, with more questions than answers, I’m not ready for another tight squeeze.

On the date of publication, Justin Estes did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Much Like Their Pants, I’m Not Ready for Another Tight Squeeze with Lululemon’s Stock Intel Just Hit a New All-Time High. Does INTC Stock Have More Room to Run? As Nike Announces Second Round of Layoffs, Is NKE Stock a Buy, Sell, or Hold? Tesla Is Making a $2 Billion Bet on Hardware as AI-Focused SpaceX IPO Draws Near. Is TSLA Stock Safe to Buy?